What began as a digital protest against Kenya’s Finance Bill 2024 tax hike in Nairobi, has evolved into a transnational youth movement challenging corruption, dynastic politics, and digital repression. The Gen-Z revolution, born in Kenya and now echoing across continents, is reshaping governance, accountability, and ESG priorities in the Global South and beyond.

What Triggered the Gen-Z Protests in Kenya?

The Gen-Z uprising in Kenya erupted in June 2024, triggered by widespread opposition to the Finance Bill 2024, which proposed steep tax increases on essential goods and digital services. Mobilized under the hashtag #RejectFinanceBill, youth-led protests swept across Nairobi, Mombasa, Kisumu, and Eldoret.

The movement was leaderless and decentralized, coordinated via TikTok, X, and encrypted messaging apps (ACCORD).

Protesters cited youth unemployment, rising cost of living, police brutality, and elite impunity as core grievances.

The demonstrations disrupted economic activity, forced parliamenExpand on how digital repression techniques vary by regiontary revisions, and sparked a national reckoning on governance and generational equity.

Though not Kenya’s first protest wave, this was unprecedented in scale, coordination, and digital fluency, marking a new chapter in civic resistance.

How Gen-Z Uses Digital Tools for Civic Mobilization

Kenya’s Gen-Z activists mobilized nationwide protests against the Finance Bill, leveraging digital platforms to coordinate leaderless demonstrations. Their demands were clear: transparency, justice, and an end to elite impunity.

Youth unemployment in Kenya fueling frustration and mass mobilization.

The movement rejected traditional political structures, favoring decentralized, tech-driven activism.

Similar uprisings followed in Nigeria, Ghana, and South Africa, where Gen-Z networks amplified calls for reform.

This digital-first defiance has become a blueprint for civic resistance across Africa, Latin America, and South Asia.

Challenges, Risks, and Opportunities Across Borders

As Gen-Z movements spread, they face a mix of systemic pushback and strategic openings:

Challenges and Risks

Digital repression: Governments in Tanzania, Nepal, and Madagascar have intensified surveillance, internet shutdowns, and platform censorship.

Legal retaliation: Youth leaders in Morocco and Sri Lanka face arrests under vague national security laws.

Fragmentation risk: Leaderless structures can hinder long-term policy engagement and institutional reform.

Opportunities

Global solidarity: Transnational hashtags and encrypted networks foster cross-border learning and support.

Policy leverage: In Nepal, youth pressure led to the resignation of Prime Minister K.P. Sharma Oli.

Civic innovation: In Kenya and Ghana, youth-led civic tech platforms are tracking budgets and exposing corruption.

Digital Repression: How Governments Counter Youth-Led Movements

As youth activism spreads, governments are adopting more sophisticated forms of digital repression. Tactics vary significantly by region.

Africa: Shutdowns and Platform Throttling

Internet shutdowns during protests.

Throttling of social platforms. Government-compelled telecom compliance.

Use of state-aligned influencers to disrupt narratives. These tactics aim to disrupt coordination during peak protest moments.

South Asia: Legal Suppression and Content Removal

Arrests under vague national-security laws.

Takedown requests to social media companies.

Restrictions on VPNs and encrypted platforms.

Monitoring of digital networks.

South Asian governments rely more onlegal tools than outright shutdowns.

Middle East & Authoritarian Regimes: High-Tech Digital Control

Deep packet inspection (DPI).

National firewalls blocking global platforms.

Forced migration to state-monitored apps. Youth activists here focus heavily on circumvention technologies.

Latin America: Information Warfare and Digital Harassment

State-backed bot networks.

Disinformation campaigns.

Targeted online harassment.

Algorithmic manipulation. The goal is to dilute, discredit, and divide activist communities.

ESG Implications of Youth Activism: Governance, Inclusion, and Accountability

Gen-Z’s demands align with core ESG principles, especially in governance and social equity:

Governance: Calls for transparency, anti-corruption, and institutional reform directly challenge ESG laggards.

Social: Youth-led movements highlight exclusion from labor markets, education, and digital rights.

Environmental: Gen-Z activism increasingly intersects with climate justice and sustainability.

Countries with stronger ESG frameworks such as Rwanda and Ghana, have seen more constructive youth engagement. In contrast, ESG-deficient states like Tanzania and Nepal face disruptive protests and reputational risk.

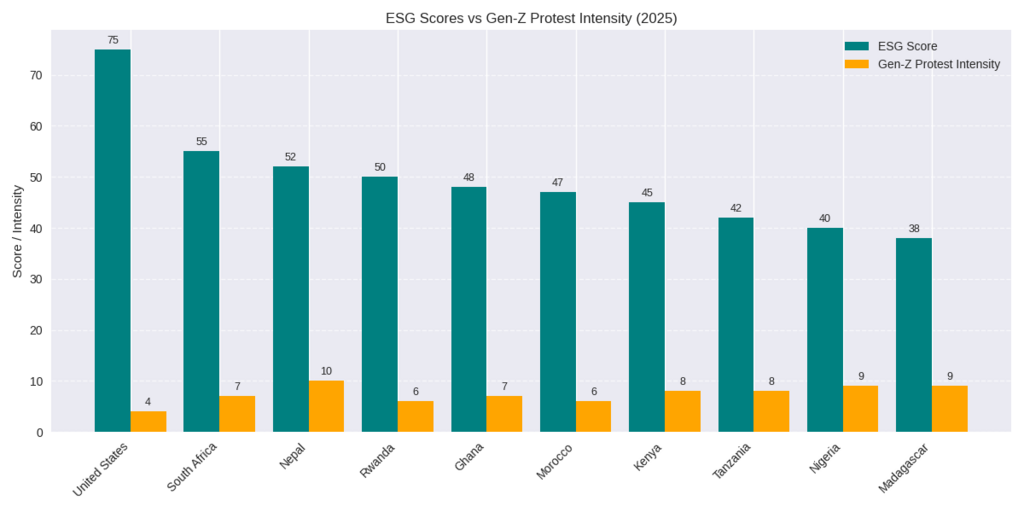

Comparative ESG Scores vs Gen-Z Protest Intensity (2025)

This bar chart compares ESG scores with protest intensity across 10 countries. It reveals a clear pattern: lower ESG scores correlate with higher youth-led unrest.

ESG scores vs Gen-Z protest intensity 2025 bar chart comparing sustainability governance with youth activism across Kenya, Nigeria, South Africa, Rwanda, Ghana, Tanzania, Nepal, Madagascar, Morocco, and United States.

