Renewable Energy, Green Financing, and Market Impact in South America

Executive Summary

South America is rapidly emerging as one of the world’s fastest-growing data center markets. Once overshadowed by established global hubs such as Frankfurt, Northern Virginia, and Singapore, the region is now attracting large-scale investment driven by cloud adoption, hyperscaler expansion, regulatory localization, and abundant renewable energy.

The South American data center market is projected to grow from USD 3.78 billion in 2025 to USD 6.42 billion by 2030, representing a compound annual growth rate (CAGR) of 11.18% (Mordor Intelligence, 2025).

IT load capacity is expected to expand from 1.51 GW to 2.23 GW over the same period, reflecting rising demand from hyperscale cloud platforms, AI workloads, and 5G-enabled edge computing.

Brazil and Chile anchor the region’s growth. Brazil leads in scale and capacity, while Chile has positioned itself as the region’s sustainability-focused hub, attracting ESG-driven hyperscaler investment.

Together, these markets illustrate how renewable energy availability, green financing, and regulatory clarity are shaping South America’s data infrastructure landscape.

South America's renewable energy growth, green financing, and data center market impact, highlighting Brazil and Chile’s energy mix, ESG investment trends, cloud demand, and internet expansion.

The Forces Driving South America’s Data Centre Growth

The surge is driven by concurrent trends that have created unprecedented demand for local data infrastructure.

Connected Population: With an estimated 345 million internet users in South America as of October 2025 anda young population, the continent offers great potential for digital services (ITU Internet Use Statistics , World Population Review 2025). Colombia’s creative industries and São Paulo’s fintech are driving demand for low-latency data services.

Subsea Cable Expansion: South America’s digital links to the world are strengthening. High-capacity subsea cables such as Humboldt, Firmina, and Malbec now connect the region to global data routes.

Cities such as Chile, Brazil, and Argentina are the landing points. They are turning into key network hubs that enable faster connections and support the growth of data centres.

Data Sovereignty Regulations: Regulation is now a growth driver. Modeled on Europe’s GDPR, Brazil’s Lei Geral de Proteção de Dados (LGPD) enforces data protection and localisation rules. Similar laws are being set in other South American Countries, forcing businesses to host and process user data locally, driving strong demand for regional data centers.

Post-Pandemic Digital Economy: The COVID-19 pandemic altered the digital landscape. There was a 30% increase in internet usage in Latin America, boosting remote work, e-commerce, and fintech growth (World Bank). This shift has created a demand for stronger local computing power.

Hyperscalers Race for Cloud Market Dominance: Competition among major cloud providers, AWS, Google Cloud, and Microsoft Azure, is fueling infrastructure growth.

These cloud providers are the largest consumers of capacity. They are expanding regional networks that meet enterprise needs. Microsoft’s $3.1 billion investment in Cloud and AI highlights the scale of this shift.

Key Markets: Brazil, Chile, and Emerging Hubs Brazil: Scale and Renewable Advantage

Brazil is also the region’s renewable energy leader. Around 89% of its electricity comes from renewables, largely hydropower, supported by fast-growing wind and solar capacity. This gives Brazil a structural advantage in powering large-scale data infrastructure with low-carbon electricity.

Brazil accounts for approximately 40% of Latin America’s data centre capacity. São Paulo ranks among the world’s top emerging data centre markets. The country’s scale, dense fibre networks, and steady enterprise demand keep it in a leadership position. Demand comes from both traditional enterprise clients and fast-growing AI and IoT workloads.

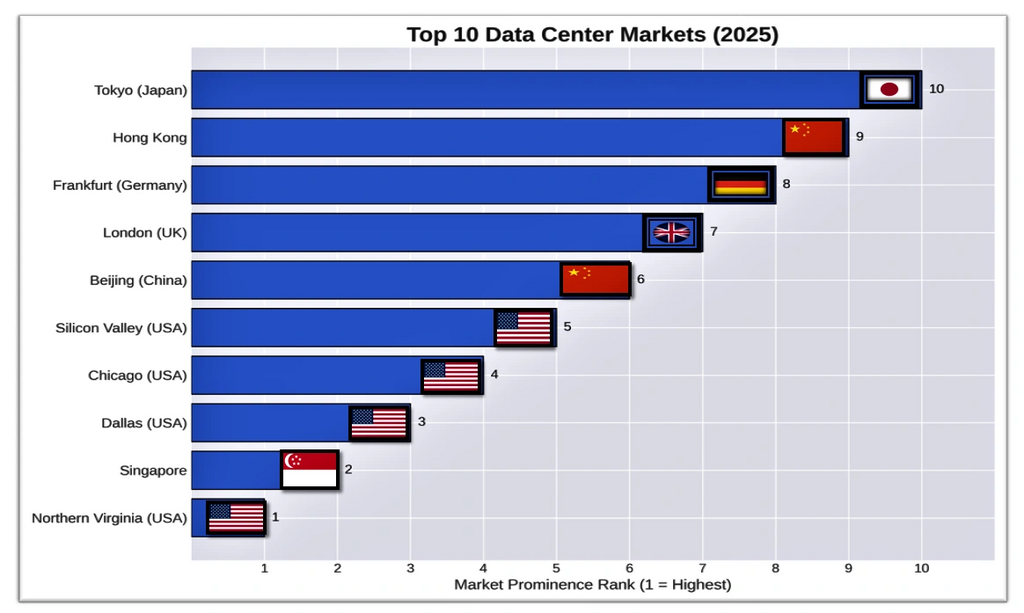

Top 10 Global Data Center Markets 2025 ranked by prominence with country flags – Northern Virginia, Singapore, Dallas, Chicago, Silicon Valley, Beijing, London, Frankfurt, Hong Kong, Tokyo. Source: Abramwireless

Prominence indicates how influencial, important and dominant a data center market is globally.

Key Indicators of Prominence

Total capacity (MW): How much IT load the market can support.

Hyperscale presence: Number of major cloud providers (like AWS, Azure, Google Cloud).

Connectivity: Access to fiber networks, internet exchanges, and latency performance.

Investment volume: Real estate, infrastructure, and energy investments.

Strategic location: Proximity to financial hubs, population centers, or geopolitical importance.

Regulatory and sustainability leadership: Compliance with data laws and green energy adoption.

Takeaway: The graph highlights that while the U.S. remains dominant, Asia-Pacific and Europe are catching up fast, driven by AI adoption, sovereign data laws, and sustainability mandates.

Chile: The Sustainability-Focused Hub Chile has positioned itself as the region’s sustainability-focused data centre hub. In 2024, renewables supplied about 70% of Chile’s electricity, driven mainly by rapid growth in solar and wind. While this share is lower than Brazil’s hydro-led mix, Chile’s energy transition is among the fastest in Latin America.

Chile is the first Latin American country to legally commit tocarbon neutrality by 2050. It is phasing out coal generation by 2040 and has issued green bonds while enforcing a national CO₂ tax to accelerate clean energy investment.

These policies, combined with political stability, make the country highly attractive to hyperscalers with Environmental, Social, and Governance mandates.

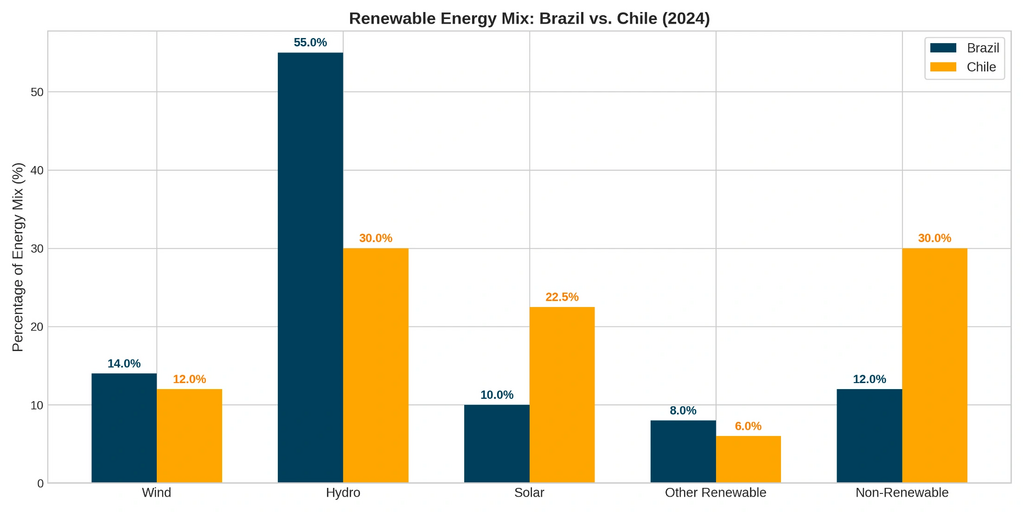

Brazil vs Chile renewable energy mix 2024 bar chart comparing hydro, wind, solar, other renewables, and non-renewable sources

Key Insights from the Renewable Brazil's and Chile's Energy Mix

Brazil's grid is powered primarily by hydropower (55%), giving it a stable, low-carbon foundation for data center growth, though with some climate vulnerability.

