Greenland’s Strategic Geography in Arctic and Transatlantic Security

With its geographical location between North America and the Arctic, Greenland is one of the largest islands in the world. In recent years, there has been an increase in interest in Greenland's natural resources, including a wide variety of rare earth minerals, uranium, and iron. It is also expected that there are significant amounts of oil and natural gas reserves in Greenland.

2026 Arctic military base map showing strategic installations by Russia, US, Canada, Denmark, Norway, and UK across the polar region, highlighting Pituffik Space Base, NORAD, and Joint Arctic Command. Source: Aljazeera.

Rare Earth Minerals, Energy Reserves, and the Global Resource Race in Greenland

Greenland is not a colony to be sold but an autonomous territory. It is supported by Denmark's constitutional partnership and subsidy, and its security is guaranteed by NATO and specifically managed through the existing U.S.-Denmark defense agreement, which already secures America's key military interests on the island.

During the Cold War, the US planned to develop nuclear weapons for use in Greenland but ultimately scrapped those plans due to:

Technical issues.

Engineering difficulties.

Objections by Denmark.

Greenland’s Political Status: Autonomy, Danish Sovereignty, and International Law

Greenland has continued to enjoy full recognition as an integral part of the Kingdom of Denmark. The leaders of Europe (UK, France, and Denmark) are against the U.S earlier threats to impose tariffs against European nations concerning Greenland. Greenland remains a part of NATO under Article 5 of the North Atlantic Treaty. NATO Article 5 and Greenland’s Role in Collective Arctic Defense

On Wednesday 21st January 2026, while speaking at the World Economic Forum in Davos, Trump stated that the United States would not use excessive force in its quest to acquire Greenland. On 24th January 2026, Trump revealed the imposition of tariffs on eight NATO-allied European nations due to their participation in military exercises at a location located off the coast of Turkey. The announcement of the tariff by Trump led to immediate threats of trade retaliation from those European Union Member States, each of which was already subject to tariffs of 10% and 15% respectively.

The EU–U.S. Trade Relationship at Risk: Energy Imports, Investment, and Retaliation

In response to this escalation, a number of European Union Officials held an urgent emergency meeting to review the possibility of coordinating a response to the U.S. imposition of tariffs. In addition, there are considerations of abandoning the U.S.-E.U. Trade Agreement reached in the summer of 2017.

The Agreement comprises:

$750 Billion in U.S. energy imports.

$600 Billion in E.U. investment.

Billions of U.S. dollars in tariff reductions for imports into the European Union.

Arctic Militarization After Venezuela: U.S. Power Projection and Global Signaling

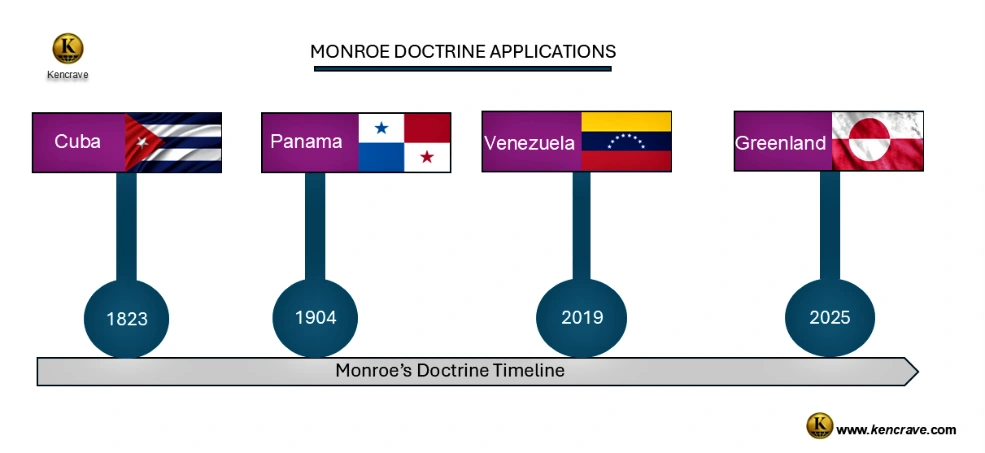

After the US Military Raid against Venezuela on January 6, 2026, Venezuela's President, Nicolas Maduro, and his wife were captured and brought to New York to face criminal prosecution. During this period, President Donald Trump began the aggressively push for US ownership of Greenland, a large island in the North Atlantic pointing to the adoption of Monroe Doctrine previously used in Cuba and Panama.

Missile Defense in the Arctic: The “Golden Dome” Proposal and Strategic Implications

Following a meeting with NATO Secretary General Mark Rutte in the Swiss Alps, President Trump proposed that an agreement could be reached among the Arctic nations that would allow for the establishment of a US Missile Defense Site or "Golden Dome" in Greenland while simultaneously accommodating the desires of his NATO partners to control access to Greenland.

Countering Russia and China in the Arctic: Strategic Competition and Resource Control

Additionally, Trump wants a strategic military and economic partnership with Arctic nations that would include shared access to valuable mineral resources and would prevent Russian or Chinese domination of the Arctic region. European Unity and Strategic Autonomy in Response to U.S. Pressure

Emmanuel Macron of France, noted the need for Europe to remain extremely vigilant and be ready to use the instruments at their disposal if threatened by the U.S. The putative deal on Wednesday 21st January 2026, could revolve around a renegotiation of that 1951 defence pact, which was updated in 2004 to take account of Greenlandic home rule.

Key Takeaways: Greenland Arctic Security, Rare Earths & The Nato Sovereignty Standoff

Greenland is a strategic Arctic focal point for NATO, NORAD, and transatlantic security, controlling key air, missile-warning, and polar routes.

Critical minerals and energy reserves position Greenland at the center of the global race for rare earths, oil, gas, and uranium.

Greenland’s sovereignty is settled under Danish and international law, with NATO Article 5 guaranteeing its security and blocking any forced transfer.

U.S. pressure risks fracturing NATO and EU–U.S. trade ties, threatening major energy, investment, and tariff agreements.

Accelerating Arctic militarization reflects U.S.–Russia–China competition, with missile defense and resource access shaping the next geopolitical frontier.

Frequently Asked Questions

1. Why is Greenland strategically important in Arctic geopolitics? Greenland’s location between North America and the Arctic, combined with its military relevance and access to critical resources, makes it a key asset in global security and great-power competition.

2. Does the United States have the legal right to acquire Greenland? No. Greenland is an autonomous territory within the Kingdom of Denmark, and its sovereignty is protected under Danish law, international law, and NATO agreements.

3. How does NATO Article 5 apply to Greenland? As part of the Kingdom of Denmark, Greenland falls under NATO Article 5, meaning any armed attack on it would trigger collective defense obligations.

4. What role do rare earth minerals play in Greenland’s geopolitical significance? Greenland holds valuable rare earth minerals, uranium, and potential energy reserves, which are critical for defense technologies and supply chain security, increasing international interest in the island.

5. How could U.S.–EU trade tensions affect Arctic security cooperation? Tariffs and trade disputes risk weakening transatlantic unity, potentially complicating coordinated NATO responses and long-term Arctic security strategies.

The renewed US interest in Greenland, particularly under President Donald Trump’s administration, reflects a convergence of geopolitical, economic, and environmental factors. Greenland’s strategic location in the Arctic, its vast mineral reserves, and its role in global climate governance have made it a focal point of US foreign policy.

Historical Attempts to Acquire Greenland

The United States has tried several times to acquire Greenland. In 1867, Secretary of State William Seward explored the idea after purchasing Alaska, but political backlash and Denmark’s disinterest ended the effort. In 1916, the U.S. formally recognized Danish sovereignty over Greenland in exchange for the Danish West Indies, closing the door on acquisition.

After World War II, President Truman offered Denmark $100 million for Greenland, citing its military importance, but Denmark refused. Most recently, in 2019, President Trump floated the idea publicly, calling Greenland vital for U.S. defense and resources.

Denmark and Greenland’s leaders dismissed the proposal as “absurd,” and NATO allies worried about unilateralism. These repeated failures underscore the resilience of Danish sovereignty and Greenlandic autonomy.

Timeline of U.S. Attempts to Acquire Greenland

US attempts to acquire Greenland timeline historical failures and Denmark resistance.

Security Risks and Strategic Importance

Greenland’s position in the Arctic makes it a critical node in global security. At the heart of this is the Thule Air Base, which serves as a cornerstone of U.S. and NATO missile defense and Arctic surveillance. Its location provides Washington with military leverage, enabling dominance in the Arctic and offering early‑warning capabilities against potential threats.

This strategic value is amplified by growing geopolitical rivalries. China and Russia have both expanded their Arctic ambitions, heightening U.S. concerns about maintaining control and influence in the region. As a result, Greenland is not simply a geographic asset but a linchpin in the broader architecture of Arctic defense.

Major Insight:Greenland is indispensable for U.S. Arctic defense. Implication:Sovereignty disputes could alter NATO’s security balance, creating vulnerabilities in alliance cohesion.

Thule Air Base Arctic military zone US Russia strategic map.

Economic Coercion and Resource Competition

Greenland’s mineral wealth and energy potential are central to US strategic calculations.

Rare‑Earths: Greenland’s southern deposits (neodymium, dysprosium, terbium, praseodymium) are vital for smartphones, batteries, wind turbines, and defense systems like jet engines, radar, and precision weapons. They offer the U.S. a potential alternative to China’s dominance in rare‑earth supply chains.

Energy Security: U.S. control of Greenland’s rare‑earths and oil reserves could reduce reliance on China and Middle Eastern imports, strengthen NATO energy security, and stabilize supply chains. However, it would intensify rivalry with China and Russia.