Key insights from the Graph “ESG Scores vs Gen-Z Protest Intensity (2025)”:

Inverse correlation: Countries with lower ESG scores tend to have higher Gen-Z protest intensity, suggesting youth are more vocal in demanding better environmental, social, and governance standards.

United States stands out with the highest ESG score (75) and lowest protest intensity (4), indicating stronger institutional frameworks and possibly more youth satisfaction.

Nepal and Nigeria show high protest intensity (10 and 9) despite moderate to low ESG scores (52 and 40), highlighting youth frustration with governance and sustainability efforts.

Regional Patterns

African countries like Kenya, Nigeria, Madagascar, and Tanzania generally have lower ESG scores (below 45) and high protest intensity (8–9), pointing to systemic governance challenges and active youth movements.

South Africa and Rwanda have moderate ESG scores (50–55) and slightly lower protest intensity (6–7), suggesting some progress in governance but still room for improvement.

Notable Outliers

Madagascar has one of the lowest ESG scores (38) and high protest intensity (9), making it a critical case for reform.

Morocco shows a moderate ESG score (47) and lower protest intensity (6), possibly indicating more stability or less youth mobilization.

Strategic Implications

Youth activism is a signal: High protest intensity may reflect unmet expectations in governance and sustainability, especially among Gen-Z.

Policy opportunity: Countries with high activism and low ESG scores could benefit from targeted reforms to address youth concerns and improve ESG metrics.

Strategic Trajectories: What Stakeholders Must Consider

For Governments: How to Invest in Youth Inclusion

Strengthen civic infrastructure: Fund youth-led platforms, protect digital rights, and ensure transparent institutions.

Integrate youth into policy: Create participatory budgeting, youth parliaments, and innovation grants tied to governance reform.

Studyreform models: Rwanda’s ESG-aligned governance and digital inclusion offer a blueprint for stability and engagement (OECD Rwanda Country Profile).

For Investors and ESG Analysts

Align ESG metrics with youth priorities: Include digital rights, civic participation, and generational equity in ESG scoring.

Monitor transnational activism: Track how digital movements influence policy, elections, and global norms.

For Civil Society and Media

Amplify youth voices: Support independent media and civic tech that elevate Gen-Z narratives.

Build cross-border coalitions: Facilitate regional forums and digital exchanges to sustain momentum.

Path Forward: A Movement, Not a Moment

From Nairobi to Kathmandu, Dar-es-Salaam to Bogotá, Gen-Z is rewriting the rules of engagement, demanding not just reform, but reinvention. Their digital fluency, civic urgency, and strategic coordination are reshaping governance and ESG priorities across continents.

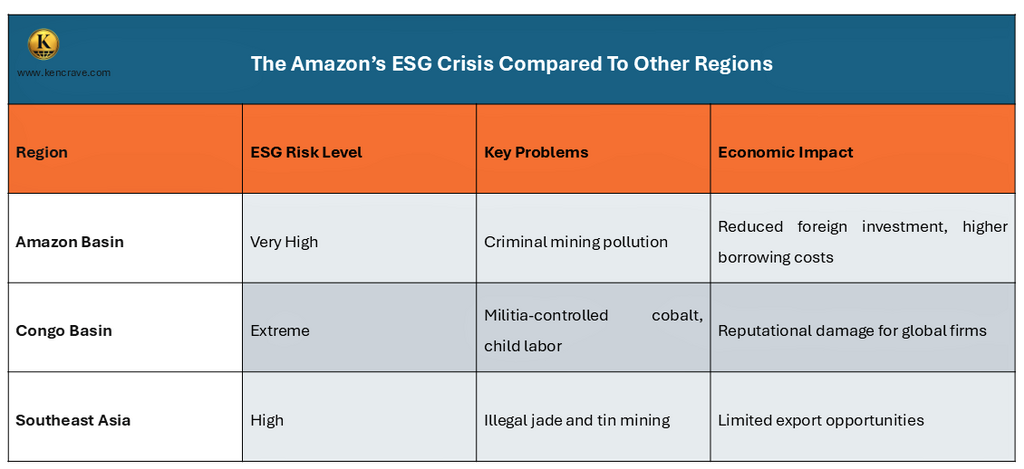

Illegal mining in the Amazon is more than an environmental problem; it’s a multi-dimensional crisis affecting people, economies, and ecosystems. InDecember 2023, a joint Colombian Brazilian task force destroyed 19 illegal gold dredges operating deep in the Amazon rainforest.

These machines were generating nearly $1.5 million worth of gold every month, while contaminating rivers with toxic mercury and displacing indigenous communities who depend on them. As William René Salamanca, Director of the Colombian National Police, stated on 6th December 2023, the mission was essential to “protect the lungs of the world.”

But the problem goes far beyond one operation. Across Brazil, Peru, Colombia, and Venezuela, illegal mining is run by well-funded criminal networks, cartels, and militias.

These operations undermine governments, destabilize local economies, and destroy one of the planet’s most important defenses against climate change. From the colonial mines of Minas Gerais to today’s mercury-contaminated rivers, the patterns of exploitation continue unchecked.

A Legacy of Extraction: From Colonial Plunder to Modern Crisis

For over 500 years, the Amazon and its neighbors have been subjected to resource extraction that prioritizes profit over nature and people. Today’s environmental and social disasters are a direct continuation of that legacy.

Colonial Beginnings: Mining and Oppression (1600s–1800s)

Amazon’s mining problems began in the late 1600s, when the Portuguese started mining gold in regions like Minas Gerais. Forests were cleared, rivers polluted or diverted, and Indigenous people and African slaves were forced into brutal labor. Historical records note:

“Thousands of Indigenous people were forcibly recruited. Hundreds of thousands of African slaves died from hunger, abuse, and isolation in the mines.”

Modern Mining: Chaos and Continued Exploitation (1970s–Today)

Mining didn’t stop after colonial times; it just evolved. The Serra Pelada gold rush in the 1980s saw tens of thousands of garimpeiros (They are small-scale miners who often work illegally for a living) working in dangerous, unregulated open-pit mines.

Today, mining-related deforestation has increased, Indigenous lands are under threat, and mercury pollution continues, a modern echo of colonial exploitation. From the enslaved miners of Minas Gerais to modern garimpeiros, the patterns of the past are still shaping the crises we see in the Amazon today.