Chile leads in solar penetration (22.5% vs Brazil's 10%), reflecting its aggressive energy transition and making it ideal for sustainable data operations aligned with corporate ESG goals.

Brazil's higher overall renewable percentage (89% vs 70%) provides an immediate carbon advantage, while Chile's diversified mix signals faster transition momentum, with both countries offering strong green power propositions for data center operators.

Implications: High renewable penetration lowers operating costs and carbon intensity, positioning South America favorably against fossil fuel-dependent digital infrastructure regions.

Emerging South American Data Center Markets Beyond Brazil and Chile, several countries are rapidly expanding their data center presence due to digital growth, supportive policies, and rising demand for cloud and AI infrastructure:

Colombia: Experiencing strong growth, attracting major AI infrastructure investments backed by national strategies.

Peru: Smaller in capacity but actively participating in regional expansion.

Panama: Developing as a digital hub, seeing increasing data center investment alongside Costa Rica and Peru.

Argentina: Drawing investment with energy opportunities from resources like the Vaca Muerta shale play.

Uruguay: Leveraging renewable energy to support sustainable data center development.

ESG Leadership and Global Operators

Global data center and cloud operators are reinforcing ESG leadership across the South American region:

Equinix sources 96% renewable energy globally and targets climate neutrality by 2030 through PPAs and advanced cooling systems.

Google has matched 100% of its electricity consumption with renewables since 2017 and is pursuing 24/7 carbon-free energy by 2030, with average data center PUE of 1.09.

Microsoft aims to be carbon negative by 2030, deploying waste-heat recovery and circular hardware reuse strategies. Its decision to establish a major Azure region in Chile underscores the country’s growing role as South America’s green data center hub.

Brazil remains the regional hub, with major investments in São Paulo, while Chile is emerging as a sustainability-focused destination due to its fast-growing wind and solar capacity.

Hyperscalers like AWS, Google, and Microsoft set the standard for ESG alignment, encouraging local operators to adopt global sustainability practices.

Green financing, advanced cooling technologies, and strategic renewable energy agreements are key trends driving growth and ensuring that South America’s data center market expands responsibly and sustainably.

The Market Players

There are three tiers of players that pose competition, which pushes the market to grow and innovate faster.

Global Colocation Giants: Companies such as Digital Realty, Equinix, and EdgeConnex form South America’s digital infrastructure backbone. These global colocation giants operate interconnected hubs that support enterprises and small cloud providers to ensure strong network resilience and connectivity.

The Hyperscalers: AWS, Microsoft Azure, and Google Cloud are considered to be the demand drivers. Their capital expenditure on large data centers defines scale and expansion across the region.

Regional Champions: Regional companies such as KIO Networks, Elea Digital, and ODATA drive growth through local insight. Their local expertise on regional markets helps them secure land, permits, and power faster than global competitors.

The Role of Green Financing

The growth of sustainable data centers is being catalyzed by specialized financing. Green bonds, sustainability-linked loans (SLLs), and financing from development banks (e.g., IFC, IDB Invest) are becoming critical tools. These instruments tie funding to ESG performance targets, such as achieving a specific Power Usage Effectiveness (PUE) or renewable energy percentage.

Regional operators like Scala and ODATA have successfully tapped these markets to fund expansions, demonstrating how global ESG capital flows are directly enabling South America's infrastructure build-out.

Challenges Ahead

The data center market’s rapid growth in South America has exposed structural and operational challenges that need to be considered.

Geopolitical and Economic Volatility: Brazil’s currency, the Brazilian real (BRL), is a characteristically volatile emerging market currency, sensitive to global commodity prices and domestic politics.

This inherent volatility exposes businesses to substantial FX risk, with direct implications for capex costs, power contracts, and foreign debt exposure. In 2024, the BRL lost more than 20% of its value against the USD, before appreciating roughly 13% year-to-date in 2025 due to high domestic interest rates and a weaker US dollar.

Power and Water Scarcity: In South America, Brazil, Chile, and Colombia are driving data center growth while prioritizing sustainability. Brazil hosts major operators like Scala Data Centers and ODATA, which integrate 100% renewable energy and liquid cooling to support AI workloads.

Chile is expanding its green data center regions, leveraging wind and solar energy. Colombia is rapidly scaling its infrastructure with a focus on renewables.

Talent and Supply Chain: Shortages of skilled technical workers and constrained supply of critical equipment, such as switchgear and generators, continue to slow expansion. In early 2024, Brazil delayed about 5.39 GW of planned power generation capacity, according to the National Electric Energy Agency (ANEEL).

Delays affected solar (2.64 GW), wind (1.95 GW), biomass (412 MW), and other projects. Causes included construction issues, licensing delays, grid access bottlenecks, PPA challenges, and regulatory uncertainty.

Outlook: Distributed, AI-Ready, and Sustainable

The next phase of growth is shifting away from centralized hyperscale facilities toward more distributed infrastructure.

Sustainability as a License to Operate: 24/7 carbon-free energy sourcing and green building standards will evolve from a market differentiator to a basic requirement for new data center projects that are driven by both future regulations and corporate ESG.

The Edge Computing Wave: Real-time applications such as telemedicine, autonomous mining, and smart cities will drive the rise of smaller edge data centers in secondary cities, positioning computing power close to users for lower latency and faster processing.

AI-Ready Infrastructure: The global AI surge will require a new generation of data centers in South America. These facilities will be equipped with high-power density and direct liquid cooling to support AI training workloads. Forward-thinking developers will gain a strong competitive edge.

Building South America’s Digital Foundation

South America’s data boom is more than infrastructure growth; it's the continent's foundational bedrock for its own digital independence. Investing billions in local computing capacity will reduce its reliance on foreign infrastructure, which will foster local innovation and strengthen global competitiveness. With every new data center, South America’s data infrastructure grows more resilient, faster, and stronger.

Implications for Stakeholders

1. Policymakers: Develop clear regulatory frameworks that encourage sustainable data center growth. Offer incentives such as tax breaks and renewable energy subsidies, while ensuring data sovereignty policies balance privacy with investment appeal.

Support workforce development through technical education and training programs to build local expertise for operating advanced AI and cloud infrastructure. Facilitate streamlined permitting and licensing to reduce project delays and attract both domestic and international investors.

2. Corporations and Data Center Operators: Focus on integrating renewable energy through Power Purchase Agreements (PPAs) and local green energy partnerships. Implement advanced cooling technologies, including liquid immersion systems, to increase efficiency and reduce water usage.

Align ESG strategies with international standards such as LEED and ISO 50001 to attract hyperscaler clients and investors. Expand AI-ready infrastructure with scalable, high-density power solutions to meet growing demand from cloud and edge computing applications.

3. Technology and Cloud Companies: Lead the market in carbon neutrality, renewable energy adoption, and resource efficiency to influence local operators and policy frameworks. Partner with governments and regional operators to develop resilient, distributed infrastructure that reduces latency and strengthens digital independence.

Invest in edge computing, AI-ready data centers, and initiatives supporting data sovereignty to meet the demands of fintech, telemedicine, smart cities, and other emerging digital applications.

Key Takeaways

South America is the fastest-growing data center market in 2025, fueled by cloud demand, AI, and post-pandemic digitalization.

Brazil leads in capacity; Chile leads in sustainability. Emerging markets like Colombia, Peru, Panama, Argentina, and Uruguay are rapidly expanding.

Renewable energy and advanced cooling are central to sustainable growth.

The market faces challenges in economics, resources, and talent.

Growth will focus on distributed, AI-ready, and edge infrastructure.

Collaboration between governments, corporates, and tech companies is key to resilient, inclusive digital development.

Frequently Asked Questions

1. Why is South America the fastest-growing data center market?

South America is growing fastest due to cloud and AI demand, data-localization laws, subsea cables, and abundant renewable energy.

2. Which South American country is best for hyperscale data centers?

Brazil leads in scale and connectivity, while Chile leads in renewable energy, ESG policy, and sustainability-focused hyperscale deployments.