Major Insight:Greenland could reshape global supply chains for rare-earths. Implication: Resource competition risks escalating US-China tensions.

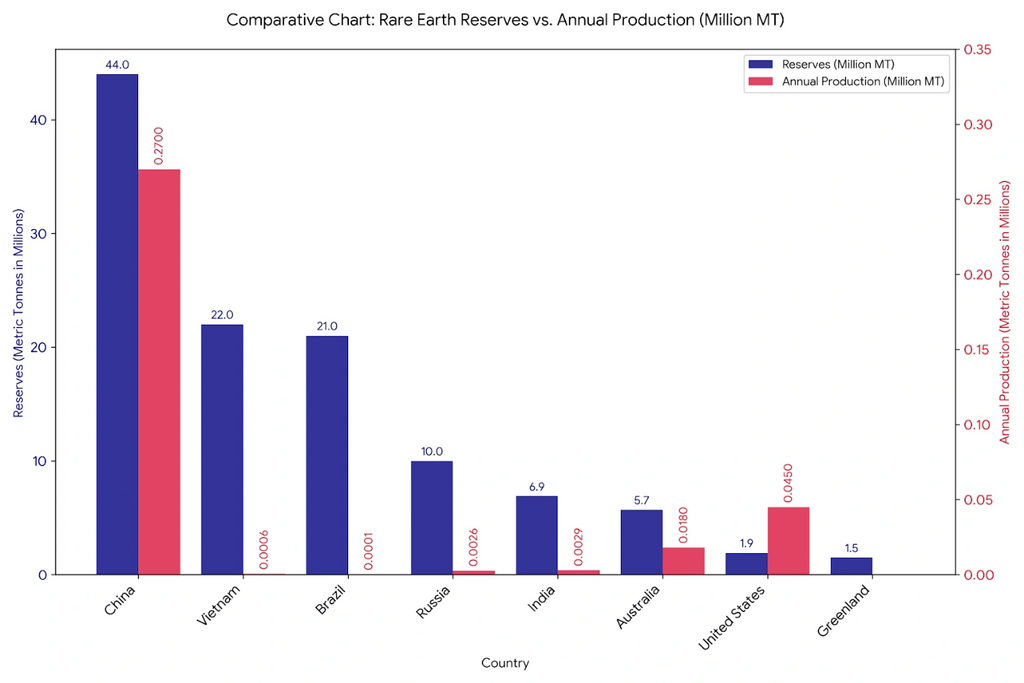

Rare earth reserves vs production China US Greenland global comparison.

Comparative Analysis: Reserves vs. Production

While a country may have high reserves, it does not always equate to high production. The chart below illustrates the stark contrast between what is "in the ground" (Reserves) and what is actually being extracted annually (Production).

China is the only nation with both massive reserves and high production, currently providing over 69% of the world's mine output.

Vietnam and Brazil hold significant reserves but contribute negligible amounts to the global supply, as many of their projects are still in the early development or exploration phases.

The United States has significantly smaller reserves than the top three, yet it is the world's second-largest producer, extracting nearly 45,000 MT annually from the Mountain Pass mine in California.

Geopolitical Coercion and International Relations

The Monroe Doctrine has been invoked to justify U.S. interests in Greenland, reframing Arctic security as part of hemispheric defense. From Washington’s perspective, any foreign involvement in Greenland is seen as a direct threat to national security.

Denmark, however, has resisted these overtures, emphasizing sovereignty and warning that unilateral U.S. moves could strain NATO unity. This tension creates the risk of fractures within both NATO and EU alignment, as allies weigh the balance between collective defense and national autonomy.

Major Insight: Trump’s extension of Monroe Doctrine logic into the Arctic sets a precedent for unilateral U.S. action beyond Latin America. Implication:Such moves could destabilize alliance cohesion and reshape Arctic geopolitics.

Monroe Doctrine timeline history of Cuba, Panama, Venezuela and Greenland.

Environmental and ESG Considerations

Greenland’s environmental role makes it central to global ESG debates. The melting of its vast ice sheets has become one of the most visible drivers of global sea‑level rise, a trend that has accelerated over the past decade and is often illustrated in climate data charts, as shown below.

This environmental shift is not only a scientific concern but also a geopolitical one, as rising seas affect coastal populations worldwide.

Greenland ice sheet mass loss vs global sea level rise 2015–2025 climate graph.

At the same time, indigenous Inuit communities face cultural and livelihood disruptions from resource extraction and militarization. Their rights and traditions are increasingly at the forefront of international discussions about sustainability.

Governance adds another layer of complexity: Greenland’s autonomy within the Kingdom of Denmark complicates questions of sovereignty and long‑term stewardship of its resources.

Major Insight: Greenland stands as a test case for whether powerful nations can balance resource extraction with ESG priorities. Implication:Environmental and social concerns could significantly limit U.S. exploitation of Greenland’s resources, even if strategic interests remain strong.

Greenland ice melt vs global sea level rise bar chart 1993–2023 climate data.

Risk Assessment

Greenland risk assessment table comparing US vs Denmark military economic geopolitical ESG positions.

Global Consequences

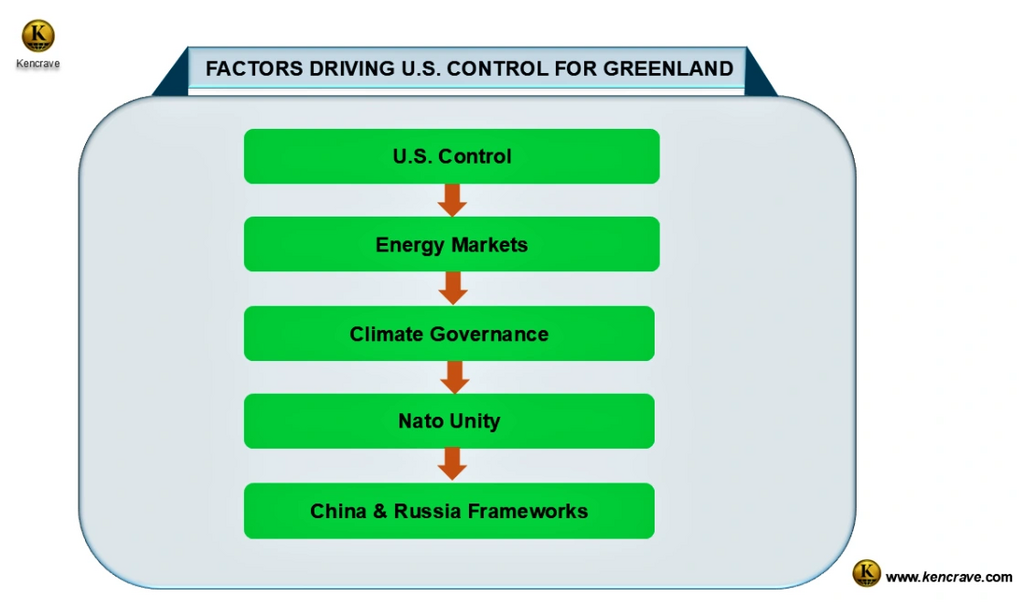

Greenland’s future carries weight far beyond its borders. If the United States were to gain control over Greenland’s rare‑earths and oil reserves, it could fundamentally reshape global supply chains.

Rare‑earth elements from Greenland would provide Washington with a secure alternative to China, which currently dominates global production and processing. This would strengthen U.S. technological independence, ensuring steady supplies for clean energy industries and defense systems such as radar, jet engines, and precision weapons.

Similarly, tapping Greenland’s oil and gas reserves could diversify U.S. energy sources, reducing reliance on Middle Eastern imports and reinforcing NATO’s energy security framework.

Yet, this pursuit of energy security collides with climate governance. Greenland’s role in Arctic climate policy makes U.S. involvement controversial, as resource extraction risks accelerating ice melt and global sea‑level rise.

Sovereigntydisputes with Denmark further complicate matters, raising the possibility of alliance strains if Washington overrides Danish authority. Meanwhile, China and Russia frame U.S. ambitions as neo‑imperialism, intensifying multipolar rivalry in the Arctic.

Major Insight: Greenland is not just territory; it is a pivot for global energy, climate, and security. Implication:Arctic geopolitics could redefine the multipolar world order, reshaping alliances and resource markets alike.

Flowchart of U.S. Control of Greenland, its impact on energy markets, climate, Nato unity, China and Russia frameworks.

Key Takeaways

Military Imbalance: Greenland is central to US Arctic defense.

Resource Race: Rare-earths and oil make Greenland strategically vital.

Monroe Doctrine Revival: Trump reframed hemispheric security to include the Arctic.

ESG Flashpoint: Climate and indigenous rights complicate exploitation.

Global Fallout: Energy markets, NATO unity, and multipolar rivalry all hinge on Greenland’s future.

FAQs

1. Why is Greenland important to the US?

Greenland is crucial for the US due to its strategic military positioning (Thule Air Base), its vast mineral resources, and its potential to influence global energy markets.

2. What is the Monroe Doctrine's relevance to Greenland?

The Monroe Doctrine, historically applied to Latin America, has been extended by Trump to include the Arctic, framing Greenland as a key part of hemispheric security.

3. How could Greenland affect global resource markets?

Greenland’s vast reserves of rare-earth minerals and oil could reshape global supply chains, reducing reliance on foreign resources and increasing competition, particularly with China.

4. What are the environmental concerns regarding Greenland?

Greenland’s melting ice sheets contribute significantly to global sea-level rise, and foreign investments and militarization could disrupt local communities and raise ESG (Environmental, Social, and Governance) concerns.

