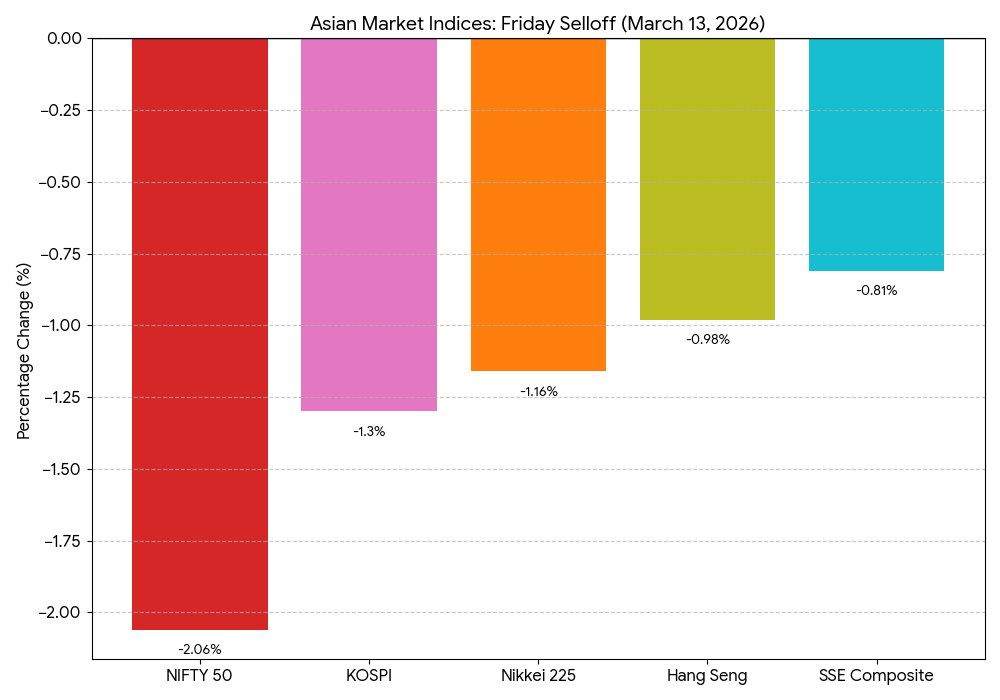

Asian stock markets fell sharply in the week ending March 13, 2026, as escalating tensions in the Middle East triggered a surge in oil prices and renewed fears of persistent global inflation. The regional selloff hit major benchmarks across Japan, India, Hong Kong, China, and South Korea, with energy-importing economies experiencing the heaviest losses.

Rising crude prices, uncertainty surrounding shipping routes in the Strait of Hormuz, and shifting expectations for central bank policy drove investors toward safer assets. As a result, risk sentiment weakened across Asia-Pacific equities.

Asia Market Performance Summary

Most major Asian indices ended the week in negative territory as geopolitical tensions and macroeconomic concerns weighed heavily on investor sentiment.

Japan

Japan’s benchmark Nikkei 225 declined 1.16% on Friday to close at 53,825 points, bringing its weekly loss to 3.24%. This marked the second consecutive week of declines for Japanese equities.

Major decliners included SoftBank Group (-4.3%), Advantest (-3.5%), and Honda Motor (-5.7%). Honda warned of potential annual losses related to electric vehicle restructuring costs and weak demand in China.

India

Indian markets experienced some of the steepest declines in Asia due to the country's heavy dependence on imported crude oil.

The Nifty 50 plunged 2.06% on Friday to 23,151.10, its lowest level in nearly 11 months. Meanwhile, the BSE Sensex dropped 1.93% on the final trading day, losing more than 1,470 points and ending the week down 5.5%.

Hong Kong

Hong Kong’s Hang Seng Index fell 0.98% on Friday to close at 25,465.60 as financial and technology stocks came under pressure.

Mainland China

China’s Shanghai Composite Index slipped 0.81% to end at 4,095.45. Mainland markets showed relative resilience earlier in the week compared to regional peers, though they eventually succumbed to broader risk-off sentiment.

South Korea

South Korea’s KOSPI declined 1.3% to close at 5,509.22 as technology stocks weakened amid rising global bond yields.

Major semiconductor companies including Samsung Electronics (-1.76%) and SK Hynix (-1.08%) weighed on the index following a volatile month for the chip sector.

Asia Market Data Snapshot

Asian stock market decline chart, NIFTY 50 leads losses, KOSPI, Nikkei, Hang Seng, SSE fall.

Key Drivers Behind the Asian Market Selloff

Middle East Conflict and Oil Price Surge

Escalating geopolitical tensions between the United States, Israel, and Iran intensified market volatility. Iran’s newly appointed Supreme Leader, Mojtaba Khamenei, vowed to keep the Strait of Hormuz closed, threatening one of the world’s most critical oil shipping routes.

The disruption could affect nearly 20% of global oil supply, pushing Brent Crude Oil above $100 per barrel despite emergency releases from the International Energy Agency.

Higher energy prices tend to weigh heavily on Asian economies that rely on imported oil, particularly India and Japan.

Inflation Concerns and Interest Rate Expectations

The surge in oil prices reignited fears that global inflation could remain stubbornly high throughout 2026.

Markets subsequently revised expectations for monetary easing from the Federal Reserve. Traders now anticipate only about 20 basis points of interest rate cuts for the remainder of the year, significantly lower than the 50 basis points priced in just a month earlier.

Higher interest rates generally reduce valuations for growth stocks and technology companies.

Currency Movements and Safe-Haven Demand

Risk aversion also drove strong demand for safe-haven assets.

The U.S. Dollar Index climbed above 100 as investors sought stability amid rising geopolitical risk.

Meanwhile, the Japanese yen weakened sharply, with USD/JPY rising above 159 and raising speculation that Japanese authorities could intervene in currency markets.

India’s rupee also came under pressure, falling to a record low of 92.45 against the U.S. dollar.