3. How important is renewable energy for data centers in South America?

Renewables are critical: Brazil runs on an estiamated 89% clean energy and Chile 70% estimate, lowering costs, emissions, and ESG risk for hyperscalers.

4 . Are hyperscalers investing in South America?

Yes. AWS, Google, and Microsoft are investing billions in South America to support cloud, AI, data sovereignty, and low-carbon operations.

5. What challenges affect data center expansion in South America?

Key risks include power and water constraints, FX volatility, talent shortages, and grid connection delays despite strong demand.

Executive Summary Africa’s 2026 growth and risk landscape is being reshaped by high-stakes agreements and regional macro developments. The Washington Accords between the DRC and Rwanda aim to de-escalate conflict in eastern Congo, while Kenya’s Health Cooperation Framework with the US seeks to strengthen state-led healthcare financing.

Across the continent, additional factors, including Nigeria’s fiscal reforms, South Africa’s energy crisis, and East African infrastructure challenges, create a complex mix of opportunity and execution risk.

Key takeaway:

Investment, trade, and insurance outcomes in Africa in 2026 will depend more on implementation, governance, and enforcement than on policy announcements.

What Is the DRC–Rwanda Peace Deal (Washington Accords)?

What was signed, and why it matters

The DRC–Rwanda peace deal, commonly referred to as the Washington Accords, is a US-facilitated agreement signed in 2025 to reduce hostilities in eastern Democratic Republic of the Congo. The accord emphasizes sovereignty, non-interference, ceasefire adherence, and political dialogue, with the stated goal of enabling regional trade, investment, and humanitarian access.

The United Nations views the agreement as a “critical step,” while cautioning that hostilities persist near border areas, underscoring the fragility of implementation (UN, 2025).

Post-signing reporting pointed to fresh clashes and public accusations of violations, signalling that enforcement, verification, and third-party monitoring are the accord’s immediate tests.

Political and security context

US officials framed the agreement as part of a broader pivot toward commerce-led engagement in Africa, linking peace to investment, trade corridors, and supply-chain resilience. However, parallel mediation tracks and the presence of non-signatory armed groups complicate the transition from diplomatic text to durable security on the ground. Early reactions suggest deterrence remains uneven and confidence highly conditional.

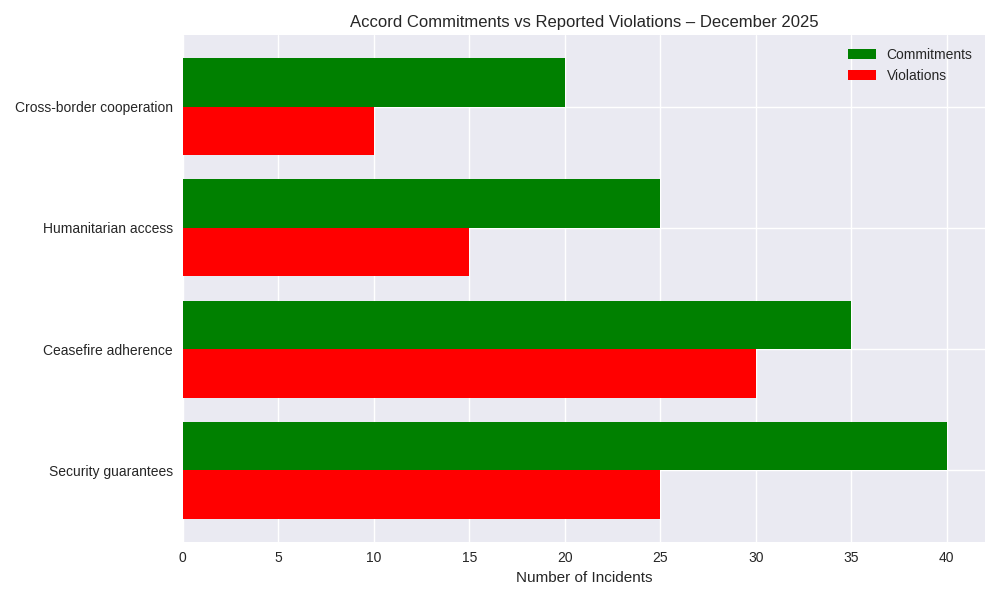

Peace accord commitments vs violations chart with North Kivu conflict nodes and de‑escalation corridor map.

Key insight: The visual shows that while commitments under the Washington Accords were substantial whereby violations remained high, especially in ceasefire adherence, highlighting fragile enforcement. Conflict nodes in North Kivu overlap with humanitarian corridors, meaning instability directly threatens aid delivery and regional trade.

Bar chart of DRC–Rwanda peace accord commitments vs violations across security, ceasefire, humanitarian, and cross‑border cooperation.

Major Insights from the Graph

Security guarantees vs. violations: Commitments (40) outpaced violations (25), suggesting partial compliance. Yet the gap is narrower than expected, showing enforcement challenges.

Ceasefire adherence: Violations (30) nearly matched commitments (35), indicating the ceasefire is the weakest pillar of the accord. This undermines confidence in DDR (disarmament, demobilization, reintegration) programs.

Humanitarian access: Commitments (25) were higher than violations (15), showing relatively better compliance. Still, violations here directly impact aid delivery to civilians.

Cross-border cooperation: Lowest commitments (20) and violations (10), reflecting limited progress but also fewer flashpoints compared to internal ceasefire issues.

Implications

Fragile peace: High violation rates in ceasefire adherence suggest relapse risk. Without stronger monitoring, the accord may fail to stabilize eastern DRC.

Humanitarian risk: Aid corridors intersect with conflict zones, raising insurance premiums and deterring NGOs from scaling operations.

Business impact: Mineral supply chains (cobalt, 3T minerals) remain vulnerable to disruption. Firms will need conflict-sensitive sourcing and diversified logistics.

Policy challenge: Enforcement gaps demand third-party monitoring (UN, AU) and incentives for compliance. Without this, commerce-led engagement will stall.

Key takeaway: The visual confirms that while commitments are ambitious, violations remain too high to guarantee stability. For businesses and policymakers, this means planning for volatility, embedding resilience in supply chains, and pressing for stronger enforcement mechanisms.

What Is the Kenya–US Health Cooperation Framework (2026–2031)?

Scope and funding

Kenya and the US signed a five-year, KSh208 billion health cooperation framework designed to shift aid from NGOs to state institutions, accelerate domestic financing, and align donor support with national reforms. The Ministry of Health published the full 37-page agreement, highlighting compliance with Kenya’s Data Protection Act (2019) and Digital Health Act (2023).

Legal challenges and sectoral allocations

Kenyan courts subsequently issued conservatory orders temporarily suspending implementation, pending petitions on data privacy, ratification procedures, and public participation. This has introduced uncertainty for procurement timelines and program rollout under Universal Health Coverage initiatives.

Preliminary allocation disclosures indicate HIV services will receive the largest funding share in 2026, with planned increases in domestic financing through 2031, placing heightened scrutiny on fiscal controls and delivery capacity.

Kenya–US Health Deal Allocations by Category (2026-2031)

Kenya–US health funding allocations 2026–2031 chart showing HIV services, lab systems, and treatment commodities growth.

Key insights from Kenya–US Health Allocations 2026–2031:

Funding Trends

Overall Growth: Total U.S. health allocations to Kenya steadily increase year by year from 2026 to 2031.

HIV Services (Blue): Largest share of funding across all years, reflecting continued prioritization of HIV response.

Laboratory Systems (Orange): Moderate but steady growth, highlighting emphasis on strengthening diagnostic infrastructure.

Treatment Commodities (Green): Noticeable increase over time, suggesting scaling up of essential medicines and supplies.

Strategic Implications

Shift Toward Systems Strengthening: The rising allocations for lab systems and commodities show a pivot from aid dependency toward building Kenya’s health system capacity.

Universal Health Coverage (UHC) Support: The funding aligns with Kenya’s UHC goals, ensuring broader access to treatment and diagnostics.

Partnership Stability: The consistent upward trend signals long-term U.S. commitment to Kenya’s health sector.

Risk Assessment and Scenarios for Kenya and DRC- Rwanda in 2026

Congo - Rwanda accord

Fragility risk: Continued hostilities and violation claims could trigger localized escalation and erode confidence in DDR and monitoring mechanisms.

Enforcement gap: Non-signatory militias, contested control zones, and limited verification capacity elevate relapse risk without credible third-party oversight.

Political volatility: Commerce-first messaging is constructive but vulnerable to security reversals, electoral pressures, and cross-border tensions.

Kenya - US health deal

Legal and governance risk: Court suspensions cloud timelines for data transfers, procurement, and disbursements, affecting vendors and implementers.