5. How does Greenland’s sovereignty affect international relations?

Denmark’s resistance to US influence over Greenland creates tensions within NATO and could have broader geopolitical implications, especially with Russia and China’s growing interests in the region.

From M-Pesa to fintech regulation, Kenya’s step-by-step approach to digital finance offers lessons for policymakers, investors, and emerging markets worldwide.

Kenya’s digital finance ecosystem is widely regarded as the most advanced in emerging markets, driven by mobile money, fintech innovation, and adaptive regulation. This analysis explains how Kenya built its digital finance model, why it succeeded, and what risks and opportunities lie ahead.

Kenya did not become a global leader in digital finance through disruption alone. Instead, it followed a deliberate, layered strategy that combined mobile money innovation, adaptive regulation, and widespread mobile access. Today, more than 85% of Kenyan adults use formal financial services, a transformation driven by choices made over two decades.

Mobile money adoption and branchless banking have significantly increased financial inclusion, with access to formal financial services rising from 27 % in 2006 to 85 % in 2024 (Central Bank of Kenya, 2025). Investments in digital infrastructure have further strengthened the reliability and scalability of financial services, establishing Kenya as a benchmark for digital finance in emerging markets (GSMA, 2024).

Kenya’s financial sector has developed through a layered process. Each stage of reform leveraged existing institutional, regulatory, and technological foundations, reinforcing system resilience and enabling incremental innovation. Mobile money platforms and branchless banking models demonstrate how regulatory guidance, infrastructure development, and market demand intersect to expand financial access and foster sustainable digital finance growth.

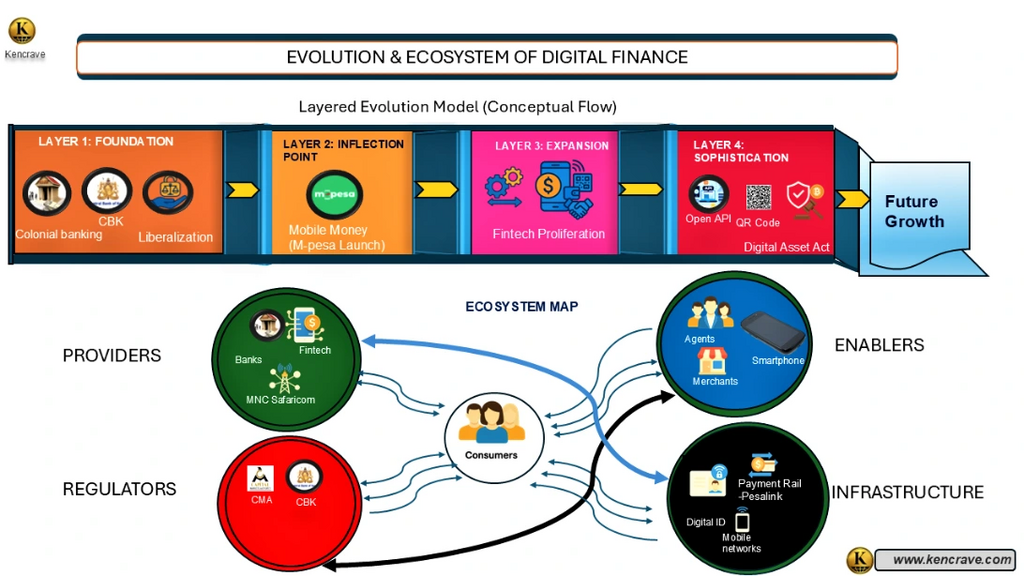

This transformation can be explained using a dual framework that shows both its historical path and its current complexity. Kenya’s digital finance sector has grown in clear stages, with each layer building upon the one before it. This step-by-step growth created today’s interconnected ecosystem, where providers, enablers, regulators, and infrastructure work together around the consumer and MSMEs.

Kenya digital finance evolution ecosystem map showing colonial banking, M-Pesa, fintech, open API, QR codes, digital assets, regulators, providers, enablers, and infrastructure

The framework highlights this dual view. The Layered Evolution Model shows the progression from early banking reforms to mobile money, fintech growth, and today’s interoperable systems. The Ecosystem Map shows the resulting market structure, centered on the Consumer and MSMEs, supported by the interdependent roles of Providers, Enablers, Regulators, and Infrastructure.

Foundations of Kenya’s Financial System

Early Banking in Kenya: Colonial Origins and Post-Independence Financial Reforms

Kenya’s formal banking system originated during the colonial period, when financial services were designed to support trade finance, settler agriculture, and government administration. Before independence, currency and monetary functions were handled by the East African Currency Board, and formal banking services were concentrated among foreign banks, with limited access for the majority of Kenyans.

After independence in 1963, the government prioritized financial sovereignty by establishing the Central Bank of Kenya in 1966, taking over currency issuance and regulatory functions, and supporting the creation of locally owned institutions such as the Co‑operative Bank of Kenya to extend services beyond elite urban clients.

Summary: The Hidden Precondition Kenya’s digital finance success rests on decades of institutional groundwork. Without a central bank, liberalized markets, and competitive retail banking, mobile money would not have scaled safely or sustainable.

Financial Liberalization in Kenya: Market Expansion and Private Sector Growth

Major financial sector reforms in the 1980s and 1990s liberalized interest rates, reduced state controls, and encouraged private sector participation. These reforms improved competition, expanded product diversity, and enabled new banking models to emerge, which in turn supported greater outreach to previously underserved populations.

Retail‑focused banks like Equity Bank took advantage of the more open environment by targeting low‑income customers and small businesses that had limited access to formal banking services outside urban centers.

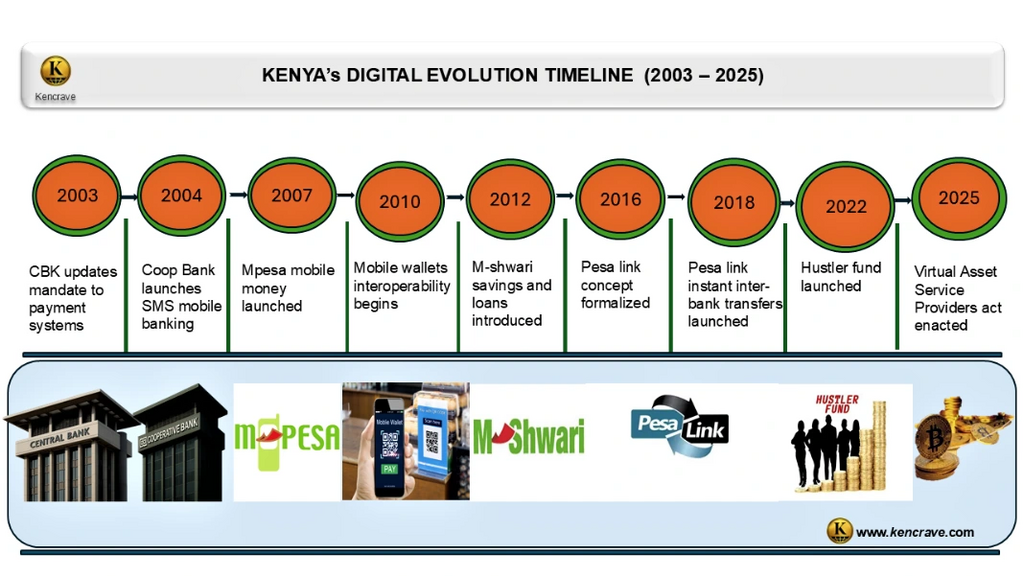

Timeline of Kenya’s Digital Financial Evolution Key Milestones in Kenya’s Digital Finance and Mobile Money Growth

Kenya digital finance timeline 2003–2025 highlighting CBK reforms, M-Pesa launch, mobile wallets, M-Shwari, PesaLink, Hustler Fund, and Virtual Asset Service Providers Act.

TheMobile Money Inflection Point

1. M-Pesa in Kenya: How Mobile Money Transformed Financial Access

The launch of M‑Pesa by Safaricom in March 2007 marked a significant inflection point in Kenya’s financial system. M‑Pesa provided a way for users to store and transfer money using mobile phones and a nationwide agent network, eliminating the need for traditional bank accounts and physical branches for many everyday transactions. This service was designed as an electronic payment and store of value system accessible on ordinary mobile devices and quickly expanded its user base due to the simplicity and reach of the mobile platform.

Kenya’s financial regulators adopted a cautious but facilitative approach that allowed mobile money to scale while monitoring risks to consumers and systemic stability. This balance of oversight and flexibility is widely cited as a key factor in enabling the mobile money sector to grow without unduly constraining innovation or financial inclusion.

Summary: Why M-Pesa Worked M-Pesa succeeded not just because of technology, but because regulators allowed it to grow outside rigid banking rules while maintaining oversight. This balance unlocked rapid adoption without eroding trust. 2. Mobile Money Adoption in Kenya and Its Impact on Financial Inclusion

Mobile money adoption expanded rapidly across Kenya in the years after M‑Pesa’s launch. Data from the 2024 FinAccess Household Survey shows that formal financial inclusion rose from approximately 27% of adults in 2006 to 80% by the early 2020s, with mobile money accounts accounting for the majority of this increase. By 2024, formal financial access reached around 85% of adults, reflecting near‑universal access to some form of formal financial service, driven largely by widespread mobile money use.

These changes show how a combination of technological adoption, regulatory support, and demand for accessible financial tools can reshape a country’s financial landscape. Mobile money has become a central component of Kenya’s digital finance market and a major driver of expanded financial inclusion.