Major Mining Companies Operating in South America

Several multinational and regional mining companies operate across South America, extracting minerals such as gold, copper, iron, and zinc. While these companies contribute significantly to national economies, their presence in and around the Amazon creates a complex "gray zone" that indirectly fuels the illegal crisis and compounds the region's environmental stress.

These large-scale operations, while legal, can act as a catalyst for illegal activity in several ways:

Infrastructure and Access: The construction of roads, railways, and ports for major mines opens up previously inaccessible pristine forests, creating pathways for illegal miners, loggers, and land grabbers to follow.

Normalization of Extraction: The dominant presence of industrial mining helps to cement an extractive mindset in regional economies, where the primary perceived path to wealth is through resource removal, discouraging investment in alternative sustainable industries.

"Camouflage" for Illicit Trade: The high volume of legitimate mineral output from a region can provide cover for laundering illegally sourced minerals, as the scale of legal activity makes oversight and tracking more difficult.

The table below outlines key players whose massive operations, while legal, intersect critically with the ecosystems and dynamics described in this report.

Table of major South American mining companies - Vale, Petrobras, Antamina, Yanacocha , detailing operations in iron, copper, gold, and oil across the Amazon region.

The Garimpeiro's Dilemma

"When survival is uncertain, risk becomes a currency, and the mines become home. For those with nothing to lose, the dangerous path to gold can feel like the only path forward."

Driven by extreme poverty and a lack of alternatives, many in the Amazon region turn to small-scale gold mining despite the risks. Their stories reveal a crisis of survival.

“We don’t have other options.” “We aren’t criminals, we are workers.”

These voices show how economic drivers of scarce formal jobs, desire for powerful economic incentives, and lack of sustainable livelihoods result in the last resort for survival.

The Corruption Engine: How Illegality Thrives

This desperate workforce is exploited by a system fueled by corruption. According to the UNODC (2025), illegal mining and mineral trafficking are powered by fraud, corruption, and money laundering.

As the U4 Anti-Corruption Resource Centre notes, bribes to police, inspectors, and government officials allow operations to continue unchecked. This web of corruption creates a shadow system of governance where criminal networks, not the state, control the profits from the Amazon’s wealth, making efforts to stop the destruction incomplete from the start.

The Illicit Global Supply Chain: From Amazon Mud to Global Market

The illegal gold from the Amazon enters the legitimate global market through sophisticated laundering techniques:

Sold to licensed local buyers: Miners first sell gold to local traders or buyers who hold licenses, giving the gold a basic paper trail and making it easier to re‑sell without immediate suspicion (Igarapé Institute; GIJN).

Mixing and smelting:Traders mix illegally mined gold with legally sourced gold or smelt it together. Once mixed and refined, the metal is chemically indistinguishable, so the illicit origin is erased. As the UNODC observes, traders “obscure the origin of gold or mix legal and illegal batches” to launder shipments into the formal chain.

False or forged paperwork covers tracks: The mixed metal is then accompanied by falsified documents claiming it came from a legal mine or concession. Paperwork may invent a supplier, overstate a legal mine’s output, or use shell companies to create a believable paper trail.

Export to international refineries: With seemingly clean documentation, gold is exported to major refineries and trading hubs. Once refined, the metal enters the legal market popularly known as “gold heating” as “clean” gold, ending up in jewelry, electronics, and financial reserves with no clear link back to the Amazon.

Money‑laundering and concealment of proceeds:The cash proceeds are also laundered through complex financial routes, further separating profits from their criminal and environmental origins. This helps sustain criminal networks and shields those who benefit.

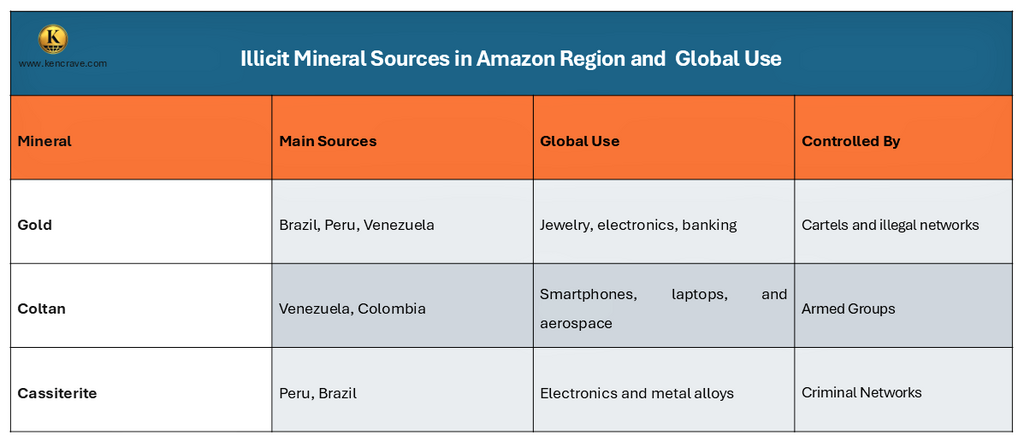

It’s Not Just Gold: The Expanding Illicit Mineral Trade

While gold dominates headlines, other illicit minerals, coltan and cassiterite, essential to the smartphones, laptops, and jets of our modern world, are also extracted illegally, creating profound Environmental, Social, and Governance (ESG) challenges that global industries can no longer ignore.

This illicit economy, controlled by armed groups, cartels, and sophisticated criminal networks, directly connects consumer electronics to environmental devastation, human rights abuses, and the destabilization of entire regions.

Global AI industry rankings by country: USA, China, Singapore, UK, France, Australia - highlighting strengths in R&D, fintech, smart cities, and AI governance.

Environmental and Economic Damage in South America

The illegal extraction of these minerals is not a victimless crime; it has created a dual crisis that destroys ecosystems while draining national economies across South America.

Environmental Damage

Mercury Pollution-Illegal mining is now one of the world’s largest sources of mercury, contaminating rivers and harming wildlife and Indigenous communities.

Deforestation: Gold mining has cleared 139,169 hectares of the Peruvian Amazon by mid-2025, worsening climate change (MAAP).

Biodiversity Loss: Between 2,400 and 4,550 species (600–1,138 species of trees) are at risk of extinction due to mining.

Economic Consequences

Massive Tax Losses: Reported gold production in the Amazon Basin leads to major revenue losses for national treasuries.

Agricultural Impact:The World Bank warns that ongoing deforestation in the Brazilian Amazon could lead to economic losses of up to $317 billion annually due to disrupted rainfall and exhausted natural resources.