Data protection risk: Despite statutory assurances, cross-border data use remains a reputational and compliance exposure without DPIAs, localization options, and regulator clarity.

Operational risk: Redirecting funds to state systems requires strong fiscal controls, supply-chain integrity, and performance monitoring, especially for high-visibility HIV programs.

Regional Context Beyond Core Deals

Africa’s 2026 outlook is shaped not only by high-profile agreements but also by macro, energy, and fiscal dynamics across key regions.

West Africa: Nigeria

Fiscal Reforms: Removal of fuel subsidies, exchange-rate unification, and higher revenue collection.

Risks: Inflation, FX volatility, and social resistance.

Implications: Market-sensitive reforms create opportunity but with execution risk. Regional spillovers affect ECOWAS trade and remittances.

Southern Africa: South Africa

Energy Crisis: Load shedding persists, private generation grows, but transmission bottlenecks remain.

Implications: Industrial production, supply chains, and insurance costs are impacted; investment is bifurcated toward self-sufficient firms.

East Africa (Beyond Kenya)

Trends: Infrastructure-led growth continues in Ethiopia and Tanzania but is debt-sensitive.

Implications: Procurement delays, FX shortages, and fiscal constraints create selective investment opportunities.

North Africa

Egypt and Morocco: Relative political stability but exposed to external financing pressures and climate stress.

Implications: Lower security risk but macro sensitivity is elevated, requiring careful investor monitoring.

Africa 2026 regional risk scorecards with investment impact and risk ratings

Legend:

1 = Low risk / high execution capacity 5 = High risk / fragile execution

Economic and Business Impact: What Africa’s 2026 Deals Mean for Trade, Investment, and Risk

Supply chains and commodities

Great Lakes minerals: Sustained peace could stabilize cobalt and 3T mineral logistics; renewed violence would raise insurance premiums, security surcharges, and route-diversion costs.

Compliance exposure: Firms operating in eastern DRC face elevated due-diligence requirements tied to conflict-sensitive sourcing and beneficiary vetting.

Health markets and procurement

Market restructuring: Kenya’s shift to state-led financing reshapes supplier relationships and may reduce NGO-led channels, affecting payment cycles and audit regimes.

Data services: Health-tech and informatics providers must align with national data laws; cross-border analytics will require enhanced contractual and regulatory safeguards.

Finance and insurance

Risk pricing: Underwriters will track DDR progress, border incidents, and court rulings in real time, directly influencing premiums for logistics, health procurement, and PPPs.

The Stakes Ahead

2026 is a decisive year for Africa’s risk and investment trajectory. If governments can translate peace accords, fiscal reforms, health financing shifts, and energy policies into credible enforcement and delivery, the payoff will be lower risk premiums, more stable supply chains, and longer-term capital commitment.

If execution falters,through renewed conflict in eastern DRC, prolonged legal uncertainty in Kenya, reform fatigue in Nigeria, or persistent energy failures in South Africa, the result will be higher insurance costs, delayed investment, and a reversion to short-term, risk-averse capital.

The outcome will be determined not by ambition or diplomacy, but by follow-through at courts, checkpoints, grids, and public institutions.

What Investors Need to Know

1.Execution risk dominates the investment case Peace accords (DRC–Rwanda), health financing reforms (Kenya), fiscal adjustments (Nigeria), and energy reforms (South Africa) are all directionally positive. However, weak enforcement, court interventions, infrastructure bottlenecks, and political pushback create volatility across sectors.

2. Risk is uneven and increasingly priced in real time

Eastern DRC and South Africa remain high-risk operating environments due to security and energy constraints. Kenya and Nigeria present medium-high risk, where reforms are credible but legally and politically exposed. North Africa offers lower security risk but higher macro and external financing sensitivity.

3.Supply chains and cash flow are the primary pressure points

Minerals (cobalt, 3T) face disruption from insecurity and insurance repricing. Health procurement and digital services face delays, compliance costs, and data governance exposure. Energy unreliability and FX volatility directly affect margins, timelines, and financing costs.

4. Resilience is now a competitive advantage

Investors with diversified logistics, flexible contracts, localized data strategies, and strong compliance systems will outperform. Passive exposure to “Africa growth” narratives without mitigation will underperform.

Investor takeaway: Africa remains investable in 2026, but only selectively, with active risk management and jurisdiction-specific strategies.

What Policymakers Need to Know

1.Agreements without enforcement erode trust

The DRC–Rwanda accord risks losing credibility without independent monitoring and consequences for violations. Kenya’s health reform agenda faces reputational risk if legal and data governance issues are not resolved transparently.

2.Legal clarity is now a macro-stability issue

Court suspensions, regulatory ambiguity, and opaque ratification processes delay investment and raise sovereign risk premiums. Predictable legal pathways are as important as fiscal or security reforms.

3.State capacity is the binding constraint

Shifting financing to government systems (Kenya, Nigeria) increases ownership but also exposes weaknesses in procurement, fiscal controls, and service delivery. Energy and infrastructure failures (South Africa) impose economy-wide costs.

4.Investor confidence is conditional

Markets reward reform intent only when paired with verifiable implementation milestones. Poor execution now results in higher insurance premiums, delayed financing, and reduced policy space later.

Policy takeaway: In 2026, credibility is earned operationally, through enforcement, institutions, and transparency not diplomatically.

Strategic Takeaway: What This Means for Africa’s 2026 Risk and Investment Outlook

Execution over agreements: Implementation determines real outcomes.

Embed resilience: Conflict-sensitive sourcing, flexible contracts, and contingency planning are essential.

Monitor real-time indicators: Security incidents, court rulings, FX, and energy metrics.

Calibrate regionally: Nigeria (fiscal), South Africa (energy), East Africa (procurement), North Africa (macro).

Opportunity is conditional: Governance, institutional capacity, and enforcement drive returns.

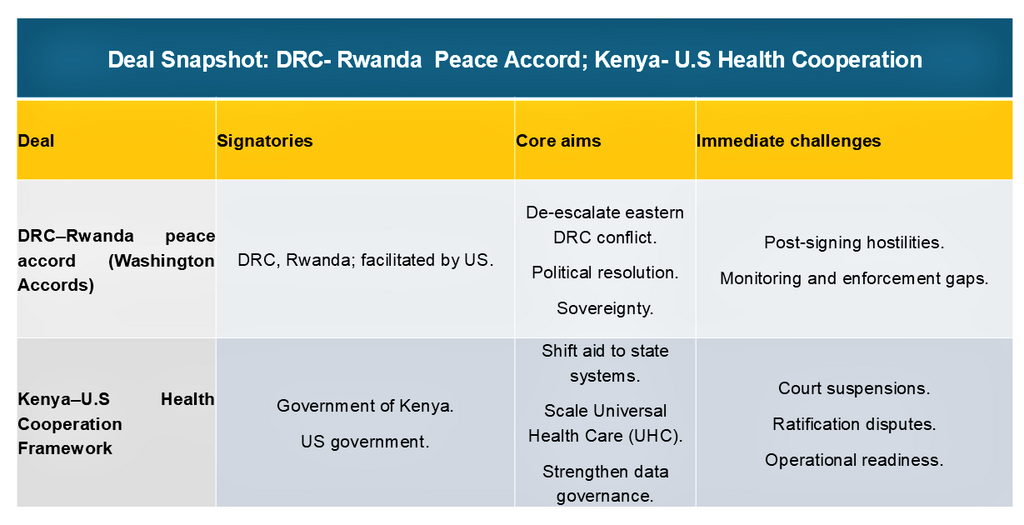

Deal snapshots

DRC–Rwanda peace accord vs Kenya–US health cooperation table with aims and challenges.

Frequently Asked Questions (FAQs)

1: What is the DRC–Rwanda peace deal’s significance for 2026?

Reduces eastern DRC conflict, but fragile enforcement maintains high DDR and supply-chain risk.

2: How does Kenya’s health deal affect businesses?

Procurement channels shift; compliance burdens increase; timelines are uncertain.

3: What should investors monitor in Africa 2026?

Ceasefire compliance, DDR progress, court rulings, FX, energy reliability, and regulatory clarity.

4: Which countries present the highest operational risk in 2026?

DRC/Rwanda and South Africa (risk score 5), followed by Kenya and Nigeria (risk score 4).

An analysis of the immediate failures, the looming gun law reforms, and the Australia's confrontation with rising antisemitism.