Summary: Access vs Depth Kenya solved financial access faster than almost any country. The remaining challenge is financial depth: savings, insurance, pensions, and long-term credit still lag behind transactional use.

Bar Chart showing: Kenya’s Mobile Money Transaction Intensity (2007–2024)

Data source: Central Bank of Kenya.

Kenya Mobile Money Transactions (2007–2024): Key Observations and Insights

Mobile money transaction volumes in Kenya have surged from KSh 16.3 billion in 2007 to KSh 8,697.7 billion in 2024.

2007–2009: Transactions jumped from KSh 16.3 billion to KSh 473.4 billion, reflecting rapid early adoption after launch.

2010–2015: Growth was steady, with annual increases of KSh 300–400 billion, showing market consolidation and rising trust in mobile money.

2016–2020: Growth picked up again, surpassing KSh 5 trillion by 2020, driven by new services like merchant payments and government disbursements.

2021–2024: Growth slowed, with 2023 showing a near plateau at KSh 7,953.9 billion compared to KSh 7,908.8 billion in 2022, suggesting possible market saturation.

Summary: Signs of Saturation Mobile money growth has slowed as user adoption nears saturation. Future expansion will come from merchant payments, SME services, and integrated financial products not new users. Mobile money is now a core financial service in Kenya.

Digital Banking and Fintech Development

1. Digital Banking in Kenya: How Banks Adapted to Mobile and Online Finance

As mobile money and digital financial services expanded in Kenya, traditional banks accelerated their digitization efforts. Mobile banking applications, USSD services, and wallet integrations became standard offerings as banks responded to changing customer preferences and widespread mobile connectivity. Rising smartphone adoption and lower data costs have supported this shift, increasing mobile banking usage across urban and rural populations.

Despite these digital changes, banks remain central to deposit mobilization, large-scale credit provision, and regulatory compliance. The move toward digital channels has improved operational efficiency and customer access, but banks continue to serve as core financial intermediaries within the broader financial system.

Summary: Banks Were Not Displaced Fintech and mobile money changed delivery channels, not financial fundamentals. Banks remain central to deposits, credit, and compliance, while fintech firms expand reach and efficiency.

2. Fintech Growth in Kenya: Digital Lending, Payments, and Insurtech

Kenya hosts one of Africa’s most developed fintech ecosystems, featuring a large and diverse set of firms operating across various financial technology segments, including payments, digital lending, and insurtech. The number of fintech startups in Kenya has grown rapidly, with hundreds of firms active across multiple sub‑sectors, reflecting the country’s supportive environment for fintech innovation (Business Daily Africa, 2025).

Digital lenders, such as Tala and Branch, expanded access to short-term credit by utilizing alternative data sources and mobile platforms, thereby improving credit access for many users beyond traditional bank customers (Kenya Bankers Association, 2023).

While this expansion increased financial access, it also raised concerns about consumer over‑indebtedness and data protection, prompting regulators to strengthen licensing and consumer protection requirements for digital lenders. Insurtech and digital investment platforms remain emerging areas with growth potential due to relatively low market penetration compared to payments and lending.

Summary: Where Innovation Is Concentrated Kenya’s fintech ecosystem is strongest in payments and digital lending. Insurtech, wealth tech, and long-term savings remain underdeveloped, representing the next growth frontier.

The Current Market Structure of Kenya’s Digital Finance Market

FinAccess survey data shows a clear hierarchy in financial product use among Kenyan adults. Mobile money services are used by more than 80 percent of adults, while bank account ownership is lower but trending upward. Insurance, pension, long-term savings, and investment products have much lower usage rates compared to mobile money and banking services.

This indicates that most users engage with basic transactional tools rather than deeper financial products. These patterns suggest that while Kenya has largely solved financial access, the depth of financial engagement remains limited (Central Bank of Kenya, 2024).

2. Financial Product Usage in Kenya: Mobile Money, Banking, and Financial Depth

Mobile money systems process large transaction volumes, reflecting their central role in Kenya’s financial landscape. Central Bank of Kenya payment systems data show that mobile money monthly transaction values reached hundreds of billions of Kenyan shillings, and the total count of active subscriptions and agents continues to expand.

This scale reflects the broad use of mobile money but should not be conflated with market revenue or direct economic contribution. Independent market research projects Kenya’s digital payments market to grow into the low to mid-teens in billions of US dollars by the late 2020s, driven by e-commerce, merchant payments, and wallet usage (Central Bank of Kenya, 2025).

3. Digital Finance Regulation in Kenya: Payments, Digital Credit, and Consumer Protection

Kenya’s regulatory framework has changed with innovation in financial services. The Central Bank of Kenya’s National Payments System regulations require mobile money platforms to support interoperability and govern payment service providers. TheCentral Bank of Kenya (Digital Credit Providers) Regulations, 2022require digital lenders to be licensed and follow consumer protection and data privacy rules under the Data Protection Act, 2019.

Regulatory sandboxes allow firms to test new products in a controlled environment before full launch. TheCapital Markets Authority’s Regulatory Sandbox Policy Guidance Note 2019 lets fintech firms trial innovations under oversight, helping regulators balance innovation with market stability.

Summary: Regulation as an Enabler Kenya’s regulators consistently prioritized flexibility over restriction. Sandboxes, interoperability rules, and digital credit licensing allowed innovation while gradually strengthening consumer protection.

4. Cryptocurrency Adoption in Kenya and the Regulatory Response

Chainalysis data from the 2023 Global Crypto Adoption Index show that Kenya is one of the leading countries in peer-to-peer cryptocurrency usage, with high P2P exchange trade volume driven in part by remittances and informal trading outside the formal financial system.

Kenya’s Digital Asset Policy and the Virtual Asset Service Providers Act

The Kenyan government has began formal policy work on digital assets, including the passage of the 2025 Virtual Asset Service Providers Act, to regulate virtual asset service providers and address consumer protection and anti-money-laundering concerns. Kenya has not issued a central bank digital currency as of 2025, and recent policy updates note that the case for a CBDC is not compelling at this time.

Summary: High Usage, Cautious Policy Kenya ranks high in peer-to-peer crypto usage, but policymakers remain cautious. Regulation is evolving to manage risk without endorsing digital assets as core financial infrastructure.

Future of Digital Finance in Kenya: Growth Opportunities and Systemic Risks

Kenya’s digital finance sector is expected to grow through stronger payment systems, expansion of SME digital lending, growth in insurtech, and deeper integration of financial platforms. At the same time, the sector faces risks from household over-indebtedness, rising cybercrime threats, regulatory lag, and uneven levels of digital literacy among users (Research and Markets report, 2025).

Summary: What Comes Next Kenya’s next phase of digital finance growth depends less on technology and more on trust: cybersecurity, digital literacy, responsible credit, and institutional capacity will determine outcomes.

Blockchain and Digital Assets in Kenya: Disruption or Complement to Mobile Money?

Blockchain and digital assets could disrupt platforms like M-Pesa by enabling low-cost, cross-border, peer-to-peer transactions without intermediaries, which may reduce transaction fee revenues. At the same time, these technologies can help manage existing risks through smart contracts that improve loan transparency and reduce fraud, and through blockchain-ledgers that support real-time regulatory oversight. Kenya’s challenge will be to adopt these innovations within strong regulatory frameworks to promote financial inclusion while avoiding systemic risks.

According to the World Data Bank, the digital finance market will expand steadily rather than explode. Growth will depend on institutional trust, clearer regulation, and broader digital skills and infrastructure. World Bank initiatives like the Kenya Digital Economy Acceleration Project stress that closing gaps in digital literacy and strengthening trust are essential for sustained growth.

Summary: Threat or Tool? Blockchain could pressure mobile money fees over time, especially in cross-border payments. Its impact will depend on usability, regulation, and whether it complements existing systems rather than bypassing them.

Who Powers Kenya’s Digital Finance Ecosystem? Regulators, Banks, Fintechs, and MNOs

Regulators and policymakers: The Central Bank of Kenya oversees banks, mobile money operators, payment service providers, and digital credit providers. The Capital Markets Authority regulates digital investment platforms and runs the regulatory sandbox. The Office of the Data Protection Commissioner enforces data privacy rules.

Mobile network operators: Safaricom leads through M-Pesa. Airtel Kenya and Telkom Kenya support competing mobile money platforms. These firms provide the infrastructure, agent networks, and distribution that anchor digital finance adoption.

Commercial banks: Banks such as Equity Bank, KCB, Co-operative Bank, and Absa Kenya provide deposits, credit, treasury services, and compliance functions. They integrate mobile and digital channels with core banking services.

Fintech companies: Payment firms, digital lenders like Tala and Branch, insurtech startups, and wealth tech platforms drive product innovation. They expand access to payments, short-term credit, and emerging digital financial products.

Agents and merchants: Mobile money agents, retail merchants, and SMEs enable cash-in and cash-out services, merchant payments, and last-mile access across urban and rural areas.

Consumers and businesses: Households, microenterprises, SMEs, and corporates use mobile money, banking, and fintech services for payments, savings, credit, and business operations.

Development partners and investors: Institutions such as the World Bank, GSMA, and private investors fund infrastructure, research, pilots, and scale-up of digital finance solutions.

Summary: Coordination Is the Advantage Kenya’s digital finance strength lies in coordination. Regulators, banks, mobile operators, fintech firms, agents, and consumers all play defined roles within a shared framework.

Policy Recommendations for Kenya’s Digital Finance Sector (Short-Term Priorities)

Policymakers should strengthen enforcement of existing digital credit and data protection regulations. Over-indebtedness and misuse of customer data remain active risks. Better supervision improves trust and reduces systemic fragility.