Public Health Costs: Mercury exposure causes lifelong neurological damage, creating a silent public health crisis and straining underfunded healthcare systems.

Investor Flight: Poor ESG scores tied to the region’s mining crisis raise borrowing costs and scare off foreign investment, limiting sustainable growth.

Social & Human Impact: The Hidden Cost of Gold

Behind the shine of Amazon gold lies a harsh reality of the miners' working conditions, including;

Physical Harm and Death: Workers face constant risks from tunnel collapses, drowning, and accidents with heavy machinery. Mercury exposure leads to chronic, debilitating health issues.

Psychological Impact: The high-stress, lawless environment fosters substance abuse, violence, and mental health crises.

Human Trafficking and Slave Labor: Many are made to believe in false promises of good wages, only to be trapped in remote locations under the control of armed guards.

Poor Conditions and Wages: Despite the high value of the gold they extract, most garimpeiros earn low wages. They work long hours with no labor rights or social protections.

Global Comparison: The Amazon’s ESG Crisis in Context

The Amazon’s crisis is not an isolated tragedy but part of a devastating global pattern where consumer demand fuels conflict and corruption.

Chart of illicit Amazon minerals: gold, coltan, cassiterite - showing sources, global tech use, and control by criminal networks.

This global comparison underscores a critical truth: the crisis is sustained by international markets. Consumer demand for cheaper electronics, faster gadgets, and precious materials creates a powerful economic incentive that feeds these destructive cycles across three continents.

Breaking the Cycle: Pathways Toward Sustainable Mining can be tackled from both supply and demand perspectives. By working together, governments, companies, and local communities can dismantle criminal networks, safeguard the Amazon, and boost the region’s economy.

For Governments & Policy Makers:

Formalize Mining: Make it easier for small-scale miners to register legally and follow basic safety and environmental rules. This helps pull workers away from illegal operations.

Stronger Cross-Border Enforcement: Fund permanent joint task forces (like the Colombian-Brazilian example) to target the leaders and finances of mining cartels, not just their equipment.

Invest in Alternatives: Support sustainable jobs in mining regions, such as farming, eco-tourism, and renewable energy projects, so people have real choices besides mining.

Track Gold Digitally: Use secure systems (like blockchain) to trace gold from mine to export, making fraud much harder.

For Corporations & Industry:

Check Supply Chains: Go beyond paperwork. Send independent teams to check suppliers and refineries to confirm where minerals really come from.

Buy Ethical Gold: Purchase gold from verified responsible miners, creating demand and fair prices for legal, safe production.

Support Communities: Work with local governments and NGOs to fund schools, healthcare, and alternative jobs in areas affected by mining.

For International Bodies & Consumers:

Enforce Global Rules: Make sure laws like the EU Conflict Minerals Regulation are strong and strictly applied, with penalties for violations.

Choose Ethical Products: Consumers should buy from brands certified by groups like Fairmined or the Responsible Jewelry Council.

Support Indigenous Guardianship: Help Indigenous groups secure land rights and fund programs that protect forests.

The illegal mining boom is more than just an environmental problem; it is the latest chapter in a centuries-long struggle between harmful extraction and the health of people and the planet. The connection from the colonial mines of Minas Gerais to today’s mercury-contaminated rivers is clear and unbroken. While the solutions already exist, the cycle can be stopped by the commitment of relevant stakeholders.

Tackling this crisis is South America’s biggest chance to secure its economic future by formalizing the economy, increasing tax revenue, creating safer jobs, and attracting investors.

The choice is no longer development or conservation. The key drive is to attain sustainable management. The future of the Amazon, the stability of South America, and the safety of the products we use every day depend on the decisions made today.

Key Takeaways.

1. The Amazon gold rush continues a 500-year history of exploitation, from colonial times to today’s criminal mining networks.

2. Illegal mining causes both environmental devastation and billions in economic losses across South America.

3. While gold is central, many other minerals fuel global supply‑chain risks.

4. Combating the crisis requires both stronger law enforcement and ethical consumer behavior worldwide.

5. Sustainable, transparent mining practices can protect the Amazon, strengthen regional economies, and improve global ESG performance.

FAQs on Illegal Mining in the Amazon

1. Why is illegal mining harmful to the Amazon rainforest?

It causes severe deforestation, mercury pollution, displacement of Indigenous communities, and strengthens criminal networks that destabilize the region.

2. How does illegal Amazon gold get laundered into the global supply chain?

It is sold to licensed buyers, mixed with legal gold, paired with falsified documents, and exported to refineries where its illegal origins become untraceable.

3. What forces people to work as illegal miners (garimpeiros)?

Extreme poverty, lack of formal employment, and limited economic opportunities push many toward dangerous, unregulated mining for survival.

4. Do legal mining companies contribute to illegal mining activity?

Indirectly by creating roads and infrastructure that open remote forests, normalizing extractive economies, and allowing illegal gold to blend with legal production.

5. What are the most effective solutions to reduce illegal mining in the Amazon?

Formalizing small-scale mining, strengthening cross-border enforcement, providing alternative livelihoods, improving gold traceability, and encouraging ethical corporate and consumer choices.

Venezuela is reasserting itself as a geopolitical disruptor in the Western Hemisphere, leveraging vast oil reserves, ideological alliances, and defiance of Western sanctions to challenge U.S. influence. Its actions reverberate across global energy markets, diplomatic corridors, and ESG governance debates, positioning Caracas as both a regional agitator and a case study in resource-based resilience.

Historical Roots of Economic Instability

Venezuela’s economic crisis is deeply rooted in the Chávez era of resource nationalism and institutional erosion.

Populist oil dependence: Hugo Chávez (1999–2013) used oil revenues to fund massive social programs, creating fiscal dependence on volatile oil prices (Council on Foreign Relations).

Industrial decline: Nationalization and price controls led to “Dutch disease,” where oil crowded out other productive sectors.

Hyperinflation and collapse: By 2019, hyperinflation exceeded 10 million percent due to monetary expansion and currency devaluation (FasterCapital).

Sanctions and humanitarian fallout: Global oil price shocks and U.S. sanctions deepened the collapse, prompting mass migration and humanitarian crises (IJCRT).

Resource Nationalism and Energy Diplomacy

Venezuela, home to the world’s largest proven oil reserves, continues to use energy diplomacy to defy isolation and re-enter global markets.