On December 14, 2025, Australia was shaken by a mass shooting at Sydney’s Bondi Beach during a Hanukkah celebration. Two gunmen, Sajid Akram (50) and his son Naveed Akram (24), opened fire on a crowd of nearly 1,000 people, leaving 15 dead and more than 40 injured (USA today). This marked the worst mass shooting in Australia since 1996 and triggered nationwide debates on antisemitism, counterterrorism, and gun control.

Bondi Beach Massacre 2025: Security Crisis and Terrorism Analysis

The gunmen opened fire from an overpass while shouting extremist slogans. One of the attackers was killed by police, while the other was critically injured.

Among the victims were children and the elderly, with vigils held at Bondi Pavilion to honor the lives lost.

Australian Government Response to Bondi Beach Shooting

Prime Minister Anthony Albanese condemned the attack as an “act of evil antisemitism, terrorism.” Over 300 police officers were deployed to Sydney, and urgent discussions on tougher gun laws have been initiated.

The attack has also intensified national conversations about rising antisemitism in Australia, particularly amid recent extremist rhetoric and hate crimes.

Bar chart comparing fatalities and injuries in major Australian mass shootings from Port Arthur, Monash and Bondi Beach (1996 - 2025).

Key Insights from the graph:

Port Arthur Remains the Deadliest: The 1996 Port Arthur massacre remains the deadliest incident shown, with 35 fatalities. It is the only event on the chart where the number of deaths exceeds the number of injuries.

Bondi Beach (2025) Recorded the Highest Injuries: While it had fewer fatalities than Port Arthur, the 2025 Bondi Beach incident resulted in the highest number of injuries recorded among these major events (40 injuries).

Significant Total Casualty Comparison: The 2025 Bondi Beach incident is the most significant mass casualty event in this comparison since 1996.

Long Intervals Between Major Events: The chart illustrates a significant 23-year gap between the 2002 Monash University shooting and the 2025 Bondi Beach incident, highlighting that such large-scale "major" incidents have historically been rare in Australia.

Scale of the Monash Incident: Compared to the other two, the 2002 Monash incident was much smaller in scale, resulting in 7 total casualties (2 deaths, 5 injuries), making it a significant but much lower-impact outlier on this specific list of major shootings.

The Bondi Beach shooting is now considered the deadliest mass shooting in Australia in nearly three decades.

Trends in Australian Mass Shootings

Over time, Australian mass shootings have shown a shift toward higher injury counts relative to fatalities, potentially reflecting changing attack tactics.

Antisemitism is on the rise nationwide, and this attack has renewed calls for stronger measures to combat hate crimes and extremist violence.

Bar chart ranking Global Antisemitic Attitude Index 2025: Kuwait & West Bank Gaza highest at 97%, Indonesia 96%, global average 46%, lowest Sweden 5%.

Key Takeaways From Global Antisematic Attitude Index Chart

Highest Index Levels:The top of the list is dominated by the Middle East and North Africa (MENA) region, with the West Bank & Gaza, Kuwait, and Indonesia recording levels above 95%.

Global Benchmark: Australia’s score of 20% is significantly lower than the Global Average (46%), but it remains more than double that of other Western nations like the UK (9%), USA (9%), and Sweden (5%).

Australia's Trajectory:While Australia ranks relatively low in terms of general population attitudes compared to the global scale, the 317% increase in reported incidents over the last year (following events like the 2025 Bondi Beach tragedy) indicates a sharp rise in active extremism despite a lower general index score

Global Context: How Australia Compares Internationally

Mass Shooting Frequency Comparison:

Australia: 1 major event per decade (average since Port Arthur).

United States: 600+ mass shootings annually (2020-2024 average).

Canada: 2-3 significant events per decade.

United Kingdom: 1 major event every 15 years.

New Zealand: Christchurch 2019 prompted major reforms.

Policy Response Comparison:

Australia (1996): Rapid, comprehensive reform post-Port Arthur.

New Zealand (2019): 72-hour response with firearm buyback.

United Kingdom (1996): Strict handgun bans after Dunblane.

Canada (2020): Assault weapon ban after Nova Scotia attacks.

United States: Incremental state-level changes, no federal consensus.

Economic and Social Impact of the Bondi Beach Massacre

1. National Security and Counterterrorism Concerns. The massacre has reignited debates over gun laws, antisemitism, and counterterrorism (ABC News). Australia may face heightened scrutiny of its security framework and pressure to tighten firearms regulation.

2. Social Impact and Public Fear. The attack has heightened fear among Sydney residents and businesses, increased reputational risk, and intensified concerns within Jewish communities nationwide.

3. Consumer Confidence and Economic Sentiment. Consumer sentiment fell by 9% in December 2025, driven by inflation concerns and compounded by security fears following the Bondi Beach attack.

Policy Recommendations: Preventing Future Attacks

Immediate Actions (0-6 Months):

National Security Review: Independent inquiry into intelligence failures.

Firearm Registry Overhaul: Real-time tracking system implementation.

Public Event Guidelines: Mandatory security assessments for gatherings >500 people.

Hate Crime Legislation: Strengthened penalties and reporting requirements.

Medium-Term Reforms (6-24 Months):

Community Policing Expansion: 500 additional officers for community engagement.

Mental Health Integration: Mandatory reporting to firearm registries.

Education Curriculum: National program on extremism prevention.

International Cooperation: Enhanced intelligence sharing with Five Eyes partners.

Long-Term Strategy (2-5 Years):

Technology Investment: AI monitoring of online extremist content.

Social Cohesion Programs: $100 million annual funding for community integration.

Research Institute: Australian Centre for Extremism Studies establishment.

Legislative Review: Comprehensive review of all counter-terrorism laws.

The Road Ahead After the Bondi Beach Shooting: Australia's Security Crossroads

The Bondi Beach Massacre of 2025 represents a critical inflection point for Australian security policy, social cohesion, and counter-terrorism strategy. The attack exposes vulnerabilities in intelligence sharing, public event security, and online radicalization monitoring.

Three critical lessons emerge:

Intelligence Reform Needed: Australia's security apparatus must adapt to evolving domestic extremism threats beyond traditional categories.

Firearm Regulation Gaps: The 1996 Port Arthur reforms require updating for digital age challenges including online sales and weapon modification.

Social Cohesion Investment: Addressing root causes of radicalization requires sustained investment in community integration and counter-extremism education.

Bottom Line

The response to the Bondi Beach Shooting issue will test Australia's ability to balance security imperatives with civil liberties, rapid response with thoughtful reform, and immediate trauma with long-term healing. The decisions made in 2025-2026 will shape Australian security policy for the coming generation.

Bondi Beach Massacre 2025: FAQs on Australia's Deadliest Shooting Since Port Arthur

1. What happened at Bondi Beach in December 2025?

On December 14, 2025, during a Hanukkah celebration at Sydney's Bondi Beach, two gunmen, Sajid Akram (50) and his son Naveed (24), opened fire from an overpass, killing 15 people and injuring over 40. It was Australia's deadliest mass shooting since the 1996 Port Arthur massacre and was declared an act of antisemitic terrorism by Prime Minister Anthony Albanese.

2. What weapons were used in the Bondi Beach attack and were they legal?

The attackers used illegally modified semi-automatic rifles obtained through black market channels, exploiting a significant loophole in Australia's National Firearms Agreement established after Port Arthur.

3. How is Australia changing gun laws after the Bondi Beach shooting?

The attack has prompted urgent parliamentary debate on four key reforms: A real-time national firearms registry (currently 24-hour delay); Tighter border controls on firearm parts; Increased penalties for illegal modifications (up to 20 years imprisonment) and Mandatory mental health reporting to licensing authorities. measures aimed at closing gaps exposed by the attack.

4. Was the Bondi Beach attack related to rising antisemitism in Australia?

Yes. The attackers targeted a Jewish celebration while shouting extremist slogans, amid documented rising antisemitism, a 60% increase in incidents reported in 2024. The attack has triggered a $25 million security package for Jewish communities, mandatory Holocaust education in schools, and enhanced hate crime legislation.

5. How does the Bondi Beach casualty count compare to Port Arthur?

While Port Arthur (1996) had higher fatalities (35 vs. 15), Bondi 2025 recorded Australia's highest injury count (40+) in any mass shooting. This reflects both changes in attack methodology (urban crowded space vs. isolated tourist site) and improvements in emergency medical response that saved lives but left many severely injured.

European markets entered December with inflation trending near the ECB’s 2% target, reinforcing expectations of a steady policy stance. The European Commission’s Autumn 2025 forecast highlighted modest growth resilience despite trade frictions, while LGT’s December outlook noted euro area inflation stability contrasted with weaker Swiss growth.