Regulators should expand and speed up regulatory sandbox approvals for insurtech, SME finance, and wealth platforms. Payments are mature, but these segments remain underdeveloped.

Investors should focus on fintech firms that improve efficiency within the existing ecosystem. Examples include merchant payment tools, SME cash flow management, and compliance technology. These address real gaps without betting on untested consumer behavior.

Summary: Short Term Action The immediate priority is trust: enforcing digital credit rules, protecting consumer data, and improving supervision of fast-growing fintech segments.

Medium-Term Strategies for Fintech Growth and Financial Deepening in Kenya

Policymakers should promote deeper financial usage, not just access. Incentives for long term savings, pensions, and micro insurance can shift users from transactional wallets to wealth-building products.

Interoperability should be enforced across banks, mobile money platforms, and fintech wallets to reduce market fragmentation and lower transaction costs.

Investors should target scalable platforms that embed finance into non-financial services such as agriculture, logistics, health, and e-commerce. Embedded finance improves adoption and unit economics.

Summary: Medium Term Action Growth will come from financial deepening: pensions, insurance, SME finance, and embedded financial services not from basic payments.

Long-Term Policy and Investment Priorities for Kenya’s Digital Finance Infrastructure

Policymakers should invest in national digital skills and cybersecurity capacity. Digital finance growth now depends more on trust and resilience than on access.

Clear, adaptive frameworks for digital assets and cross-border payments are needed to prevent regulatory arbitrage while supporting innovation.

Investors should prioritize infrastructure-level opportunities such as payment rails, regtech, credit bureaus, and identity systems. These offer lower volatility and long-term returns as the ecosystem matures.

Summary: Long Term Action Long-term resilience depends on infrastructure investments: digital skills, cybersecurity, identity systems, and adaptive regulation for cross-border finance and digital assets.

Key Takeaways

Kenya’s digital finance success followed a deliberate, step-by-step path built on early banking and regulatory reforms. These foundations enabled mobile money and later fintech growth.

M-Pesa marked the major turning point from bank-led to user-centered finance. It drove financial inclusion from 27% in 2006 to over 85% by 2024.

Regulation balanced innovation and stability. Policies from 2003 to 2025 created trust, managed risk, and supported sector growth.

The ecosystem relies on collaboration between providers, enablers, regulators, and infrastructure.

Access to digital finance is widespread, but advanced services remain underused. Future growth depends on expanding savings, insurance, and responsible credit use.

Innovation has moved beyond payments to savings, lending, interoperable transfers, and digital assets. SME finance and embedded services will drive the next phase.

Growth prospects are strong but face risks like cybercrime and over-indebtedness. Progress depends on better skills, trust, and inclusive policies.

Summary: Core Lesson Kenya’s experience shows that inclusive digital finance is built through sequencing, regulation, and institutional trust not disruption alone.

Frequently Asked Questions: Kenya’s digital finance model

1. What makes Kenya’s digital finance model different from other countries?

Kenya combined mobile network reach, agent-based distribution, and flexible regulation early. Mobile money scaled before smartphones or widespread banking access, which shaped user behavior and market structure.

2. Is mobile money growth slowing in Kenya?

Transaction value growth has slowed since 2022, suggesting saturation in basic payments. Growth is shifting toward merchant payments, SME services, and integrated financial products rather than new users.

3. Have banks been displaced by mobile money and fintech?

No. Banks remain central to deposits, large-scale lending, and regulation. Mobile money and fintech changed delivery channels and customer interfaces, not the core role of banks.

4. What are the main risks in Kenya’s digital finance sector?

Household over-indebtedness, cybercrime, data misuse, and uneven digital literacy are the key risks. Regulatory capacity and consumer education are now as important as innovation.

5. Are cryptocurrencies a threat to mobile money platforms?

In the short term, no. In the long term, blockchain-based payments could pressure fees on cross-border and peer-to-peer transfers. The impact depends on regulation, usability, and trust.

6. What is the next growth frontier for Kenya’s digital finance ecosystem?

SME finance, insurtech, long-term savings, and embedded financial services. These areas deepen economic impact beyond payments.

7. Can other countries replicate the Kenya model?

Elements can be adapted, but direct replication is unlikely. Kenya’s success depended on timing, regulatory choices, and market structure that are hard to reproduce exactly.

The World Economic Forum (WEF) Annual Meeting 2026 in Davos, Switzerland (January 19-23) convened nearly 3,000 leaders under the theme “A Spirit of Dialogue.” The meeting reflected a convergence of geopolitical, economic, and environmental priorities, with direct implications for Africa and Kenya in climate finance, refugee integration, and positioning Nairobi as a financial hub.

Keynote Speakers and Highlights at Davos 2026

President Donald Trump (United States): Stressed the importance of energy security and warned against overdependence on rare-earths from single regions, calling for “balanced supply chains that protect national sovereignty.”

Ursula von der Leyen (European Commission President): Urged accelerated climate finance pledges, noting that “Africa’s renewable energy potential is not just regional; it is central to Europe’s net-zero future.”

President William Ruto (Kenya): Presented the Shirika Plan as a model for refugee integration, stating that “refugees must be seen as contributors to resilience, not burdens,” while positioning Nairobi as a rising financial hub.

President Cyril Ramaphosa (South Africa): Highlighted South Africa’s BRICS role and green hydrogen investments, emphasizing that “Africa must shape the rules of sustainable finance, not just follow them.”

President Bola Tinubu (Nigeria): Spoke on Nigeria’s energy markets, balancing oil exports with renewable diversification, declaring that “Africa’s energy future must be both profitable and sustainable.”

President Abdel Fattah el-Sisi (Egypt) and King Mohammed VI (Morocco): Showcased North Africa’s solar and wind projects as critical to Europe’s energy transition, with el-Sisi noting “the Sahara sun can power continents,” and King Mohammed VI adding that “Morocco’s wind corridors are bridges to shared prosperity.”

Historical Context of Davos

Since its founding in 1971, WEF has evolved from a European management symposium into the world’s premier platform for global cooperation. Over the decades, it has addressed Cold War tensions, globalization, and digital transformation. In 2026, Davos reaffirmed its role as a neutral convening space amid geopolitical fragmentation, echoing its legacy of bridging divides.

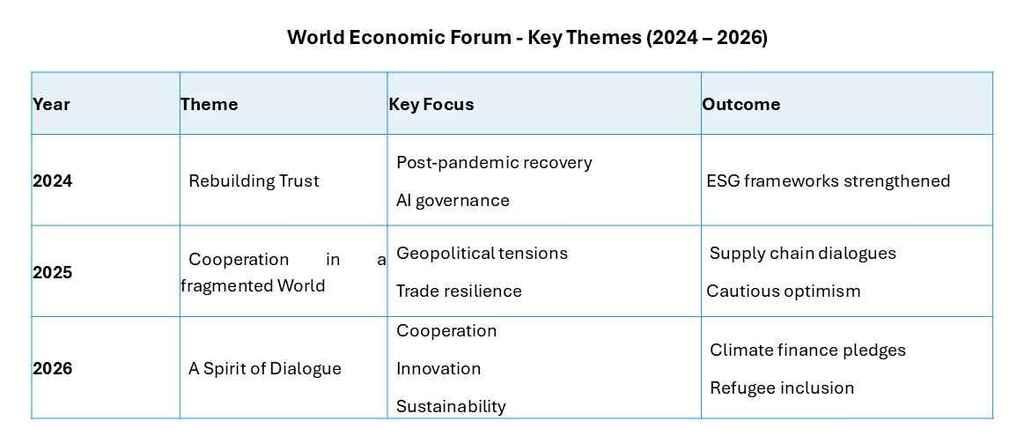

World Economic Forum 2024–2026 key themes table highlighting global priorities in trust, cooperation, innovation, sustainability, and climate finance outcomes.

Davos themes evolved from rebuilding trust in 2024, to managing fragmentation in 2025, and finally to dialogue and Africa’s strategic role in 2026.

Comparative Analysis: WEF Davos 2025 vs. WEF Davos 2026

Tone Shift: WEF DAVOS 2025 emphasized “fragmentation” and the risks of geopolitical breakdown while the WEF DAVOS 2026 pivoted to “dialogue,” signaling cautious optimism and renewed multilateralism.

Economic Focus: WEF DAVOS 2025 prioritized trade resilience and supply chain security while the WEF DAVOS 2026 shifted toward green growth and inclusive finance, spotlighting Africa’s renewable energy potential.

Security Lens: WEF DAVOS 2025 centered on geopolitical conflict management while WEF DAVOS2026 broadened security to include climate resilience and refugee stability, aligning with Kenya’s Shirika Plan.

ESG Evolution: WEF DAVOS 2025 ESG debates were corporate-driven while the WEF DAVOS 2026 ESG expanded to national policies, refugee inclusion, and indigenous rights, making Africa’s adaptation financing gap a global priority.

Key Insight: Davos 2026 marked a transition from defensive postures to proactive collaboration. Implication: Kenya and Africa gained visibility as strategic partners rather than peripheral actors.

Security Risks and Strategic Importance

Davos 2026 highlighted geopolitical risks:

NATO cohesion amid conflicts in Eastern Europe.

Cybersecurity threats from AI misuse.

Africa’s role in peacekeeping and refugee integration.

Economic Coercion and Resource Competition

Economic discussions focused on:

Green energy transitions and rare-earth supply chains.

Africa’s potential as a renewable energy hub.

Nairobi’s push to become a regional financial center via the Nairobi International Financial Centre (NIFC).

Geopolitical Coercion and International Relations

Davos underscored fractures in multilateralism, with U.S., EU, and China competing for influence. African leaders emphasized equitable access to climate finance and warned against neo-colonial resource extraction.