China and Brazil investments: Billions poured into oil infrastructure and joint ventures, bypassing Western sanctions.

Iranian cooperation: Fuel supplies and technical aid have deepened logistical and ideological ties.

Alternative trade systems: PDVSA has resumed limited exports to India and Turkey via barter and crypto-based deals.

This “energy defiance” undermines Western control over oil markets and opens new pathways for South-South energy cooperation.

Militarization and Regional Tensions

In August 2025, the U.S. deployed 4,000 Marines and eight naval vessels near Venezuelan waters under an anti-narcotics pretext. Caracas retaliated with military drills and outreach to allies including China, Brazil, and Iran.

$700M Venezuelan assets frozen by the U.S. Treasury (DW).

Sovereignty dispute: Maduro denounced U.S. maneuvers as violations of sovereignty, inflaming regional sentiment.

Regional response: Colombia and Argentina monitor closely, wary of spillover and destabilization.

Strategic Alliances and Global Influence

Venezuela’s non-Western alliances strengthen its defiance and amplify its global footprint.

China: Provides surveillance tech, loans, and diplomatic cover.

Brazil: Offers energy cooperation, ESG expertise, and pragmatic regional support.

Iran: Supplies fuel and ideological solidarity.

These partnerships form a multipolar bloc challenging U.S. hegemony and reshaping Global South diplomacy.

A chart of comparative ESG Scores in Latin America and Global Powers (2025). Sources: ISESG Global ESG Ranking, KPMG Chile ESG Transparency Report, Anuário Integridade ESG – Brazil, Pacto Global Colombia, SDG Index – Argentina, SDG Index – United States, IBISWorld Germany ESG Rankings, India360 ESG Risk Ratings, NenPower ESG Impact – China, IRAS ESG Assurance – South Africa

Venezuela’s ESG score of 42 is the lowest among peers, underscoring deep sustainability and governance risks.

Regional Relationships and Diplomatic Outlook

Venezuela’s regional diplomacy balances defiance with pragmatism.

Brazil: Offers energy cooperation yet remains wary of destabilization.

Uruguay: A governance benchmark with strong institutions and transparency.

Mexico: Maintains neutrality and often mediates in regional forums.

Chile & Colombia: Prioritize rule-based diplomacy and ESG compliance.

Venezuela’s aggressive posture could alienate democratic neighbors, but shared interests in resource sovereignty may enable selective collaboration.

Key Insights (2025)

Venezuela’s ESG score (38) remains the lowest in the region, reflecting governance and environmental decline.

China, Brazil, and Iran are its primary strategic partners, helping bypass sanctions.

South American resource nationalism may spread, with Bolivia and Suriname exploring similar assertive models.

Global energy markets are shifting as Venezuela re-enters via barter and crypto trade.

U.S. military deployments and Venezuelan mobilization heighten escalation risks.

The Stakes Ahead: What Lies Beyond 2025

Venezuela’s trajectory will shape global debates over sovereignty, energy security, and ethical governance. Key considerations for policymakers and investors include:

Balancing deterrence and diplomacy: Avoid escalation while addressing ideological divides.

Promoting ESG reform: Transparency and sustainability can stabilize Latin American supply chains.

Monitoring resource-backed alliances: Oil and minerals may become leverage in global voting blocs.

Studying Uruguay’s model: Robust governance and fiscal discipline provide a regional blueprint for credibility

On the night of October 28, 2025, Israel initiated a new wave of air and ground attacks across Gaza, citing a breach of the Trump-brokered ceasefire signed earlier that month. According to Israeli authorities, Hamas facilitated attacks in southern Gaza that left one Israeli soldier dead and allegedly returned an empty coffin instead of the remains of a deceased hostage, a violation of the agreement’s key terms.

Gaza’s Civil Defense Agency reported heavy civilian casualties, including women and children, reigniting international condemnation and humanitarian concern.

The Trump-Brokered Ceasefire Agreement Between Israel and Hamas

The ceasefire, brokered by former U.S. President Donald Trump and entered into force on October 10, 2025, was hailed as a landmark truce aimed at ending a two-year-long rift. Its main provisions included:

Mutual release of hostages,

Suspension of Israeli military operations in Gaza,

Humanitarian aid access and monitoring,

Gradual withdrawal of Israeli forces from occupied zones.

Despite its ambitious framework, critics warned of its structural fragility and lack of inclusivity in the negotiation process.

What Triggered the Renewed Violence? Inside the Alleged Breach of Truce

The latest escalation followed Israeli claims that Hamas had violated ceasefire terms through an orchestrated attack and deceptive prisoner-exchange gesture. Hamas, in contrast, denied the allegations and accused Israel of provoking renewed violence to justify continued occupation. The finger-pointing has undermined trust in the fragile peace and reignited fears of a full-scale conflict in Gaza.

Humanitarian Crisis Deepens: Civilian Toll Mounts in Gaza

Gaza’s Civil Defense Agency confirmed that Israeli strikes hit residential buildings and the Bureij refugee camp in central Gaza. Early estimates suggest dozens killed, many of them women and children, while hundreds more were injured or displaced. International humanitarian organizations have warned that access to food, water, and medicine remains critically limited amid the ongoing bombardment.

Stakeholder Reactions: Global Powers Respond to Israel–Hamas Ceasefire Collapse

Israel: “A Duty to Defend”

Prime Minister Benjamin Netanyahu defended the military response, saying Israel was “ethically and morally bound” to protect its citizens. IDF Chief Lt. Gen. Herzi Halevi reiterated that the army “shall not relent” in defending Israeli sovereignty (Times of Israel).

Hamas: “Israel Violated the Deal First”

Hamas accused Israel of breaking the truce, warning that further escalation would halt hostage releases and deepen the humanitarian catastrophe.

United States: Cautious Endorsement of Israel’s Response

U.S. Vice President JD Vance stated that “small skirmishes” were inevitable but insisted that the Trump peace deal remains the only viable path to lasting peace. Washington emphasized Israel’s right to respond while urging both sides to avoid all-out war.

United Nations: Alarm Over Renewed Violence

U.N. Spokesperson Stéphane Dujarric expressed “grave concern” that renewed attacks could stall peace progress and deepen Gaza’s humanitarian disaster.

Ceasefire Prospects: Why the Trump Peace Deal Is Facing Collapse

Over 2 million people facing extreme hunger and malnutrition.

Analysts say the ceasefire’s rigid 20-point plan lacked flexibility for political realities. While hostage exchanges and limited aid deliveries occurred, trust deficits and unresolved issues made the deal inherently unstable.