Sentiment indicators such as the MacroMicro European Fear & Greed Index showed mixed readings, reflecting cautious optimism amid disinflation and stable credit conditions.

Cyclicals: Autos and industrials showed selective strength which means that gains were not broad-based across all cyclicals, but concentrated in pockets where order books, export demand, or pricing power remained resilient.

Rates & credit: Sovereign yields stabilized as inflation cooled; credit spreads remained contained.

FX: The euro traded in tight ranges after CPI data confirmed stability.

European macroeconomic drivers

A pie chart - European macroeconomic drivers breakdown by category and impact share (Dec 1–10, 2025).

Label: Allocation reflects typical market focus around calendar-flagged releases and policy events that carry higher volatility impact in European trading. Source: ECB – Macroeconomic Projections

Key Insights from Chart: European Macro Drivers Breakdown (Dec 1–10, 2025)

Inflation prints (30%) are the top macro driver, followed by central bank decisions (25%).

PMIs and industrial data (20%) and labor/earnings (15%) also play significant roles.

Credit spreads/liquidity (10%) are the least influential in this period.

Implications ofEuropean Macro Drivers Breakdown:

Market sensitivity to inflation and ECB signals remains high, any deviation from expected CPI/HICP or hawkish/dovish tone could trigger volatility.

Industrial and labor data are gaining relevance, suggesting investors are watching real economy indicators more closely.

Liquidity concerns are subdued, indicating stable credit conditions for now.

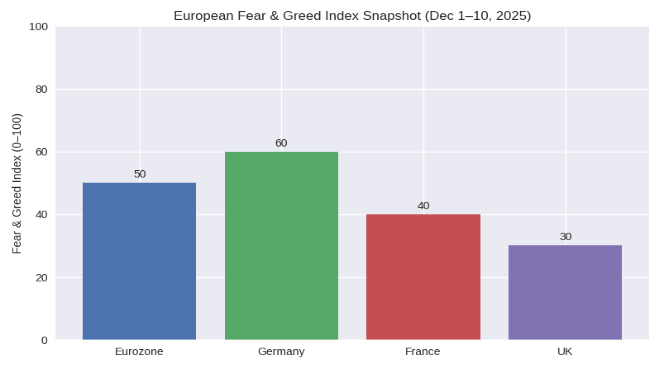

European Market Fear & Greed Index snapshot

Bar chart – European Fear & Greed Index comparison for Eurozone, Germany, France, and UK (Dec 1–10, 2025).

Label: Higher bars = more “greed” (optimism); lower bars = more “fear” (pessimism). Source: MacroMicro – European Countries Fear & Greed Index

Key Insights from the Chart : European Market Fear & Greed Index snapshot

Germany (60) shows the highest investor optimism ("greed").

Eurozone (50) sits at neutral sentiment.

France (40) and UK (30) reflect rising investor caution or "fear."

Implications ofEuropean Market Fear & Greed:

Germany’s bullish sentiment may drive short-term equity inflows and sector rotation into growth stocks.

UK’s elevated fear suggests potential capital outflows or defensive positioning, possibly due to macro uncertainty or political risk.

Divergence across regions highlights the need for country-specific strategies rather than a pan-European approach.

Quick takeaways

Disinflation supports stability: Inflation near target underpins predictable ECB policy.

Asia is entering a new phase of economic transformation, driven by decades of export-led growth, market liberalization, and human capital development. Through reforms that promoted exports, opened markets, and built skilled human capital, the region moved from low-income to middle-income status. Asia is the home to the world’s largest and fastest-growing middle-class consumer base, shaping global demand, investment strategies, and digital innovation. Understanding how this shift began, and where it is headed remains key to capturing the $15 trillion Asia consumption opportunity emerging by 2030, (Private Wealth Management Association).

Asia’s Reform-Driven Rise and the New Consumer Landscape

Asia’s transformation was the result of economic reforms, export-oriented policies, and integration into global supply chains.

China’s Dual Track Strategy

China’s rise was anchored by the dual-track reform strategy, including the Household Responsibility System (1978), which increased rural incomes and food production. Gradual market liberalization encouraged competition in exports and light industries such as textiles, electronics manufacturing, and food processing (Center for International Knowledge on Development, 2020). Pro-investment policies opened doors to foreign multinationals and supported large-scale infrastructure investment in transport, telecommunications, and education—building the world’s largest manufacturing workforce.

The Four Asian Tigers

Hong Kong, South Korea, Singapore, and Taiwan executed rapid export-led growth.

Singapore’s Economic Development Boardattracted foreign industries and innovation centers.

South Korea invested heavily in heavy and chemical industries, later liberalizing finance and advancing technology.

All four economies invested in education to align skills with labor market needs and productivity gains.

ASEAN Economies

Indonesia, Vietnam, and the Philippines adopted trade openness, private investment promotion, and financial inclusion to support the rising ASEAN middle class.

In 2024, Foreign Direct Investment (FDI) remained a major driver of Asia’s economic growth, strengthening industrialization, technology adoption, and the expansion of the Asian middle class. China, the Four Asian Tigers, and Southeast Asian economies leveraged FDI inflows to modernize industries and accelerate their integration into global value chains, setting the stage for Asia’s second consumption wave.

These reforms shared a common theme: market-based systems, open trade, and investment in education and infrastructure. This boosted productivity, created millions of jobs, and lifted people out of poverty into a growing middle-class consumer market.

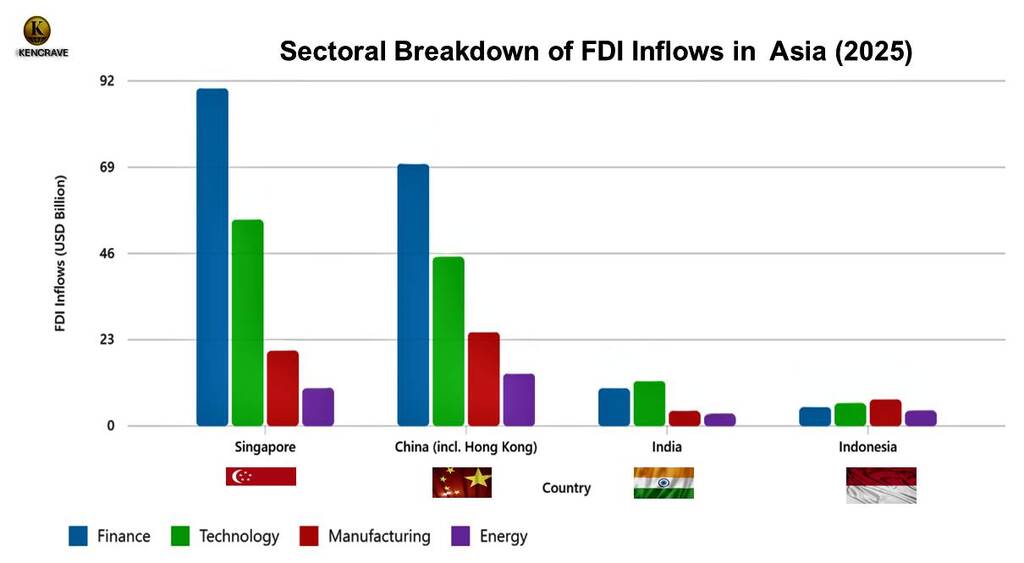

2025 FDI inflows by sector in Asia in Finance, Technology, Manufacturing, Energy across Singapore, China, India, Indonesia.

Key Insights from the graph: FDI Inflows by Sector in Asia (2025)

Singapore dominates Finance FDI (est. $92B), reinforcing its role as Asia’s financial hub.

China (incl. Hong Kong) attracts strong investment in both Finance and Technology, showcasing its dual strength in capital and innovation.

India’s FDI is tech-focused, while Indonesia shows balanced inflows, suggesting diversified sectoral appeal.

Implications: Investors prioritize financial and tech sectors in developed markets, while emerging economies attract broader interest.

By 2025, Asia’s growth drivers shifted toward digital adoption, consumer behavior, and sustainability-driven consumption. Today’s Asian middle class is connected, diverse, and values-driven, making it one of the world’s most complex and influential consumer segments. Updated 2030 projections highlight how businesses can position themselves within the $15 trillion Asian consumer market.

Asia’s 2030 Middle-Class Blueprint: The $15 Trillion Opportunity

Forecasts indicate that Asian consumer spending will exceed $15 trillion by 2030.

A 3.5 Billion-Person Middle Class

The World Economic Forum expects the global middle class to reach 5.5 billion by 2030, with Asia accounting for over 3.5 billion, making it the world’s epicenter of consumption (World Economic Forum).