Kenya showcased its Shirika Plan for refugee integration as a model of resilience.

Kenya's Shirika Plan emerged as a flagship initiative at Davos 2026, embodying the forum's call for inclusive resilience. The plan transforms the long-standing refugee camps of Dadaab and Kakuma, home to over 500,000 refugees, into integrated settlements with municipal status. This grants refugees access to public services, land rights, and economic opportunities, while fostering social cohesion with host communities.

By aligning with the Global Compact on Refugees and the Comprehensive Refugee Response Framework, the Shirika Plan positions refugee integration as a development opportunity rather than a humanitarian burden. Davos leaders recognized this approach as a scalable model for other refugee-hosting nations, linking it directly to ESG goals, climate adaptation, and sustainable finance.

Key Insight: Africa is reframing itself as a partner, not a recipient, in global governance. Implication: Wef 2026Davos outcomes could shift Africa’s bargaining power in multilateral forums.

Environmental and ESG Considerations

Climate change dominated World Economic Forum in Davos 2026, with pledges to accelerate net-zero transitions.

Greenland’s ice melt was cited as a global warning, but Africa’s adaptation financing gap was spotlighted.

Indigenous rights and refugee inclusion were linked to ESG frameworks.

Key Insight: ESG debates now extend beyond corporations to national policies and refugee integration. Implication: Kenya’s refugee inclusion strategy positions it as a leader in ESG-aligned governance.

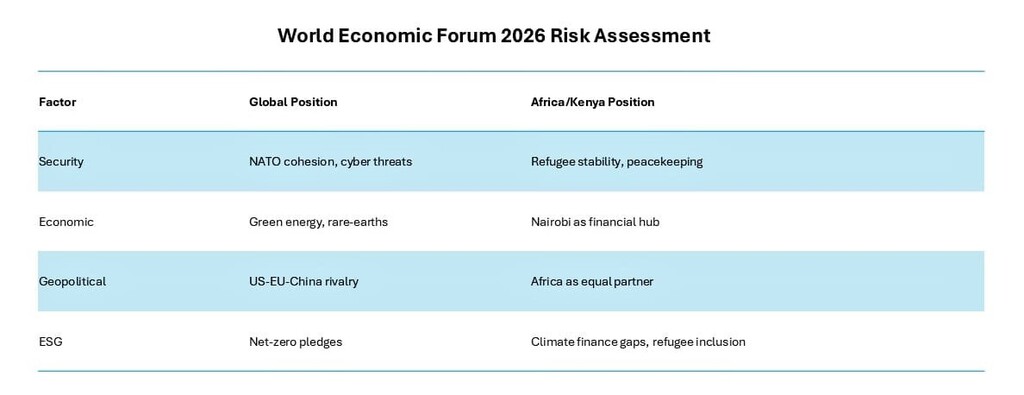

WEF Risk Assessment 2026

World Economic Forum 2026 Risk Assessment table comparing global vs Africa/Kenya positions on security, economy, geopolitics, and ESG sustainability challenges.

Davos 2026 positioned Africa at the center of global risk mitigation, linking security, economic, geopolitical, and ESG challenges to highimpact outcomes.

WEF 2026 Global Consequences

WEF Davos 2026 outcomes will ripple across continents:

Energy markets: Africa’s renewable energy potential could reshape supply chains.

Climate finance: Equitable funding is critical to prevent instability in vulnerable regions.

Refugee governance: Kenya’s Shirika Plan may become a global model.

Financial hubs: Nairobi’s positioning could attract fintech and ESG capital.

KeyInsight: WEF Davos 2026 reframed Africa from a peripheral actor to a strategic partner in global resilience. Implication: Kenya’s leadership in finance, climate, and refugee integration could redefine its global role.

Strategic Recommendations for Key Stakeholders

Kenyan Government

Strengthen NIFC governance for ESG capital.

Scale Shirika Plan globally.

Expand geothermal, wind, and solar projects.

Position Nairobi as fintech hub.

Secure bilateral climate finance deals.

African Governments

Coordinate renewable energy projects.

Push for equitable climate finance.

Guard against neo-colonial extraction.

Integrate refugee inclusion into development.

Build green hydrogen & rare-earth alliances.

Investors

Prioritize Africa’s renewable frontier.

Support Nairobi’s NIFC for ESG investments.

Back refugee integration projects.

Diversify supply chains via rare earths.

Align portfolios with adaptation finance needs.

Multilateral Institutions

Close Africa’s climate finance gap.

Recognize refugee inclusion as ESG-aligned development.

Provide technical support to financial hubs.

Facilitate access to green technologies.

Amplify Africa’s voice in global governance.

Key Takeaways

Security Dialogue: Refugee stability is now part of global security.

Economic Growth: Africa is central to green energy and finance.

Geopolitical Balance: Multilateralism is fragile, Africa seeks equal footing.

ESG Flashpoint: Climate finance and refugee inclusion dominate.

Global Fallout: Africa’s positioning could reshape alliances and markets.

FAQs

1. Why is Davos important for Africa?

It provides a platform to demand equitable climate finance and showcase Africa’s renewable energy potential.

2. How did Kenya feature at Davos 2026? Kenya promoted Nairobi as a financial hub and highlighted its Shirika Plan for refugee integration. 3. What ESG issues were discussed?

Climate adaptation, indigenous rights, and refugee inclusion were central. Kenya's Shirika Plan was highlighted as a concrete example of refugee inclusion in action, demonstrating how transitioning camps to integrated settlements can drive social sustainability (the 'S' in ESG) while creating stability that attracts investment. 4. How does Davos affect global markets?

Commitments on green energy and rare-earth supply chains could shift investment flows toward Africa.

5. What risks remain?

Financing gaps, geopolitical rivalries, and fragile multilateralism could undermine progress.

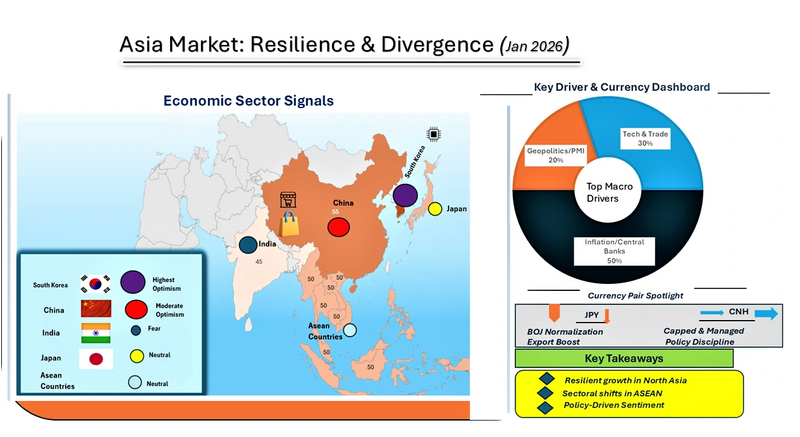

Asia Market Outlook 2026 points to a cautiously risk-on environment in early Q1, supported by easing inflation, resilient exports, and policy-managed stability across China, Japan, and South Korea. This Asia macro outlook highlights selective strength in Asian equities, particularly AI and semiconductor supply chains, alongside contained FX volatility, with the yen softening and the offshore yuan (CNH) capped. Overall, the Asia equity outlook remains constructive but uneven, with performance increasingly driven by policy signals, FX dynamics, and sector-specific fundamentals rather than broad beta.

Asia Macro Outlook

The macro environment leaned cautiously risk-on, supported by easing inflation pressures across East Asia and resilient export flows despite lingering global trade frictions. According to the World Bank’s January 2026 Global Economic Prospects, East Asia and Pacific growth held near 4.8% in 2025, with China at 4.9%, buoyed by fiscal stimulus and consumption resilience. J.P. Morgan’s Asia Outlook 2026 highlighted AI-driven industrial buildouts in China, South Korea, and Taiwan as structural tailwinds for semiconductors and technology.

Asia Equity Market Outlook

Equity markets reflected this resilience: the Nikkei 225 extended gains on domestic demand optimism, while the Shanghai Composite stabilized after property-sector stress. Southeast Asian indices (Vietnam, Indonesia) showed selective strength, benefiting from supply-chain diversification.

Currency markets remained steady, with the CNH capped by cautious capital flows, while the yen softened modestly amid BOJ’s gradual policy normalization. Credit spreads across Asia stayed contained, reflecting confidence in disinflation and policy support.

Sector Leadership

Technology & semiconductors: Outperformance in Korea and Taiwan on global AI demand

Consumer discretionary: Recovery in China, supported by stimulus

Financials: Stable, though property-linked exposures weigh on sentiment

Defensives: Utilities and staples resilient in Japan and ASEAN markets

Key Drivers Ahead for Asia Market Outlook

China PMI releases, BOJ policy signals, and regional inflation prints will test whether optimism sustains into Q1. Sentiment momentum will remain sensitive to policy communication and FX stability.

Visual Summary: Asian Macro Drivers (Focus Allocation)

Inflation prints (CPI/PPI): 25%

Central bank decisions (BOJ, PBOC, RBI): 25%

PMIs & industrial data: 20%

Tech/semiconductor earnings: 20%

Credit spreads/liquidity: 10%

Asia macro drivers Jan 2026 pie chart showing inflation, central bank decisions, tech earnings, PMI data, and credit spreads.

Inflation data and central bank policy dominate sentiment formation, while PMIs and tech earnings reflect Asia’s manufacturing resilience and AI-driven growth. Credit conditions remain a stabilizing, secondary factor.