Unresolved Issues Threatening Peace

Experts highlight three core disputes that could doom the agreement:

Incomplete return of deceased hostages.

Hamas disarmament and reintegration.

Israeli withdrawal from key Gaza regions.

Until these are addressed with mutual verification, peace remains more illusion than promise.

Promise or Illusion: Is Trump’s Gaza Peace Deal Built to Last? The Trump ceasefire was celebrated as a turning point, but is now seen as politically one-sided. Analysts at the Arab Center Washington DC note that the deal was framed as an ultimatum to Hamas rather than a mutual negotiation, undermining long-term legitimacy. While limited successes, such as partial hostage release, have occurred, disarmament and troop withdrawal remain largely unimplemented.

The Future of Peace in the Middle East: Lessons from a Fragile Ceasefire

The conflict’s persistence suggests that neither Hamas nor Israel alone determines the outcome. Peace depends on sincere implementation, regional cooperation, and balanced diplomacy. The Trump Administration continues to claim that the “core foundations of the deal remain solid”, but skepticism prevails among observers.

Roadmap for Action: Pathways Toward a Lasting Resolution

Engage Key Regional Actors: Include Egypt, Iran, and Gulf States as economic and diplomatic partners in peace enforcement.

View Ceasefires as Beginnings, Not Endpoints: Treat truces as frameworks for deeper negotiations, not as conclusive settlements.

Promote Palestinian Political Inclusion: Encourage unity between Hamas and the Palestinian Authority to prevent remilitarization and internal division.

Broaden the Peace Architecture: Frame negotiations as part of a regional peace system, not just an isolated bilateral deal.

Pursue a Two-State Solution with Renewed Vision: Sustainable peace demands equal sovereignty, security, and recognition for both Israelis and Palestinians.

Genuine Commitment as the Key to Lasting Peace

The October 2025 escalation demonstrates how quickly optimism can evaporate in the Middle East. Unless both parties and the global mediators commit to transparent, enforceable mechanisms, any ceasefire will remain a temporary pause rather than a path to resolution. The world now watches to see whether the Trump-brokered deal becomes a blueprint for durable peace or another missed opportunity in Gaza’s long history of conflict.

While global tech giants pour hundreds of billions into AI, Australia is taking a strategic different path. With a modest regulatory budget of just $39.9 million, the nation is prioritizing sovereignty over scale, refusing to let its creative output become mere training data for foreign algorithms.

This strategic stance was made on October 27, 2025, when Attorney-General Michelle Rowland announced that the government would not weaken copyright laws for AI companies, a strategy aimed at safeguarding Australia’s $116 billion economic potential and preserving its distinctive cultural identity.

How Australia Compares in Global AI Adoption and Innovation Leadership

Australia's adoption of AI reveals significant challenges when compared to global leaders. While 37% of Australian SMEs have embraced AI (Australian AI Ecosystem, 2024), this adoption rate trails behind major economies that have integrated AI deeply across multiple sectors.

The Global AI index published on 19 September 2024 shows that Australia needs stronger national coordination and investment to remain competitive internationally.

Global AI industry rankings and strengths by country - USA, China, Singapore, UK, France, Australia, highlighting leadership in AI talent, R&D, fintech, smart manufacturing, and government strategies.

The Four Pillars of Australia’s National AI Sovereignty Framework

Australia’s strategy is to make AI inclusive and responsible, while achieving a delicate balance between two national priorities: protecting creativity and building innovation.

The country is aligning its policymakers, industry leaders, and researchers under a unified vision of AI sovereignty, designed to strengthen coordination, attract investment, and advance a cohesive national AI agenda. This strategic framework is anchored on four key pillars;

Sovereign Infrastructure: Building secure, onshore data centers to support trusted AI development.

Australian Models & Data: Creating local AI models using datasets that reflect diverse values and contexts.

A World-Class Workforce: Fostering essential domestic expertise for future AI systems.

Responsible Governance: Implementing strong oversight for ethical and safe AI use in our national interest.

AI Regulation in 2025: Australia’s Turning Point for Digital Policy

Globally, AI is expected to contribute $15.7 trillion to the global economy through 2030, with $6.6 trillion driven by increased productivity and $9.1 trillion driven by AI products and services.

In contrast, the Australian federal government has earmarked just $39.9 million for AI regulation, lower than the billions that other countries are investing in. This creates a tension between participating in global AI innovation and preserving Australia’s creative sovereignty.

To navigate this challenge, the government has set an urgent deadline to unveil its National AI Plan by the end of 2025.

Australia’s AI Economic Potential: Key Growth Sectors and Opportunities

AI's transition from emerging technology to economic driver positions it to contribute over $116 billion to Australia's GDP (Productivity Commission report, 2025). The ecosystem shows potential growth with 1,533 AI companies, including 110 startups, and significant productivity gains across key sectors.

Mining operations optimize through predictive maintenance, healthcare-enhancing diagnostics, and agriculture advancing toward sustainable practices.

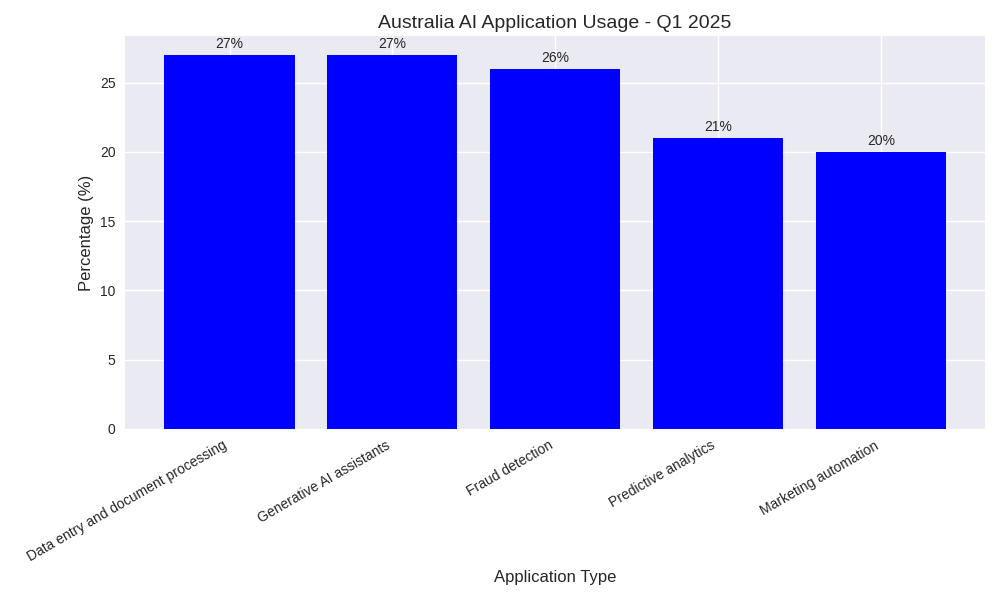

The Australian Government Q1 report, 2025, shows that the adoption of AI has seen a growing trend, particularly in the retail, health, and education sectors. In Q1, 2025, the businesses used AI for different purposes.