Sector Performance Across Asian Markets

The week saw sharp divergences across sectors as investors rotated capital toward energy producers and defensive assets.

Sectors Under Pressure

Financials

Banking stocks declined across several markets due to investor concerns about slower economic growth and foreign capital outflows.

Hong Kong financial stocks were particularly volatile after a major insider trading investigation involving multiple financial firms.

Indian banking stocks also weakened as foreign institutional investors withdrew over ₹7,000 crore in a single trading session.

Technology and Semiconductors

Technology shares across Asia declined as rising bond yields reduced the attractiveness of high-growth stocks.

South Korea’s semiconductor sector faced renewed selling pressure amid global uncertainty surrounding demand cycles.

Consumer and Automotive

Automotive stocks were among the hardest hit during the week.

Honda Motor shares dropped more than 6% after the company warned of its first annual loss in nearly seven decades due to costly electric vehicle restructuring efforts.

Higher fuel costs also hurt transportation companies across Southeast Asia, particularly in Indonesia.

Real Estate

Property developers continued to face headwinds from high interest rates, with real estate indices across several Asian markets falling between 2.7% and 3.3%.

Defensive and Outperforming Sectors

Energy

Energy companies were the standout performers during the week as oil prices surged.

China’s largest oil producers — CNOOC, PetroChina, and Sinopec — saw strong gains, with CNOOC rising as much as 10% in Shanghai trading.

In Malaysia, energy-linked firms such as Hibiscus Petroleum surged 18.5%, while Petronas Chemicals climbed 7%.

Basic Materials

Commodity exporters saw selective investor interest as rising global prices supported mining and infrastructure-related firms.

Indonesia’s Bumi Resources attracted foreign buying even as the broader market declined.

Outlook for Asian Stock Markets

Market volatility across Asia is likely to remain elevated in the coming weeks as investors closely monitor geopolitical developments in the Middle East and the trajectory of global oil prices.

If tensions around the Strait of Hormuz persist, sustained high energy prices could place additional pressure on inflation and delay central bank rate cuts.

Energy-importing economies such as India and Japan may remain particularly vulnerable to further oil price shocks, while energy producers and commodity exporters could continue to benefit from the current environment.

Key Takeaways

Escalating Middle East tensions triggered a sharp oil price surge and global market volatility.

Asian stock markets broadly declined, with India experiencing the largest losses.

Rising energy costs revived inflation concerns and reduced expectations for interest rate cuts.

Energy companies outperformed while financials, technology, and automotive stocks lagged.

FAQs

1. Why did Asian stock markets fall this week?

Asian stock markets declined due to escalating tensions in the Middle East that pushed global oil prices above $100 per barrel. The surge in energy costs raised concerns about persistent inflation and reduced expectations for interest rate cuts from the Federal Reserve. Major indices including the Nikkei 225, Nifty 50, and Hang Seng Index all recorded weekly losses as investors moved toward safer assets.

2. How do rising oil prices affect Asian stock markets?

Rising oil prices typically hurt Asian stock markets because many regional economies depend heavily on imported energy. Higher crude prices increase production costs, fuel inflation, and weaken currencies. During the latest market selloff, the surge in Brent Crude Oil particularly impacted energy-importing countries such as India and Japan, leading to significant declines in their equity markets.

3. Which sectors performed best and worst in Asian markets during the selloff?

Energy stocks were the top performers during the week as oil prices surged, benefiting major producers across China and Southeast Asia. In contrast, financials, technology, and automotive stocks faced heavy selling pressure. Semiconductor companies weighed on South Korea’s KOSPI, while banking stocks declined due to foreign investor outflows and concerns about slower economic growth.

The Nairobi Securities Exchange (NSE) 20 Share Index closed the weekend at 3,604.75, edging up by +18.59 points (+0.52%). While the daily gain appears modest, the underlying volume story is anything but. Total shares traded surged to 45.8 million, a 150% improvement from the previous session, pushing daily equity turnover past the KES 1.38 billion mark.

The NSE 20 Share Index, commonly referred to as the Nairobi Stock Exchange 20, is a market capitalization, weighted benchmark that tracks the performance of the 20 leading companies listed on the Nairobi Securities Exchange (NSE). It serves as a vital barometer of the Kenyan stock market’s overall health and is widely relied upon by investors to assess market trends and gauge performance.

The Banking Moat: Stability as a Service

The Banking Sector Index remained the market’s steady hand, gaining 1.63 points. KCB Group led the large-cap charge with a +4.38% climb to close at KES 77.50. This follows a blockbuster February where bank stocks added KES 327 billion in market value. This isn't just price action; it’s a signal of institutional resilience as banks successfully absorb foreign selling through strong domestic demand.

The Speculative Surge vs. Strategic Value

There was a massive 20.21% jump in Eveready East Africa, which led the gainers alongside Kenya Airways (+9.84%). While these "penny-stock" rallies generate high-traffic headlines, Kencrave’s longevity lens focuses elsewhere: Safaricom continues to anchor the market by volume (19.3 million shares), and Equity Group maintains its position as the brand-value leader.

The Dividend Cycle: Cash is King Corporate actions are heating up as we enter the peak dividend season. Notable upcoming books closures include:

British American Tobacco (BAT): Final Dividend of KES 60.00 (Payment: Mar 31, 2026).

Absa Bank Kenya:Final Dividend of KES 1.85 (Payment: Jun 12, 2026).

Safaricom: Interim Dividend of KES 0.85 (Payment: March 31).

Takeaway: The NSE 20 is currently in a "non-directional" texture after the massive wealth creation of February. NSE is currently at the 3,617 level and a breakout above this could signal a new "Bull" phase. For now ignore the speculative noise and follow the Dividend Yield of the stable dividend companies.