Asia Fear & Greed Index Snapshot

China: 55

Japan: 50

South Korea: 60

India: 45

ASEAN (Vietnam, Indonesia): 50

Asia Fear and Greed Index Jan 2026 bar chart comparing investor sentiment in China, Japan, South Korea, India, and ASEAN.

Optimism is strongest in South Korea on semiconductor momentum, moderate in China, neutral in Japan/ASEAN, and cautious in India due to inflation pressures and capital flow sensitivity.

Supports Japanese export competitiveness (autos, electronics)

Raises import costs for energy/raw materials

Signals BOJ normalization path, tempering regional bond risk appetite

Increases hedging demand for ASEAN corporates with yen exposure

Capped CNH (Offshore Yuan)

Reflects managed capital flows and volatility control

Supports confidence in China’s policy discipline

Constrains offshore liquidity and arbitrage flows

Reduces FX volatility for regional trade partners

Trade Implication (Directional, Non‑Prescriptive)

The market environment favors targeted risk-taking rather than broad market exposure. Technology and semiconductor companies in North Asia especially in South Korea and Taiwan, are better positioned to outperform, supported by strong AI investment and resilient exports. Japanese equities also benefit in the near term from a weaker yen, which supports exporters.

By contrast, property-related financials and highly indebted cyclical sectors remain vulnerable. Across the region, the more attractive opportunities are in export-focused manufacturing and AI infrastructure, while a cautious approach to currencies and credit remains appropriate, as gradual policy tightening and managed capital flows are likely to limit sharp upside moves.

Asia Market Surprise Risk to Watch

AI Investment Slowdown If global spending on AI infrastructure slows more than expected due to weaker earnings, tighter regulations, or large tech companies pulling back on investment, it would quickly hurt semiconductor companies in South Korea and Taiwan and their suppliers.

This would weaken the current positive outlook for the sector, likely causing investor sentiment to turn negative, credit conditions in tech to worsen, and money to move back into more defensive and domestically focused sectors. Asia Market Outlook 2026: Scenario Framework (Next 1–3 Months)

Base Case (est. 60% probability)

Asia’s market outlook remains cautiously positive. Inflation continues to ease and central banks are tightening policy slowly and carefully. In China, government stimulus is helping consumer spending and keeping growth stable without fueling another property boom.

Investment in AI is supporting earnings growth in South Korea and Taiwan, while Japan benefits from a weaker yen without aggressive interest rate hikes from the Bank of Japan. Equity markets are rising gradually in selected areas, credit conditions remain stable, and currency markets are relatively calm.

Bull Case (est. 25% probability)

If global demand improves more than expected and policymakers communicate more clearly, investor confidence would rise. Consumer spending in China would strengthen further, manufacturing data across North Asia would improve, and investment in AI would last longer than currently expected.

At the same time, the yen could weaken further without policy surprises, supporting Japanese stocks. Increased capital inflows would lift equity markets across the region and improve credit conditions, allowing Asia to outperform other emerging markets thanks to stronger growth visibility and leadership in technology.

Bear Case (est.15% probability)

If policymakers send mixed signals or an unexpected external shock occurs, investor confidence could quickly weaken. A pullback in AI spending, renewed stress in China’s property sector, or sudden swings in the yen or offshore yuan could push stock markets lower and worsen credit conditions.

In this environment, investors would likely shift money into safer U.S. dollar assets, causing Asian equities to underperform and driving a rotation toward more defensive and domestically focused sectors.

Key Takeaways: Asia Market Outlook 2026 Q1

Resilient Growth Amid Global Frictions. East Asia’s steady GDP growth and China’s stimulus underpin regional stability despite trade tensions.

Policy-Driven FX and Sentiment . Softened yen and capped CNH anchor currency stability, while sentiment is strongest in South Korea and most cautious in India.

The United States is undergoing a supply chain realignment, driven by global disruptions, geopolitical tensions, and the need for greater systemic resilience. An era defined by cost-focused globalization and just-in-time models prioritized efficiency at the expense of resilience (The World Economic Forum, 2020).

As reported by Al Jazeera in 2021, events like the COVID-19 pandemic and the 2021 Suez Canal incident exposed the risks of depending on distant, centralized supply chains. These crises revealed that low cost and speed were insufficient, prompting a strategic resurgence of priorities like stability, security, and oversight.

This transformation is now widely described as the US Supply Chain Transformation. It marks a move away from hyper-globalized sourcing toward a more regional, diversified, and politically aligned production system. Understanding how this transformation emerged and how it is being executed is essential for businesses, policymakers, and investors navigating the next phase of global trade.

From Just-in-Time Efficiency to Systemic Fragility

For decades, the dominant supply chain model relied on just-in-time production. Goods moved from Asian factories to US markets with minimal inventory and precise scheduling. The system reduced costs and boosted margins, but it assumed stable geopolitics, predictable transportation, and uninterrupted global trade.

Pandemic-related factory shutdowns, port congestion, container shortages, and record freight rates broke delivery timelines. The Ever Given incident alone delayed nearly $10 billion in trade per day (Bloomberg, 2021). These shocks exposed the risk of relying on single-region manufacturing for essential goods such as semiconductors, pharmaceuticals, and consumer staples.

What emerged was not a temporary disruption, but a structural failure. Firms and governments began to reassess supply chains as strategic assets rather than cost centers.

What Defines the US Supply Chain Transformation

The US Supply Chain Transformation is a coordinated shift led by both public policy and corporate strategy. Its objective is to reduce dependence on single-source overseas manufacturing, particularly in China, by diversifying production locations and shortening supply lines.

Three approaches define this transition.

Reshoring focuses on bringing manufacturing and critical supply chains back to the United States.

Nearshoring shifts production to geographically close partners, primarily Mexico and Canada.

Friend-shoring relocates supply chains to countries with strong political alignment, trade ties, and stable institutions.

These strategies form the backbone of a more regional and risk-aware supply chain model.

The Forces Driving the Transformation

Several forces made the old model unsustainable.

Geopolitical Tensions and National Security: The US-China trade conflict highlighted the vulnerability of relying on a strategic competitor for semiconductors, rare earths, and pharmaceuticals (The New York Times, 2025). The war in Ukraine exposed the risk of relying on adversarial countries for resources.

High Cost of Supply Chain Distribution: During the pandemic, delays and freight price spikes erased decades of cost savings from global sourcing. OECD data shows that logistical breakdowns outweighed efficiency gains, forcing businesses to reassess total supply chain cost rather than unit price alone.

Push for Resilience: Companies began shifting toward just-in-case approaches by holding safety stock, adding backup suppliers, and diversifying production footprints. Predictability and shock absorption replaced marginal cost optimization.

Government Legislation: Government policy accelerated the shift. The CHIPS and Science Act of 2022 provides over $52 billion to boost domestic semiconductor production. The Inflation Reduction Act of 2022 introduced tax credits for clean energy, electric vehicles, and battery production within North America.

Consumer and Investors Demand: Consumer and investor expectations also evolved. Buyers and investors increasingly value supply chain ethics, sustainability, and reliability. Firms with visible, local, and resilient operations gained reputational and strategic advantages.

The 3 Strategies of the Supply Chain Transformation

1. Reshoring and the Return of Domestic Manufacturing

Reshoring is rebuilding US industrial capacity after decades of offshoring. Investment is concentrated in advanced manufacturing, semiconductors, clean energy, and electric vehicles (Tech News World, 2025).

Major chipmakers are leading the trend. Intel is expanding fabrication plants in Arizona and building a large-scale semiconductor hub in Ohio. TSMC is constructing a multi-fab campus in North Phoenix. Samsung is developing a major semiconductor complex in Texas that combines production and research.

These projects strengthen intellectual property protection, create high-skilled jobs, and reduce exposure to global logistics shocks. They also face constraints. Labor costs are higher, and the supply of skilled manufacturing talent remains limited.

2.Nearshoring: The “China +1” Strategy

Nearshoring is among the most popular and scalable supply chain strategies, with Mexico being the primary beneficiary (Boston Consulting Group, 2024). Companies are adopting a China +1 model. They maintain Asian production for global markets while shifting US-focused output to Mexico. This approach helps reduce risk without a complete exit from Asia.

Key Structural Advantages of Mexico:

Proximity enables faster and cheaper truck and rail transport.

The USMCA trade agreement provides tariff-free access and regulatory predictability.

Shorter transit times reduce inventory risk and improve responsiveness.

As a result, Mexico has become a critical node in North American manufacturing, particularly for automotive, electronics, and consumer goods.

3.Friend-Shoring and Trusted Supply Networks

Friend-shoring adds a geopolitical dimension to supply chain design. Production is relocated to countries with strong diplomatic ties, stable governance, and aligned economic interests (The World Economic Forum, 2023).

Each partner plays a specific role. Canada supplies critical minerals. Japan and South Korea provide advanced electronics and battery technology. Australia supports lithium and raw material supply. India offers an alternative manufacturing hub with scale and growth potential.

The result is a distributed but trusted network that reduces exposure to political pressure and trade disruption.