A chart indicating adoption of AI in percentages in different areas in Australia.

The Structural Weaknesses Slowing Australia’s AI Competitiveness

Despite promising growth, Australia faces substantial structural challenges that specialists caution may hinder its effectiveness. Australia's AI Ecosystem Report 2024 shows that a substantial research-to-commercialization gap persists, with 93,302 AI research papers resulting in only 4,075 patents between 2015 and 2024.

The ecosystem remains constrained by several structural and capacity limitations.

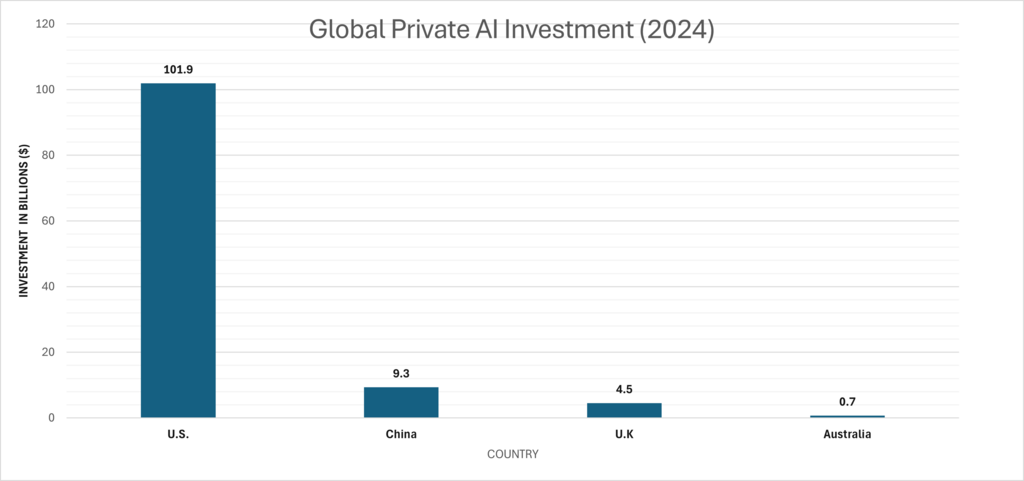

Investment Deficit: Australia's $0.7 billion private AI investment falling significantly behind the US ($109.1Billion), AUD $166.4 billion (Australian AI Report, 2024).

Small firms dominate the sector, with 85% of AI companies having fewer than 50 employees, hindering scaling.

Talent concentration where 58% of AI job listings come from just 100 companies in major cities, creating regional imbalances.

Australia's AI infrastructure gap, with only three foundation models (Phoenix, SAIGE, and Harrison, rad.1)

A graph indicating Global Private AI investment by U.S., China, U.K and Australia. Source: Australia AI Ecosystem, 2024 Report.

Key Insights and Highlights: Where Australia Stands in 2024–2025

The United States leads AI investment significantly, attracting $109.1 billion, showing its strong position in AI innovation, fueled by robust venture capital and major tech companies.

China maintains a steady $9.3 billion but tightly regulated AI investment strategy, focusing on semiconductors, generative AI, and industrial automation.

The United Kingdom follows with investments of $ 4.5 billion, benefiting from national AI strategies that balance innovation and governance, establishing them as regional hubs.

Australia's $ 0.7 billion investment points to a critical weakness, as it trails behind comparable economies. Despite a strong research foundation, gaps in research commercialization and funding hinder the development of market-ready AI technologies.

Policy Implications and Strategic Recommendations for Australia to Strengthen National AI Capability

To protect Australia's innovation sovereignty and address structural gaps, a unified national AI policy is essential. This policy should unite government, academia, and industry to develop a robust AI ecosystem. This is through;

Boosting AI Investment by creating national investment funds, tax incentives, and public-private partnerships to attract domestic and foreign capital while supporting startups.

Accelerating Research by linking universities with industry to turn academic research into market-ready AI products.

Developing AI Hubs by establishing innovation zones and research centers beyond major cities to foster inclusive growth and broaden access to talent.

Investing in AI Models by focusing on funding and developing local foundation models that secure domestic data infrastructure to maintain digital sovereignty. Strengthening Talent Pipelines by enhancing AI education and training programs to cultivate a sustainable local talent pool and decrease dependence on foreign expertise.

The Five-Year Transformation Window: How Australia Can Lead in AI by 2030

The global examples of Canada, Singapore, and the UK demonstrate that mid-sized economies can achieve AI leadership through targeted investment and a cohesive strategy. Australia has the fundamental ingredients for success in world-class research, robust industries, and rich data.

The next five years present a transformative opportunity. Australia's path to AI leadership is about leveraging unique strengths, in research and values, to strategically outthink the current challenges and collaboratively build a better tomorrow.

Key Takeaways for Australia’s Path to AI Leadership and Innovation Sovereignty

The next five years are crucial for Australia to assert itself in the global AI arena, urging immediate action.

The strategic leadership Approach is about leveraging Australia’s unique strengths and values, not engaging in an expensive arms race.

Australia to apply strategic intelligence to navigate complex challenges and mobilize national collaboration to develop tangible AI capacity.

To unite stakeholders and build the strategic momentum essential for transforming this vision into reality.

Argentina’s 2025 midterm elections, held on 26 October 2025, renewed half of the Chamber of Deputies (127 of 257 seats) and one-third of the Senate (24 of 72 seats). As with every midterm cycle, these elections act as a nationwide referendum on the performance of the sitting government.

With the economy undergoing historic restructuring under Javier Milei, these midterms were especially pivotal. They determined whether the public still supported his reform agenda, one based on drastic fiscal tightening, deregulation, subsidy cuts, and aggressive market liberalization.