Executive Summary: A convergence of Traditional and Digital Health in Asia

Asia is creating a new healthcare model by merging 3,000-year-old traditional medicine (TCM, Ayurveda) with artificial intelligence and digital health. With $5.8B invested in China and $2.64B in India, and 54% of all funding now going to AI-driven solutions, the region is proving that ancient wisdom and modern technology can coexist. Recent successes like a 2025 stroke trial showing herbal formula effectiveness and a Cambodia clinic treating 34,000 patients with 67% follow-up demonstrate real-world potential. The path forward requires hybrid regulations, interoperable health records, cross-trained practitioners, and insurance coverage. Asia isn't just adopting Western digital health, it's redefining healthcare as personalized, preventive, and accessible to all.

Origins of Traditional Chinese Medicine (TCM) and the Foundations of Traditional Asian Medicine

The Chinese people created traditional Chinese medicine (TCM) as a system of medical knowledge. The holistic idea of "harmony between man and nature" defines TCM as a practice that includes visible information; cognitive activity from a point of view of both attributes and relationships; natural resources found inside and outside of one's body; as well as the regulation and balance of one's state of health.

The provision of Traditional Asian Medicine, particularly Traditional Chinese Medicine (TCM), began over 3,000 years ago with shamanistic practices and early therapeutic tools like stone acupuncture needles. By the Western Zhou Dynasty (1046–771 BCE), healthcare had evolved into a remarkably sophisticated, state-funded system documented in the Rites of Zhou, featuring specialized physicians whose performance and compensation were tied to patient outcomes.

The foundational "why" of this era was both practical and driven by the holistic belief in achieving harmony between humanity, nature, and the vital energy of Qi. This theoretical framework was solidified between 200 BCE and 200 CE with the creation of canonical texts like The Yellow Emperor's Inner Classic and Shen Nong's Herbal, which explained illness as an imbalance to be corrected through individualized care, diet, and natural substances.

Throughout subsequent centuries, imperial patronage advanced TCM as a matter of statecraft and cultural prestige, with governments commissioning the world's first pharmacopoeias to standardize knowledge. The tradition was further enriched through cross-cultural exchanges along the Silk Road, integrating ideas from Ayurvedic, Greco-Arabic, and Tibetan medicine.

In the 20th century, TCM faced existential threats from modernization movements but was politically reinvented under Maoist China as a source of national pride and an affordable, scalable healthcare solution for rural populations. Today, the "why" has expanded to include scientific validation through AI in healthcare, biotechnology, economic opportunity, and global digital health leadership.

Case Studies: Integration of Traditional Asian Medicine and Digital Health Systems

Cases where Traditional Chinese (Asian) Medicine was adopted, the effectiveness and failures.

Case 1: National TCM Integration Model of China – Digital Health and AI in Traditional Medicine

More than 85% of hospitals in China are integrating TCM, with standardized education, national treatment guidelines, insurance coverage, and government research infrastructure. TCM is used along with conventional treatments, not as an alternative to them.

Successes:

Show large scale viability of traditional medicine integration into the modern healthcare system.

Providing insurance coverage eliminates financial barriers and ensures equal access for all patients.

Government funding has resulted in standardization of education, practice, and research. Serves as a global reference point for countries looking to integrate traditional medicine.

Failures:

Although China has achieved success domestically, there are no international regulatory harmonization efforts raising questions about compliance with international evidence standards.

Limited ability to export TCM products and practices; limited ability to gain acceptance of TCM in the international marketplace.

The integration of TCM has not resolved the epistemological conflict between the holistic nature of TCM and the reductionist approach of modern Western evidence-based health care.

Case 2: Jianpi Fuzheng Formula RCT – Evidence-Based Validation of Traditional Chinese Medicine

In 2025 double-blind randomized placebo-controlled clinical trials were performed for the Jianpi Fuzheng formula (JPFZF) for ischemic stroke patients over 24 weeks.

Successes:

JPFZF showed lower rates of recurrence of vascular events over time compared to placebo.

Patients treated with JPFZF had significant improvements in cognition (MoCA score) and reduced anxiety and depression (SAS and SDS).

The design of this study followed gold standard RCT methods (double blind randomized, placebo controlled registered study) and did not show any significant differences in safety compared to placebo; indicating that JPFZF has a good safety profile.

Failures:

Lack of multi-center replication.

Case 3: Traditional Medicine and COVID-19 – Global Use of TCM and Ayurveda During the Pandemic

Due to the COVID-19 pandemic, several Southeast Asian countries began using Traditional Medicine in conjunction with conventional medical treatment. Over 78 studies from Traditional Chinese Medicine (TCM), Ayurvedic, Siddha, and Homeopathic were reviewed in a meta-analysis.

Successes:

TCM showed minor improvements in symptom relief and reduced hospitalization.

Ayurvedic products (AYUSH 64, Ashwagandha) reduced viral loading faster in some studies.

Significant acceptance and demand for Traditional Medicine from treated populations.

Governments actively mobilized Traditional Medicine resources to aid the COVID-19 response within China/India.

Failures:

Homeopathic medicine showed no treatment effect greater than placebo with no evidence of efficacy.

Inconsistent safety reporting on TCM among the studies.

There was a lack of data around severity of cases of COVID-19; therefore, treatment decisions cannot be made without more data.

Due to the high degree of methodological heterogeneity between studies, valid conclusions about the comparative effectiveness cannot be drawn.

There was a wide variation in the robustness of the evidence for each system of Traditional Medicine.

Case 4: International TCM Clinic in Cambodia – Cross-Border Digital Health and Traditional Medicine Expansion

In 2022, a Chinese medical team established a TCM clinic at the Cambodia-China Friendship Hospital located in Phnom Penh, Cambodia. The clinic treated approximately 34000 local patients for a year, which included treating patients for COVID-19.

Successes:

Follow-up rate for this international medical mission is very high at 67%.

Several former patients have documented successful outcomes, such as a hearing-impaired patient regaining their hearing and a patient.

Highlights potential for acceptance and desire for cross-cultural utilization of TCM.

Failures:

Evidence is anecdotal and there have been no controlled studies completed.

This international medical mission was dependent on the support of diplomats and other officials from their respective governments. Therefore, without continued political support, there are concerns surrounding their future sustainability. Cultural translation and acceptance requires continued resources to support the initiative.