Emerging Growth Hubs

While China remains a major market, Southeast Asian economies such as Vietnam, Indonesia, and the Philippines, among the fastest-growing emerging consumption hubs.

Asian consumers are evolving beyond traditional “premium” preferences toward:

Sustainability-driven consumption.

Digital-first shopping.

Frictionless commerce powered by super apps and integrated payment systems

Sustainability and Frictionless Commerce: The New Consumer Drivers

The Sustainability Imperative

Over 65% of urban Asian consumers under 40 identify as conscious consumers, seeking eco-friendly, traceable, and ethical products. Sustainability has shifted from niche to mainstream as consumers expect recycling, carbon neutrality, and traceability.

Frictionless Shopping

Asian markets are undergoing a transformation towards contextual commerce, where consumers can discover, purchase, and receive products instantly. The super app ecosystem continues to evolve into an integrated digital commerce infrastructure.

Untapped Markets: Gen Z Alpha and the Silver Economy

Gen Alpha: The Phygital Natives

Born after 2010, Gen Alpha represents Asia’s first true digital natives. They move seamlessly between digital and physical (“phygital”) experiences, adopt virtual identities, and expect AI-driven personalization and immersive commerce.

The Silver Economy

Asia’s population of individuals aged 60 years and above is projected to exceed 1.3 billion by 2050, creating a booming Silver Economy across:

Wellness tourism.

Smart living solutions.

Health technology.

Retirement fintech.

Assisted living.

Japan, Hong Kong, and South Korea lead in aging demographics, while China, Thailand, and Armenia are entering mid-stage transitions. Indonesia, India, and Bangladesh will experience accelerating aging through the next decade.

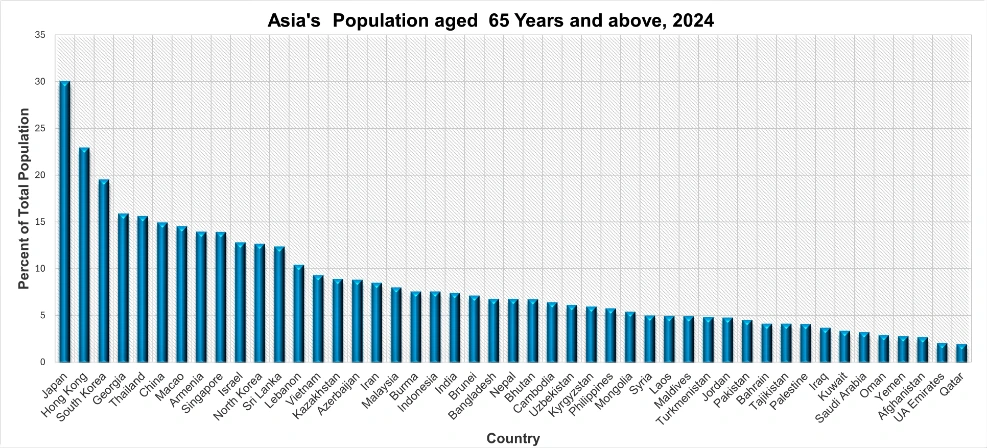

The chart below shows the percentage of the population aged 65 and above across Asia in 2024. Source: The Global Economy

2024 bar chart showing the percentage of the population aged 65+ years across Asian countries, led by Japan.

Key insights from the graph: Asia's Aging Population (2024)

Japan leads Asia with nearly 30% of its population aged 65+, signaling advanced aging and potential labor shortages.

Hong Kong, South Korea, and Georgia follow closely, indicating similar demographic pressures.

Qatar and other Gulf nations show minimal elderly populations, reflecting younger migrant-heavy demographics.

Implications: Rising healthcare demand, pension strain, and shifting consumer needs toward eldercare and wellness sectors.

These trends mark the rise of the silver economy and will shape spending patterns, service needs, and long-term market strategies across Asia.

The 2030 Digital Infrastructure: AI, Web3, and the Sovereign Consumer

Asia’s digital innovation is accelerating through AI, Web3, and digital identity ecosystems.

AI as a Personal Assistant

Generative AI is reshaping how consumers discover products, with AI set to influence 40% of online sales in leading Asian markets by 2027.

Web3 Consumer Trends

Although still emerging, Asia is becoming a global leader in Web3 adoption, including:

Blockchain-based rewards.

Token-gated communities.

Digital asset ownership.

Decentralized identity management.

Southeast Asia currently leads global participation in Web3 ecosystems.

Challenges for Web3 Adoption in Asia

Web3 growth faces several major obstacles:

Fragmented regulations.

Conflicting data protection laws.

Complex cross-border compliance.

Evolving crypto governance frameworks.

China restricts crypto trading, while Singapore and Hong Kong are building regulated Web3 hubs. India’s stricter data rules challenge decentralized network models.

Key regulatory issues include:

Token classification inconsistencies.

AML and KYC requirements.

Blockchain’s conflict with data deletion rights.

Data localization vs. decentralized nodes.

Web3’s expansion will depend on regulatory clarity, consumer demand, and innovations that align decentralization with national data rules.

Actionable Strategies for Businesses in 2030 Asia

To compete effectively, companies must shift from static marketing to dynamic personalization and localized strategy development.

Dynamic Personalization powered by AI. Use AI to adapt customer profiles in real-time, considering life stages, locations, and values like sustainability.

Phygital integration across retail channels. Combine online and offline channels for seamless browsing, in-store pickup, and follow-up engagement.

Blockchain traceability to validate sustainability. Use blockchain or traceable data to validate sustainability claims.

ASEAN-first localization for products and operations. Localize operations, sourcing, and products to meet cultural and regulatory requirements.

Data-driven consumer insight to navigate diverse markets.

Policy Recommendations for Asia's Sustainable Growth

Governments must build an enabling ecosystem through:

Digital infrastructure for AI, cloud computing, and cross-border e-commerce.

Stable regulatory frameworks for digital payments and Web3 assets.

Investments in education, upskilling, and advanced manufacturing.

SME support through incentives and digital platforms.

Green technology and sustainable production policies.

Comprehensive plans for aging populations

Key Takeaways for Asia's 2030 Market Success

Asia will house the majority of the global middle class by 2030.

Digital habits, sustainability, and rising incomes will drive growth.

Gen Z Alpha and the Silver Economy define future market demand.

AI and Web3 will transform shopping, identity, and product discovery.

Companies that localize, embrace sustainability, and build integrated digital systems will lead.

Policymakers must advance regulation, infrastructure, and education to support Asia’s next growth wave.

FAQs: Key Insights on Asia’s 2030 Middle-Class Market, Digital Trends, and $15 Trillion Consumption Shift

1. Why is Asia projected to reach $15 trillion in consumer spending by 2030?

Because of rapid middle-class expansion, rising incomes, digital adoption, and sustained investment in manufacturing, technology, and infrastructure.

2. Which countries will drive the fastest middle-class growth?

Vietnam, Indonesia, and the Philippines—alongside steady growth from China, are emerging as key consumption hubs.

3. What are the major consumer trends shaping Asia’s 2030 market?

Sustainability-driven purchasing, frictionless digital commerce, AI-powered personalization, and the rise of “phygital” experiences.

4. Why are Gen Z Alpha and the Silver Economy important for businesses?

Gen Z Alpha demands hyper-personalized, digital-first experiences, while Asia’s aging population fuels growth in healthcare, wellness, fintech, and smart living solutions.

5. What challenges could slow Web3 adoption in Asia?

Fragmented regulations, conflicting data protection rules, and compliance barriers related to decentralization, AML, KYC, and cross-border data governance.

Market Pulse (4th December 2025): African equities stayed strong this week, with 12 of 15 major exchanges recording gains. Year-to-date performance remains robust, with several markets among the fastest-growing globally in 2025 (African Markets).

Catalyst of the Week: The rally was driven by active buying from local institutions and strengthening currencies, which boosted market momentum and attracted additional foreign investment.

Market Pulse: Key Highlights

Broad-based weekly gains across major African exchanges.

Malawi, Ghana, and Zambia continue to dominate global equity returns.

FX appreciation is boosting USD-denominated returns for foreign investors.

Local institutional demand remains a stabilizing force.

Markets with IMF-backed reforms (Egypt, Nigeria) are outperforming risk peers.

Weekly Market Trends (Week Ending 4 December 2025)

Market Performance Overview

Most exchanges recorded positive momentum this week, including:

Nairobi Securities Exchange (Kenya)

Johannesburg Stock Exchange (South Africa)

Ghana Stock Exchange (GSE)

Egypt EGX

Mild pullbacks occurred in Uganda, Malawi, and Morocco after recent rallies.