The result would define not only governability for the rest of Milei’s term but also the political landscape leading into the 2027 presidential race.

Javier Milei’s Economic Reforms: Achievements, Inflation Decline, and Market Impact

Since taking office in late 2023, libertarian President Javier Milei has implemented some of the most aggressive free-market reforms in modern Argentine history. His achievements, though controversial, have reshaped the macroeconomic environment.

Subsidy Cuts and Fiscal Tightening

Milei eliminated or sharply reduced subsidies on energy, transportation, and food. These measures were intended to reduce the fiscal deficit and dismantle decades of state intervention. While successful in lowering government spending, they also intensified short-term social pressure.

Exchange Rate Alignment

The often-chaotic dual-exchange-rate system was streamlined, narrowing the gap between the official and parallel markets. This created more transparency in currency pricing and reduced arbitrage opportunities.

Inflation Reduction

Argentina’s inflation peaked at230% in late 2023,a hyperinflationary environment. Under Milei: 00

Monthly inflation fell from nearly25% to under 5% by late 2024.

Annual inflation dropped from 230% to 117.8% by December 2024.

In May 2025, inflation hit 1.5%, the lowest since 2020.

A graph showing Argentina's General Inflation rate from January 2018 - December 2024. Source: National Institute of Statistics and Census of Argentina (INDEC)( PIIE).

This reduction marks one of the fastest disinflation periods in Argentine history.

Foreign Reserves and IMF Support

Gross foreign reserves increased from $23 billion in 2023 to nearly $30 billion in 2024, helped by IMF backing and new credit lines. However, net reserves remain negative, improving only from -$11 billion in late 2023 to roughly -$6.6 billion in early 2025. This gap highlights Argentina’s ongoing inability to fully defend its currency or meet external obligations without external dependence.

Social Costs and Regional Tensions

Despite macroeconomic improvements, real wages have stagnated, poverty has increased, and social unrest has grown. Regionally, Milei’s ideologies clash with Brazil and Chile having strained diplomatic relationships with the two countries.

Midterm Results and Political Shifts: LLA’s Rise and Peronism’s Weakening Strongholds

The 2025 midterms produced a transformative political realignment.

Vote Distribution

La Libertad Avanza (LLA): est. 40.8%

Peronist coalition: est. 31.7%

LLA secured victories in 16 of 24 provinces, including Buenos Aires, historically the heart of Peronist power.

Congressional Gains

Chamber of Deputies:

LLA grew from 37 seats to 80.

With allies, the governing coalition now controls 111 seats.

The opposition totals 99 seats.

Senate: LLA won 13 of the 24 seats in play, strengthening its influence in the upper house.

Political Realignment

This election marks one of the most significant setbacks for Peronism in decades. New coalitions are emerging, and radical factions within traditional parties are vying for influence. Milei’s legislative power is substantially strengthened, enhancing his ability to pass reforms and setting the stage for a formidable 2027 reelection bid.

U.S. and Donald Trump’s Role in Argentina’s 2025 Elections: Support, Controversy, and Geopolitics

Former U.S. President Donald Trump played a visible and controversial role in Argentina’s electoral process.

Public Endorsement - In early October 2025, Trump released a video calling Milei:

“A great leader and a great friend who’s saving his country from socialism.”

U.S. Conditional Support

Weeks before the election, the U.S. offered:

A $20 billion currency-swap and loan package.

Treasury support for debt restructuring. Both offers were implicitly tied to Milei’s electoral performance, a rare example of open geopolitical leverage.

Regional Reactions

Brazil, Mexico, and Colombia condemned U.S. interference, arguing it compromised Argentine sovereignty.

Investors, however, viewed U.S. backing as geopolitical “insurance,” leading to immediate strengthening of bonds and the peso after the election.

China, having previously supported Argentina, sees the U.S.-Milei alliance as part of a broader struggle for influence in Latin America.

This election may become a blueprint for how Washington supports pro-market governments in the region.

Implications of Milei’s Victory for Argentina’s Future: Governance, Markets, and Regional Dynamics

Milei’s midterm success reshapes Argentina’s trajectory across political, economic, and geopolitical domains.

Governability and Reform Pace

With a more favorable Congress, Milei can accelerate deregulation, state-shrinkage measures, and wider market reforms. Opposition parties now face greater difficulty blocking legislation.

Market Confidence

Markets responded immediately:

Argentine bonds rose.

The peso stabilized.

Investor optimism increased.

Regional Attention

Latin American governments are watching closely. Milei represents a bold policy experiment in:

extreme fiscal tightening.

rapid deregulation.

reliance on external capital.

Whether this model becomes a new regional trend or collapses under social strain, remains to be seen.

Foreign Dependence and Risk

U.S.-linked support packages create new forms of dependency. Success may attract global investment; failure may intensify unrest, raise debt pressure, and deepen Argentina’s political divides.

Recommendations for Argentina: Policy Priorities, Investment Opportunities, and Economic Stabilization

Argentina now confronts the challenge of translating political capital into sustainable long-term development.

Policy Priorities

Maintain fiscal discipline while avoiding excessive austerity.

Strengthen productive investment rather than solely cutting expenditures.

Manage IMF commitments carefully to avoid social destabilization.

Social Stability Measures

While maintaining reforms, the government must ensure:

support for vulnerable sectors.

stabilization of real wages.

controlled rollout of deregulation to prevent shocks.

Investment Outlook

Investors should diversify within South America and focus on strategic sectors such as:

Lithium (Argentina holds some of the world’s best reserves).

soy and agriculture.

energy and critical minerals.

Argentina could become Latin America’s next commodity and energy hub, especially if aligned with U.S. markets, potentially reducing Chinese economic dominance.

Argentina at a Crossroads After Milei’s Strengthened Mandate

Argentina stands at a defining moment. Milei’s midterm victory consolidates his power, giving him unprecedented ability to reshape the country’s political and economic structure. Success could position Argentina as a leading free-market economy in the region, attracting investment and stabilizing long-term growth. Failure could deepen poverty, increase unrest, and intensify geopolitical tensions.

The coming years will determine whether Milei’s experiment becomes a historic transformation or a cautionary tale for Latin America.

A leading global company for Business Solutions , bringing the intriguing global business arena into your space to a business and financial savvy mind.

social media:

Stay In Touch

Don't hesitate. Reach us with these info.

0795046415financialshub01@gmail.comNairobi/Kenya

We create great content everyday. Subscribe to be the first notified when released.

.png)

.png)

.png)