Case 5: Ayurveda for Hemiplegia - Systematic Review of Traditional Indian Medicine

A systematic review carried out in 2025, assessed the efficacy of Ayurvedic interventions for hemiplegia (Pakshaghata) by analyzing 30 studies. These studies included randomized controlled trials, non-randomized controlled trials, and pre-post tests.

Successes:

Ayurvedic interventions are being provided and researched as treatment options for neurological conditions.

Both practitioners and patients demonstrate significant commitment to their respective cultures and histories surrounding the use of these types of therapies such as Ayurvedic treatment.

Failures:

The studies included in this review could not provide adequate evidence to make definitive conclusions regarding either efficacy or safety due to the insufficient quality of the individual studies.

With much of the worldwide innovation in digital health emerging from Asia, Asia is becoming the leading global hub for digital health innovation through substantial financial investments in real-time clinical informatics, artificial intelligence (AI) based decision support, and cloud-native digital health platforms. This investment will support the future development of the next generation of digital health services (Smart Health Asia).

Investments in Digital Health among top leading Asia Countries (2016 – 2025)

India

India has seen massive amounts of venture capital (VC) and private equity (PE) investment flowing into the Digital Health, totalling to approximately $10.2 billion Tracxn. The largest amount of funding was raised in 2021 (approximately $2.83 billion), after which there has been an overall decline in funding volume. India’s digital health market size grew from $1.07 billion in 2016 to $2.29 billion by 2021, and it is projected to reach a total size of $6.0 billion by end of 2026.

China

China is characterized by the immense scale of its healthtech market. The wearable medical devices market alone was worth $56 billion in 2016, and it grew 20.1% during that year. Furthermore, healthcare information technology (IT) spending in China is expected to be approximately $12.7 billion (RMB 92.1 billion) by end of 2026. The digital health and wellness market will reach approximately $28.6 billion (RMB 198 billion) by the year end, 2026.

Singapore

The value of the digital health market in Singapore was approximately $1.1 billion in 2021. The government has committed to digital health initiatives through the Smart Nation Programme with a commitment of approximately $1.5 billion, including $100 million of that dedicated to funding AI-based diagnostic systems and approximately $4.5 million for innovation grants.

South Korea

South Korea's market for e-health and telemedicine was estimated to be approximately $3.9 billion in 2021. The government has committed an estimated amount of approximately $250 million to promote digital health initiatives such as telemedicine and e-health technologies (Kenresearch).

Japan

Japan pursues targeted investment funds that support multiple aspects of digital health, including AI, remote care, connected devices and health data.

Comparative Analysis: AI Integration, Telehealth Adoption, and Traditional Medicine Digitalization by Country

2025 cumulative digital health investments in Asia

Bar chart of 2025 cumulative digital health investments in Asia, comparing AI-driven solutions versus traditional digital health across China, India, South Korea, Singapore, and Japan. Source: Galen Growth & Rock Health.

Key Insights: 2025 cumulative digital health investments in Asia

China as the market leader: With $5.8B in cumulative investment, China has established itself as the undisputed hub for digital health innovation in Asia. This scale signals strong government backing, robust capital markets, and a mature ecosystem for healthcare technology.

India as a fast-rising challenger: At $2.64B, India is positioning itself as the second-largest player, leveraging its vast population base and growing digital infrastructure to attract significant capital inflows.

Other markets remain niche: South Korea, Singapore, and Japan are investing at sub-$1B levels, indicating smaller but potentially specialized opportunities rather than broad-scale market dominance.

AI as the strategic priority: With 54% of total investment directed toward AI-driven solutions, the region is clearly prioritizing scalable, technology-led healthcare models over traditional digital health approaches.

Asia’s digital health investment growth from 2022 to 2025

Stacked area chart showing Asia’s digital health investment growth from 2022 to 2025, highlighting rapid AI-driven healthcare funding versus traditional portfolios. Source: Galen Growth & Rock Health.

Key Insights: Asia’s digital health investment growth from 2022 to 2025

Consistent upward trend: Digital health investment across Asia has shown year-on-year growth, reflecting sustained confidence in the sector.

AI outpaces traditional portfolios: The accelerated growth of AI-driven investments highlights a structural shift in capital allocation, with investors favoring disruptive technologies that promise efficiency, personalization, and scalability.

Market maturity by 2025: By the end of the period, AI-driven healthcare is projected to dominate the investment landscape, signaling a tipping point where traditional digital health solutions may struggle to attract comparable funding.

Strategic Implication: The market is undergoing a paradigm shift. Stakeholders who fail to integrate AI into their healthcare strategies risk capital flight and competitive obsolescence.

Regional Strategic Outlook

China & India: Command the lion’s share of capital and innovation, shaping the competitive landscape.

AI as the growth engine: AI is no longer optional, it is becoming the default investment area in healthcare.

Smaller markets: Offer specialized innovation opportunities but lack the scale to compete head-to-head with China and India.

Recommendations for Executives & Investors

Prioritize AI integration: Position portfolios and strategies around AI-driven healthcare to align with capital flows.

Focus on China & India: Treat these markets as core investment destinations for scale and growth.

Explore niche plays: Leverage South Korea, Singapore, and Japan for specialized innovation (e.g., precision medicine, biotech partnerships).

Prepare for consolidation: Expect M&A activity as traditional digital health players seek to pivot into AI-driven models.

As delivery models continue to evolve from solely hospital-based models towards more diverse delivery models, including ambulatory care clinics, community-based facilities, and at home, there is a region-wide effort to create more accessible and cost-effective healthcare options.

Digital vs Traditional Medicine across major power countries

Comparative table of global healthcare systems analyzing AI integration, traditional medicine adoption, regulatory speed, telehealth usage, and data governance across China, India, Singapore, Japan, South Korea, USA, UK, and Germany. Source: Galen Growth & Rock Health.