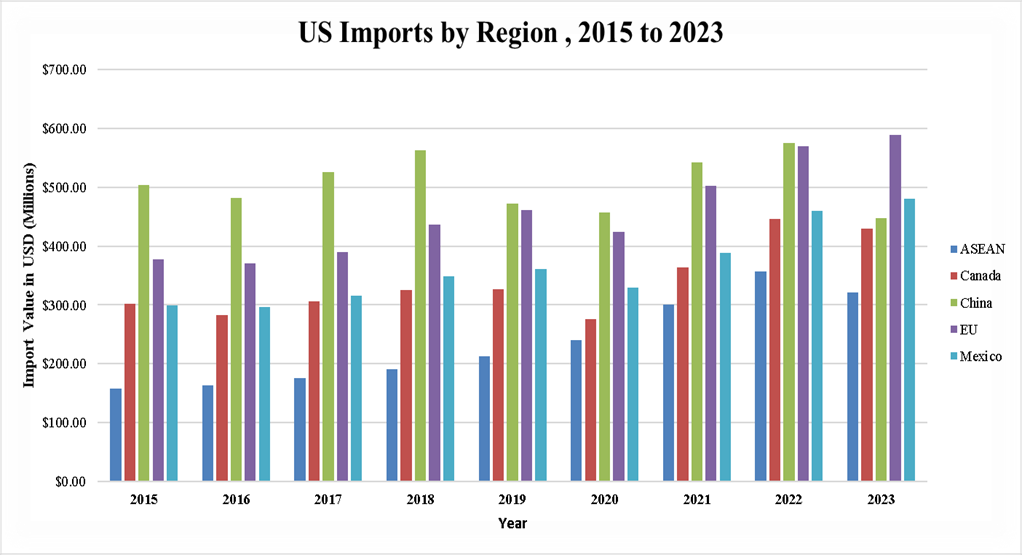

Bar chart showing US imports from major partners (ASEAN, Canada, China, EU, Mexico) from 2015–2023, highlighting shifts in trade volumes and diversification trends.

Key Insights from the US Import Trends by Region (2015–2023)

China’s share of US imports peaked in 2018 at $563 billion but fell to $448 billion by 2023, reflecting efforts to reduce dependence on a single source.

Mexico’s imports rose steadily from $299 billion in 2015 to $480 billion in 2023, highlighting its role as a nearshoring partner.

Canada remains a stable supplier, with imports increasing from $302 billion in 2015 to $430 billion in 2023, peaking at $447 billion in 2022.

ASEAN imports more than doubled, from $157 billion in 2015 to $321 billion in 2023, showing broader Southeast Asian sourcing.

EU imports grew from $378 billion to $589 billion, reflecting continued reliance on advanced machinery, pharmaceuticals, and high-value goods.

Implications: The US is actively diversifying supply sources, reducing reliance on China, strengthening nearshoring in Mexico, and broadening partnerships with ASEAN and EU countries to support supply chain resilience.

The Infrastructure and Technology Enablers

The supply chain transformation depends on modern infrastructure and advanced technology. For companies to rebuild a more resilient system, they have to upgrade the tools and the networks that support it.

Workforce Development: The new supply chain model depends on experts in logistics analysis, robotics, and advanced manufacturing. Investments in such areas help build a workforce that supports long-term growth.

Digital Supply Chains: Companies are deploying AI to forecast demand and spot risks early, IoT sensors to track goods in real time, and cloud platforms to connect every stage of production and transport. This transition increases supply chain transparency and operational agility.

Physical Infrastructure: The Bipartisan Infrastructure Law of 2021 allocates roughly $1.2 trillion between 2022 and 2026 to upgrade roads, rail, ports, and logistics corridors needed to handle increased domestic and regional freight.

Economic and Strategic Implications

The supply chain shift is already shaping the US economy, business decisions, and consumer expectations.

The US Economy With this shift, the growth of high-skilled, high-wage jobs in manufacturing will increase, and there will be reduced dependencies on adversaries for essential goods, strengthening national and economic security. Funding is flowing into regions that are building new factories, technology centers, and logistics hubs, creating momentum for industrial growth across the country.

Businesses The shift brings lower long-term risk but higher upfront costs. Production costs in the US, Mexico, or allied countries are higher, yet they protect businesses from long delays and shutdowns. Businesses must build partnerships with suppliers in Mexico, the US, and allied countries. To stay competitive, they will have to invest in advanced technologies that provide visibility across the chain.

Consumers Some products may cost more because of higher production costs, but with minimal shortages during crises and better availability trade-off. Consumers will have access to goods made in the US, which often come with confidence in quality and labor standards.

Strategic Risks and Critical Implementation Challenges

Systemic Strategic Risks

Geopolitical and Alliance Risks

Friend-shoring assumes long-term political alignment. This is not guaranteed. Leadership changes, trade policy shifts, or regional instability can weaken alliances over time. Overreliance on a narrow group of allied partners can recreate concentration risk under a different label.

Export controls, sanctions, or diplomatic disputes may still disrupt critical inputs such as semiconductors, critical minerals, or energy components.

Economic and Market Risks

Reshoring and nearshoring increase fixed costs. If global demand slows or inflation persists, higher cost structures can compress margins and reduce competitiveness.

Firms that restructure supply chains during economic downturns risk stranded assets if projected demand does not materialize. Currency volatility and interest rate fluctuations also affect cross-border investments in Mexico, Canada, and allied economies.

Execution and Timing Risks

Supply chain transformation is capital-intensive and slow. Semiconductor fabs, battery plants, and logistics hubs take years to reach scale. If execution lags behind geopolitical or market shocks, firms may remain exposed during the transition period. Poor sequencing of investments can lead to capacity bottlenecks, underutilized assets, or missed market windows.

Core Implementation Challenges

Workforce and Talent Pipeline

Advanced manufacturing requires engineers, technicians, data analysts, and automation specialists. The current US labor market does not supply these skills at a sufficient scale. Training pipelines lag capital deployment. Without coordinated investment in technical education, apprenticeships, and immigration pathways for skilled labor, new facilities will face chronic understaffing and lower productivity.

Cost Competitiveness and the Business Case

The U.S. based and allied manufacturing struggles to match Asia on unit cost. Energy prices, labor costs, and regulatory compliance raise production expenses. The business case for reshoring depends on valuing resilience, reliability, and risk reduction. Many firms still lack internal frameworks to quantify these benefits, making investment decisions harder to justify to shareholders focused on short-term returns.

Strategic Recommendations

For Policymakers and US Institutions

Align industrial policy with workforce strategy. Capital subsidies must be matched with funding for technical education, community colleges, and apprenticeship programs tied directly to new manufacturing projects.

Build redundancy into trade policy. Avoid concentrating friend-shoring incentives in a narrow set of countries. Broaden alliances across regions to prevent new single points of failure.

Accelerate permitting and infrastructure delivery. Delays in zoning, environmental reviews, and grid access increase execution risk and discourage private investment.

Standardize resilience metrics. Develop national frameworks for measuring supply chain risk so firms can incorporate resilience into financial decision-making.

For Multinational Corporations

Adopt portfolio based supply chain design. Balance cost-efficient global sourcing with regional redundancy rather than pursuing full reshoring or full globalization.

Invest in digital visibility. Real-time tracking, scenario modeling, and supplier risk analytics are now core operating capabilities, not optional upgrades.

Build long-term supplier partnerships. Stability comes from co-investment, shared data, and joint contingency planning with suppliers in Mexico, the US, and allied economies.

Quantify resilience value. Incorporate downtime risk, revenue loss, and reputational impact into capital allocation models.

For Investors

Reprice resilience. Favor firms with diversified sourcing, regional manufacturing footprints, and strong supply chain governance.

Target infrastructure and enablers. Logistics, grid modernization, industrial real estate, and supply chain software benefit directly from regionalization trends.

Assess execution capability. Capital alone is insufficient. Management teams with proven experience in large-scale industrial projects will outperform.

Take a long-horizon view. Returns from reshoring and friend-shoring accrue over years, not quarters.

Regionalization as the Dominant Supply Chain Model

The US Supply Chain Transformation is shaping a future built on predictable operations and regional networks. The shift away from hyper-global systems is permanent. Businesses are moving toward a structure that balances production across the United States, nearby trade partners, and trusted allies.

The goal is to create a supply chain that supports long-term growth and withstands disruption. Workforce and costs remain challenges, but they do not change the overall path. The priority now is strength and stability, not the lowest possible price. Resilience-centered supply chain design is now a core determinant of long-term US commercial and industrial competitiveness.

Key Takeaways

The US supply chain model is shifting from cost minimization to risk minimization.

Reshoring, nearshoring, and friend-shoring now define industrial strategy.

Government policy is actively reshaping manufacturing geography.

Mexico and allied economies are gaining lasting strategic importance.

Companies that invest early in supply chain visibility and redundancy will outperform.

Supply chain resilience is now a competitive advantage, not a contingency cost.

Frequently Asked Questions: US Supply Chain Transformation

1. What is the US Supply Chain Transformation?

The US Supply Chain Transformation is a shift toward reshoring, nearshoring, and friendshoring to reduce supply chain risk, improve resilience, and protect national and economic security.

2. Why is the US reshoring and nearshoring manufacturing?

The US is reshoring and nearshoring to reduce dependence on China, limit exposure to geopolitical risk, shorten supply lines, and prevent disruptions like those seen during the COVID-19 pandemic.

3.What is friend-shoring in supply chains?

Friend-shoring is the practice of relocating supply chains to politically aligned countries with stable institutions to reduce trade risk and ensure reliable access to critical goods.

4. How does supply chain regionalization affect businesses?

Regionalized supply chains increase resilience and reliability but raise production costs, requiring firms to invest in automation, digital visibility, and diversified supplier networks.

A leading global company for Business Solutions , bringing the intriguing global business arena into your space to a business and financial savvy mind.

social media:

Stay In Touch

Don't hesitate. Reach us with these info.

0795046415financialshub01@gmail.comNairobi/Kenya

We create great content everyday. Subscribe to be the first notified when released.

.jpg)

.png)

.png)

%20(1).png)

%201%20(1).png)