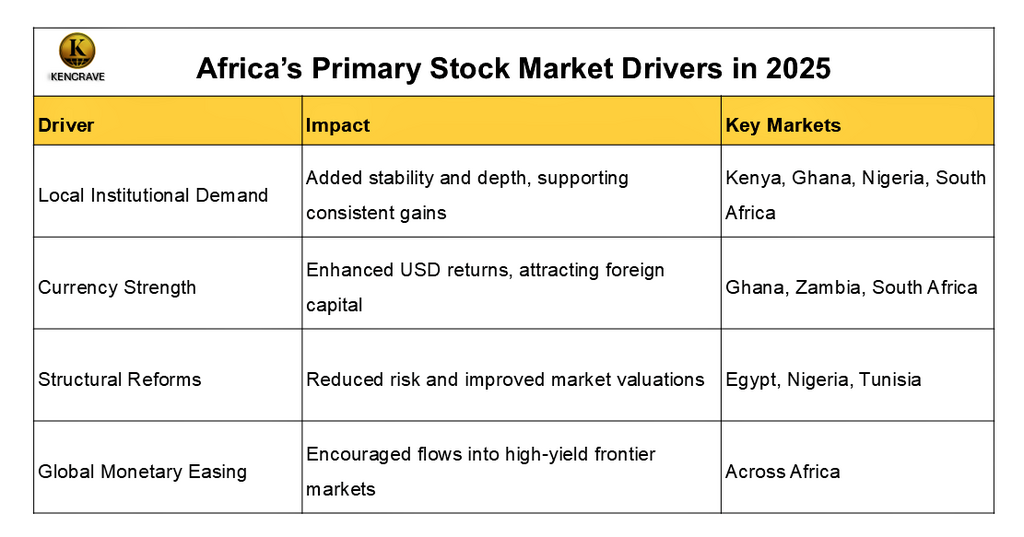

Main Market Drivers

Table showing key drivers of Africa’s 2025 stock market performance: institutional demand, FX strength, reforms, and global monetary easing.

Key Insights:

Domestic institutions are anchoring market stability, especially in larger economies.

Strong local currencies are amplifying returns for foreign investors, making FX-resilient markets more attractive.

Reform-driven markets (like Egypt and Nigeria) are seeing valuation boosts due to improved fiscal credibility.

Global monetary easing is a tailwind for all African markets, enhancing liquidity and investor appetite.

Africa's 2025 Stock Market Top Performers (YTD USD Returns)

Table ranking Africa’s top-performing stock markets in 2025 by YTD USD returns: Malawi, Ghana, Zambia, Egypt, South Africa.

Key insights and observation:

Malawi leads with explosive growth driven by currency stability and strong performance in large-cap stocks.

Ghana and Zambia benefit from macro reforms and commodity-linked optimism.

Egypt’s reform credibility under IMF guidance is translating into solid foreign inflows.

South Africa’s diversified sectors (resources and finance) are fueling steady gains.

Observation: USD returns are higher than local-currency gains, showing that strong local currencies add extra profits for foreign investors

Investment Implications

For Investors

Prioritize liquid markets with reform momentum (Egypt, Ghana, Zambia, South Africa).

FX-stable markets provide dual returns (equity appreciation + currency gains).

Consider selective exposure to high-growth smaller markets (Malawi, Namibia).

For Policymakers

Sustained FX stability and clear fiscal guidance remain critical for attracting foreign capital.

Transparency in reform delivery directly increases market valuations.

For Analysts

Monitor FX flows, as currency resilience correlates strongly with market inflows.

Expect divergence in 2026 performance depending on reform credibility and commodity exposure.

Forward View: The market is gaining but unevenly, showing that markets backed by steady policies provide more reliable returns, while commodity-dependent markets are riskier and more unpredictable.

2026 Outlook: A Two-Speed African Market

Based on the 2026 outlook for Africa’s equity markets, the high-risk markets are those that lack diversification, carry heavy debt burdens, or are highly sensitive to global monetary shifts.

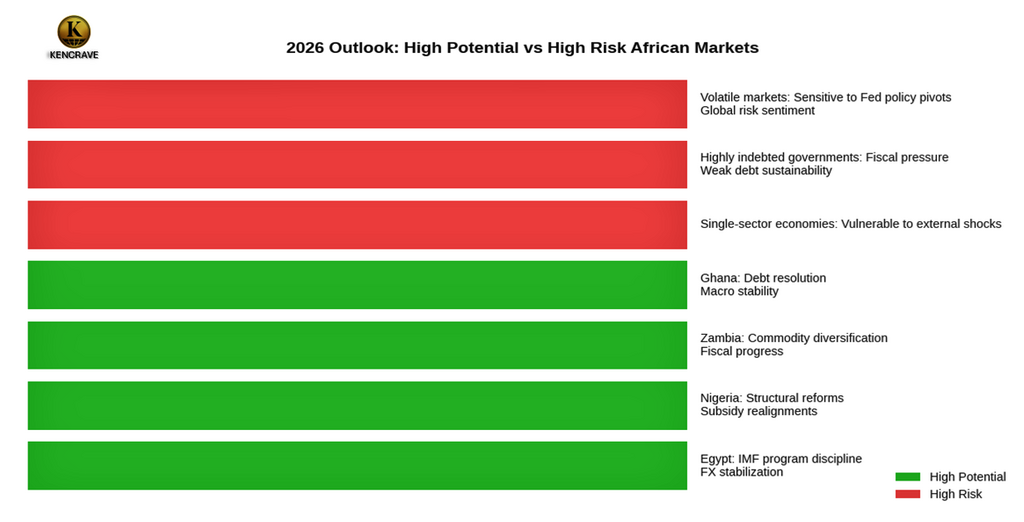

The chart below highlights Africa’s 2026 outlook, contrasting high-potential reform-driven markets with economies at greater risk from debt, single-sector dependence, and global volatility. It offers a clear snapshot of where opportunities and vulnerabilities lie.

A chart showing 2026 African market outlook, comparing high-potential markets with high-risk categories.

Likely Outperformers

Egypt: Strong IMF program discipline and stabilization of the FX regime continue to attract foreign inflows.

Nigeria: Structural reforms, subsidy realignments, and fiscal adjustments position the market for steady recovery.

Zambia & Ghana: Commodity diversification and progress on debt resolution enhance resilience and investor confidence.

Markets at Greater Risk

Single-sector economies: Overdependence on one industry leaves them vulnerable to external shocks.

Highly indebted governments: Fiscal pressure and weak debt sustainability could undermine investor trust.

Volatile markets: Economies sensitive to Fed policy pivots or global risk sentiment may face sharp reversals.

Global Risks to Monitor

Delayed U.S. Federal Reserve rate cuts: Prolonged tight monetary conditions could reduce capital inflows.

Declining global risk appetite: Investors may retreat from frontier markets, dampening liquidity.

Commodity price volatility: Fluctuations in oil, copper, and other exports could destabilize resource-dependent economies.

Strategic Takeaways

Winners will be reform-driven and diversified: Countries combining credible reforms with sectoral breadth are best positioned for sustained growth.

Losers risk policy inertia: Economies that fail to diversify or manage debt effectively may lag behind.

Global headwinds matter: External monetary and commodity cycles will amplify the divergence between outperformers and vulnerable markets.

Bottom Line: Reforms and FX stability remain the strongest predictors of outperformance heading into 2026.

FAQs: Africa's Stock Market Performance in 2025

1. Which African stock markets performed best in 2025?

Malawi, Ghana, Zambia, Egypt, and South Africa led African equity returns in 2025, with Malawi exceeding +250% YTD on FX stability and strong large-cap performance.

2. How did currency movements impact African equity markets?

Currency appreciation boosted USD-denominated gains, especially in Ghana, Zambia, and South Africa, making these markets more attractive to foreign investors.

3. What drove the African equity rally in 2025?

Key drivers include institutional buying, FX strength, structural reforms, improved fiscal discipline, and global monetary easing that increased flows into frontier markets.

4. Which African markets look strong for 2026?

Egypt, Nigeria, Zambia, and Ghana are well positioned due to reforms, diversified exports, and improved macro stability.

A leading global company for Business Solutions , bringing the intriguing global business arena into your space to a business and financial savvy mind.

social media:

Stay In Touch

Don't hesitate. Reach us with these info.

0795046415financialshub01@gmail.comNairobi/Kenya

We create great content everyday. Subscribe to be the first notified when released.

.png)

.png)

%20(2).png)

%20(1).jpg)

.png)

.png)

.png)