Key Contrasts Between Traditional Asian Medicine (TAM) and Digital Healthcare Systems

Scientific Validation: Digital Health Tech: Requires evidence from randomized controlled trials (RCTs) and biochemical pathways. Traditional Asian Medicine:Strongest evidence is often seen in systems biology and long-term outcomes, which do not align with standard Western validation methodologies.

Standardization vs. Individualization: Digital Health Tech: Advantages in standardization due to the nature of digital health data.

Traditional Asian Medicine: Based on highly individualized care, creating challenges for developing universal "one-size-fits-all" digital solutions.

Regulatory Frameworks: Digital Health Tech: Must comply with extensive medical device and software regulation. Traditional Asian Medicine: Regulatory status depends on product classification (e.g., as a supplement) and practitioner licensing, leading to a complex, non-uniform landscape for herbal products and providers.

Co-Existence of Traditional and Digital Health Care Eco-System

Digital Health Tech complements the traditional health care ecosystem and will assist in the digitization, validation, and scaling of traditional health care ecosystems. The relationship between traditional Asian medicine and new health tech is not one of simple comparison or competition, but increasingly one of fascinating convergence and coexistence.

It's a story of ancient health wisdom meeting digital health innovation. There is an increased shift towards a combination of both traditional and modern-day medicine, resulting in need for explorations for safe adoption in the health sector (World Health Organization & Springer Journal).

How can Traditional Asian Medicine and Health Technology co-exist:

1. Digitalizing Diagnosis & Treatment:

AI-powered analysis of tongue and facial complexion via smartphone cameras.

Pulse waveform quantification using digital sensors.

Tele-traditional medicine platforms for online consultations with licensed TCM and Ayurvedic doctors, including home delivery of herbal prescriptions.

Digital herbal pharmacies (e.g., 1mg in India, Alodokter in Indonesia) offering verified traditional products (Ayurvedic, Jamu) with usage instructions.

2. Modernizing Wellness & Prevention:

Wearables tracking stress (via HRV), sleep, and mindfulness: aligning with the TAM principle of balance.

Mental wellness apps incorporating traditional concepts: Buddhist mindfulness, Yogic breathing (Pranayama), and traditional sound therapy.

3. High-Tech Verification & Manufacturing:

Using biotechnology, genomics, metabolomics, and AI to identify active compounds in herbal medicine, enhancing verification and production.

The Asia-Pacific digital health market has grown rapidly due to a wide range of demographic factors and supportive policy and technology adoption. Below are a few examples of health tech trends in Asia:

Wearable Health Technology: Devices like fitness trackers and smartwatches are popular for monitoring vitals, activity, and motivating personal health management (Pojoksatu).

Telemedicine and Remote Patient Monitoring: Enables access to care from home, significantly improving accessibility in rural and remote areas.

Artificial Intelligence in Healthcare: Improves operational efficiency, diagnostic accuracy via machine learning, and enables personalized treatment plans through data analysis.

Data Security and Privacy: With increased digitization, robust data security practices and regulatory compliance are becoming imperative to protect patient data.

Virtual Reality (VR): Used for advanced medical training and to guide patients through pre- and post-surgery therapeutic exercises.

Policy Recommendations for Adopting Hybrid Medicine (Traditional and Modern medicine)

1. Integrating Regulation and Evidence-Based Research

Develop a new hybrid classification structure for traditional medicine (rather than simply drug or supplement) based on existing regulatory systems such as Indonesia's 3-tiered system (Jamu, OHT and Fitofarmaka).

Integrate traditional medicine historical evidence to include both long-term treatment outcomes and biology systems to provide random controlled trial support for any indications.

Establish a joint regulatory body/task force to provide oversight and governance for the collaborative integration of traditional medicine and modern/conventional medicine.

2. Research Infrastructure and Fund Hybrid Evidence-Based Research

Establish dedicated hybrid research centers that will consist of the collaborative efforts of traditional and modern health care practitioners; establish inclusion of traditional medicine in national health research plans/programs.

Develop hybrid outcome measures that consider holistic (or potential) improvements in balance, energy and overall well-being in addition to biochemical outcomes.

3. Create Digital Infrastructure and Develop Interoperable Systems

Establish electronic medical records that will consist of data fields to allow for the inclusion of traditional medicine data (such as tongue and pulse data). Tongue and pulse will then correlate with ICD codes so that traditional data is readily available when physicians utilize electronic medical records in their decision-making process.

Implement AI Applications to support clinician decision making based on hybridized data.

Establish secure tele-traditional medicine programs that can be offered by traditional medicine practitioners.

Utilize Blockchain technology to track and verify the authenticity of herbal products.

4. Dual Competency Workforce Education

Require all health care professionals to receive cross-training in both traditional and modern health care systems.

Develop hybrid medicine specialization certifications that are recognized by both the medical board and traditional boards of registrars (governing bodies).

Provide continuing education in evidence-based practice in traditional medicine to physicians trained at Western Medical schools.

Develop and implement exchange programs/fellowships between traditional medicine practitioners and allopathic practitioners.

5. Financing: Create Equitable Access

Expand insurance coverage to include evidence-based hybrid programs (prevention, chronic disease management, wellness).

Develop innovation funding for hybrid medicine startups to address regulatory uncertainties.

Establish value-based reimbursement for preventative hybrid care and where traditional medicine excels.

Include hybrid care metrics in hospital accreditation & quality incentives.

Bottom Line:

While Asia will not simply take and use Western health technology, it will redefine how we use it. The way of the future relates to creating an integrated model that combines cutting-edge technology (deep-tech) with age-old wisdom about health (deep tradition), via scalable, mobile-first digital platforms. Health will be transformational (preventive, and personalized) through active involvement of patients in their own care. Asia will become the world’s model for using technology to enable everyone’s access to holistic, human-centric health care.

Key Takeaways: The Convergence Redefining Traditional Asian Medicine and Global Digital Health

1.Asia Is Pioneering Hybrid Medicine

Asia is integrating Traditional Asian Medicine (TCM, Ayurveda, Jamu) with AI, digital health, and telemedicine, creating a new hybrid healthcare model.

2. Digital Health Enhances Traditional Medicine

AI diagnostics, wearable devices, and digital platforms are improving the validation, scalability, and safety of traditional medicine without replacing its holistic principles.

3. AI Is Bridging Holistic and Evidence-Based Care

Artificial intelligence enables standardized analysis of tongue, pulse, and herbal data, helping align traditional medicine with modern clinical research standards.

4. Asia Is a Global Digital Health Investment Leader

China, India, Singapore, Japan, and South Korea are investing heavily in health tech, AI diagnostics, and digital therapeutics, positioning the region at the forefront of healthcare innovation.

5. Regulation and Infrastructure Will Determine Long-Term Success Clear regulatory frameworks, interoperable health records, AI governance, and insurance coverage are essential to scaling hybrid medicine globally.

Frequently Asked Questions

1. What is hybrid medicine in Asia?

Hybrid medicine combines Traditional Asian Medicine (TCM, Ayurveda, Jamu) with digital health technologies such as AI, telemedicine, and wearable devices to create scalable, preventive, and personalized healthcare systems.

2.How is AI validating traditional medicine?

AI analyzes tongue diagnosis, pulse patterns, herbal compounds, and patient outcomes to standardize traditional practices and align them with evidence-based healthcare models.

3.What are the main challenges to integrating traditional and modern medicine?

Key challenges include regulatory fragmentation, differences in evidence standards, limited digital health record integration, and inconsistent clinical research quality.

4.Which Asian countries are leading in digital health and traditional medicine integration?

China and India lead in large-scale integration and investment, while Singapore, Japan, and South Korea advance AI, telehealth, and regulatory innovation.

5.What policies support the growth of hybrid medicine?

Successful integration requires clear regulatory pathways, hybrid research funding, interoperable electronic health records, workforce cross-training, and insurance coverage for evidence-based traditional care.

Executive Summary: Rwanda’s Horizon 1000 Initiative, AI Transforming Primary Healthcare

Rwanda’s Horizon 1000 Initiative (2026), funded by the Gates Foundation and OpenAI, deploys AI-powered clinical decision-support tools in primary care clinics, starting with 50 sites and scaling to 1,000 clinics across Africa by 2028. Facing a severe healthcare workforce shortage and high malaria burden (70% of CHW cases), Rwanda uses AI to guide patient intake, flag risks, suggest care steps, and reduce administrative workload, while keeping human clinicians in control.

The system combine, large language models with structured medical rules, aligns with national standards, and safeguards data privacy and health sovereignty.

Evidence shows AI can cut diagnostic errors by 12–30%, boosting efficiency and care quality. Rwanda’s strong digital infrastructure, political commitment, and localized, low-connectivity design make Horizon 1000 a model for ethical, scalable AI in African healthcare.

The First Phase Of The Horizon 1000 Healthcare Initiative

Rwanda is piloting artificial intelligence-powered technology in public health clinics as part of a new initiative aimed at strengthening primary healthcare, starting with more than 50 clinics this year.

The Gates Foundation and OpenAI on January 21st 2026 launched a new initiative dubbed Horizons1000, with joint funding of $50 million over two years.

This is the first step of a broader, continent-wide plan to bring AI tools to around 1,000 primary healthcare clinics across Africa by 2028. The Horizon 1000 initiative is set to begin in Rwanda, and expand further in Africa to Nigeria, South Africa and Kenya.

Why Horizon 1000 Matters For Rwanda’s Healthcare System

Rwanda now has one health care worker for 1000 patients this is far below workforce density levels associated with countries approaching universal health coverage (WHO, 2022).

Bar graph comparing Rwanda's physician-to-population ratio (1:1000) against the WHO recommended standard (4:1000), highlighting a 75% deficit in healthcare human resources.

Key insight:

There is a 75% shortage of healthcare human resource. This puts a strain on healthcare services.

Rwanda’s Healthcare Workforce Gap And Why Ai Is Being Deployed Now

Rwanda is already exploring the use of AI to help health workers with disease diagnosis, relieve them of tedious administrative tasks, and model the trajectory of diseases.

As a start, the country has rolled out internet access to around 97% of its population , a significant achievement in a country where most people live in rural areas.

It is currently building some of the foundational digital infrastructure that is enabling and powering the technological advancements.

One of Rwanda’s aims is to use AI to create decision-support tools for its 60,000-plus community health workers who provide primary healthcare to communities across the country.

The country wants an AI tool to help them in the diagnosis of malaria.

It aims to make much accurate diagnosis and to predict when and where to expect malaria cases. Malaria accounts for approximately 70% of the cases community health workers deal with yearly in Rwanda.

Pie chart showing Rwanda's disease burden: 70% Malaria cases versus 30% other medical cases, highlighting why malaria is the strategic priority for Rwanda's Vision in healthcare goals.

Why Rwanda Was Selected As The Pilot Country For Ai-Driven Primary Care

Rwanda was chosen as the pilot country because of:

Strong digital health leadership.

The country has been building digital systems (like national health information platforms and community health worker support tools) for years.

Readiness to scale innovation.

Officials see Rwanda as an ideal testing ground for ethical and practical AI integration before expanding to other African health systems.

Political commitment.

Senior health leaders in Rwanda emphasize using AI in ways that support clinicians and improve care quality across local communities.

Inside The "Ai Co-Pilot": How It Actually Works

The system is best understood as a clinical decision-support assistant built on:

1.Large Language Models (LLMs)- The model does pattern recognition and reasoning over text, not diagnosis in the legal sense. It is fine tuned on medical guidelines.( WHO protocols, Rwanda MoH standards) and restricted in scope (primary care, triage, maternal/child health, common infections).

2.Structured clinical rules layered on top-the AI is constrained by rule-based medical logic

Inputs:

Patient symptoms (entered by nurse / community health worker).

Vitals (temperature, BP, weight, etc.).

Basic patient context (age, pregnancy status).

Past visit summaries (if available).

It does not:

Train itself on new patient data.

Store raw identifiable patient data long-term.

Replace national health records.

From Patient Arrival To Clinical Decision: How Ai Is Integrated Into Daily Care

Flowchart diagram Illustrating the step-by-step clinical workflow from patient arrival to final diagnosis in Rwanda's Horizon 1000 AI-assisted primary healthcare clinics.

Step 1: Patient arrives- A nurse or community health worker opens the clinic system (tablet / desktop).

Step 2: Guided intake

The AI:

Prompts structured questions.

Flags missing critical info.

Adjusts questions based on answers (e.g. pregnancy → maternal pathway).

This reduces human error and inconsistency.

Step 3: AI reasoning

The system:

Converts inputs into structured tokens.

Runs them through:

Clinical rules engine.

Language model for reasoning and explanation.

Produces:

Risk level.

Suggested next steps.

Red-flag warnings.

The AI suggests, it does not decide.

Step 4: Human confirmation

The clinician accepts, rejects or modifies the AI’s suggestion. This human-in-the-loop setup is legally and ethically essential.

Data Governance, Privacy, And Health Sovereignty In Rwanda’s Ai Clinics

Rwanda’s Ministry of Health controls:

Data access.

Deployment scope.

OpenAI does not own the health data and the models are used as tools, not autonomous agents.

This matters a lot for sovereignty.

What The Ai System Cannot Do Safely

The model has less accuracy for:

Rare diseases.

Complex multi-condition cases.

Cultural nuance in symptom reporting.

Situations with poor or missing data.

That’s why it’s limited to primary care support, not hospitals or specialists yet.

Key Benefits Of Ai-Assisted Primary Healthcare In Rwanda

This initiative aims at being the transformative opportunity that will:

Improve citizens’ access to health care. AI can help stretch limited human resources more effectively especially in areas with severe staffing shortages.

Reduce administrative burden . Systems can help cut down paperwork and free up time so clinicians can spend more time with patients.

Assist in the realization of accurate and timely decisions by health care professions. AI can assist frontline nurses and community health workers in triaging patients, suggesting care guidance and flagging warning signs that may need urgent attention.

Technical, Linguistic, And System Integration Challenges

1. Digital experts are worried about AI technology using the English language, which is not widely spoken in Rwanda.

Efforts are underway to develop AI technologies in Kinyarwanda, the language spoken by about 75% of Rwanda’s population.

2. Integration with existing systems Making sure that AI tools work smoothly with existing Rwanda health infrastructure and workflows is essential for long-term success.

Lessons From Ai Trials And Deployments

AI in clinical support isn’t entirely new There have been Research trials with live clinicians. In Nairobi, an AI tool called AI Consult was tested in 15 primary care clinics and results showed reduction in medical errors in routine primary care by supporting clinicians without replacing them. (The star)

It offered real-time alerts and guidance to clinicians and was associated with:

Est. 16 % fewer diagnostic errors,

Est. 13 % fewer treatment errors,

Est. Reductions in omissions during patient history taking.

AI’s impact on diagnostic accuracy across selected health systems in Rwanda, Kenya, India, China, United Kingdom and United States.

Error bars represent observed or reported ranges in diagnostic error reduction following AI decision-support deployment. Kenya reflects real-world primary care trial data, while Rwanda represents a projected national target under Horizon 1000 (science direct).

Key insights: AI’s impact on diagnostic accuracy across selected health systems

Across global healthcare systems, AI decision support tools consistently reduce diagnostic errors by approximately 12–30%, depending on clinical setting and use case.

The strongest gains are observed in high-volume environments where clinicians face heavy workloads and time pressure.

United States: est. 18–25% reduction in diagnostic errors in radiology and primary care decision support systems.

United Kingdom: est. 15–20% reduction in missed or delayed diagnoses using NHS AI triage and imaging tools.

China: est. 20–30% improvement in diagnostic accuracy in AI-assisted imaging and clinical decision systems.

India: est. 12–18% reduction in diagnostic errors in AI-supported primary care and telemedicine platforms.

Kenya (Nairobi trials): est. 15.8% reduction in diagnostic errors in AI-assisted primary care clinics.

Rwanda is estimated to reduce errors by 16%.

Bar graph showing AI decision support reduced diagnostic errors by 15.8% and treatment errors by 12.9% in Nairobi primary care clinics,

The AI decision support proves its value for initiatives like Rwanda's Horizon 1000. (O'Brien et al., 2024).

Key insights: Reduction in error after AI Trials in Nairobi

A 15.8% reduction in diagnostic errors directly translates to fewer missed or incorrect diagnoses, a leading cause of preventable harm in primary care, especially in high-volume, low-resource clinics.

The 12.9% reduction in treatment errors (incorrect medications or dosages) shows AI's utility beyond diagnosis, improving the entire care pathway and enhancing patient safety.

Real clinic deployments tested for safety and impact. The PErioperative AI CHatbot (PEACH) system was embedded in real perioperative clinical workflows and evaluated for accuracy and safety with actual clinicians.

Historical AI decision tools used in clinical practice. The HIV Treatment Response Prediction System (HIV-TRePS) was an AI-based system used from around 2010 by clinicians worldwide, enabling them to predict how individual patients would respond to combinations of HIV drugs based on very large treatment datasets. It was widely used in clinical practice to tailor therapies.

Rwanda’s current program(Horizon 1000) is one of the most ambitious attempts yet to scale AI assistance across a national primary care network in low-resource settings with a structured integration into the public health system.

What Comes Next: Scaling Ai In Rwanda Without Sacrificing Safety Or Trust

1. Plan early for financial sustainability.

Gradually integrate AI costs into:

National health budgets.

Insurance and reimbursement frameworks. Donor funding should support transition, not create dependency.

2. Scale cautiously and evidence-first.

Expand only after:

Demonstrated outcome improvements.

Stable clinician adoption.

Clear governance structures.

Rwanda’s strength lies in credibility and discipline, not rapid expansion.

Policy And Implementation Recommendations For Rwanda’s Ai Health Strategy

1. Keep AI as clinical support and not decision-maker. AI should remain advisory, with all final decisions made by trained health workers. This preserves patient safety, legal clarity, and clinician trust.

2. Prioritize consistency and early risk detection. The goal is reliable care at scale, not superhuman performance.

3. Invest deeply in Kinyarwanda and local context. Ensure Kinyarwanda-first interfaces,locally validated symptom descriptions and alignment with Rwanda’s disease patterns and care pathways. Localization is essential for accuracy and adoption.

4. Design for low-connectivity environments. AI tools must work offline with delayed syncing and never block care due to technical issues.

5. Establish frequent AI health oversight. Create a dedicated unit to monitor AI performance, review errors and adverse events, update clinical rules and models and audit bias and system drift.

Key Takeaways

Rwanda Is Leading AI-Driven Primary Healthcare in Africa.The Horizon 1000 Initiative positions Rwanda as a continental model for safely scaling AI clinical decision-support in public healthcare.

AI Supports Clinicians Without Replacing Human Judgment The system operates as decision support only, reinforcing human-in-the-loop care for nurses and community health workers.

Malaria Is the Highest-Impact AI Use Case Targeting malaria about 70% of CHW caseloads, maximizes gains in diagnostic accuracy and early risk detection.

Data Sovereignty and Governance Are Core to the Strategy Rwanda’s Ministry of Health retains full control over data, deployment, and oversight, ensuring ethical AI use.

Evidence-Based Scaling Drives Long-Term Success With AI reducing diagnostic errors by up to 30% globally, Rwanda’s cautious, outcomes-first approach prioritizes safety and trust.

Frequently Asked Questions (FAQs)

1, What is Rwanda’s Horizon 1000 Initiative?

Horizon 1000 is Rwanda’s national AI healthcare program deploying clinical decision-support tools in primary care clinics to improve diagnosis, triage, and care delivery, with plans to scale across Africa.

2. How is AI used in Rwanda’s primary healthcare system?

AI supports patient intake, risk detection, diagnosis guidance, and administrative efficiency for nurses and community health workers, while all final decisions remain human-led.

3. Does AI replace doctors or community health workers?

No. The system is strictly advisory. AI supports clinicians but does not replace human judgment or medical responsibility.

4. How does Rwanda ensure patient data privacy and sovereignty?

Rwanda’s Ministry of Health controls all data governance, access, and deployment, ensuring patient privacy and national health data sovereignty.

5. Why is malaria the primary AI use case?

Malaria accounts for roughly 70% of community health worker cases in Rwanda, making it the highest-impact area for improving diagnostic accuracy and early intervention through AI.

IShowSpeed's African Tour and the New Era of Influencer Diplomacy

Darren Jason Watkins Jr., better known as “IShowSpeed”, is an American YouTuber and livestreaming sensation. His high-energy, unpredictable content blends gaming, IRL (In Real Life) travel, reactions, and cultural exploration. His popularity surged in the early 2020s, fueled by the pandemic-driven rise of platforms like Twitch.

IShowSpeed embarked on a landmark 28-day tour across twenty African nations titled "Speed Does Africa," spanning late 2025 to early 2026. He live-streamed the majority of his travels to a global audience, achieving remarkable results:

● Subscriber Growth: His channel gained hundreds of thousands of new subscribers.

● Live Engagement: Broadcasts consistently attracted over 200,000 concurrent viewers.

● Cumulative Reach: Individual streams from each country garnered millions of views.

Viral Metrics Breakdown: Record-Breaking Viewership and Global Impressions

According to an audience measurement report from Ipsos referenced by multiple media outlets, the Kenya stop of IShowSpeed’s tour generated an estimated 93.1 billion potential online impressions, making it the most digitally engaged segment of the 20-country ‘Speed Does Africa’ tour. The report also cites peak livestream viewership in the millions and substantial subscriber growth during the visit (Capital fm).

This phenomenal reach highlighted the continent's digital creativity and global appeal. However, it also revealed critical gaps in coordination, infrastructure readiness, and the systematic conversion of viral visibility into long-term economic value.

Case Study: Kenya's 93.1 Billion Impressions and Shattering Stereotypes

The impact in Kenya extended far beyond tourism marketing, fostering a significant cultural shift:

Authentic Visibility: Kenyan cities, especially Nairobi, went viral through the unfiltered lens of everyday life, local culture, and vibrant street scenes.

Challenging Narratives: Analysts note that the visit positively impacted stereotypes about Kenya and Africa. IShowSpeed’s content made the positive, dynamic daily lives of Kenyan citizens highly visible to a global audience of millions.

Ishowspeed during a livestream session in Kenya. Photo Credits: Mpasho

Cultural Aspect and Digital Participation of Ethiopia

Digital Audience and Viewership: For one of the least marketable areas, Ethiopia’s livestreams secured a top 5 ranking among the most engaging stops on the tour based on total viewership share.

Featured Content: Ethiopian culture and local commerce in Addis Ababa were central highlights, providing an authentic, unfiltered view:

Deep Cultural Traditions: Showcasing traditional dress and the coffee ceremony in its birthplace. Historical Landmarks: Featuring sites like the Victory Memorial and Adwa. Local Interactions: Offering a personal, ground-level perspective of daily life and experiences in Ethiopia.

Economic Potential for Business and Travel:

Travel: Promoting Ethiopia's heritage, cuisine, and urban life is generating significant interest and curiosity among Speed's global, young audience, a demographic often unreachable through traditional tourism campaigns.

Business: The surge in online interest is likely to drive tourist searches for Ethiopian experiences, creating direct demand for; Local guides and tour operators, featured restaurants and culinary tours, Cultural venues and event spaces.

Bottom Line: Despite not matching the raw impression numbers of Kenya or Morocco, Ethiopia received tremendous, authentic cultural exposure reaching millions. This has successfully elevated Ethiopian culture onto the global stage for discussion and discovery.

South Africa - Extended Stay and Versatile Exponential Exhibitions

Streaming Engagement: South Africa's livestreams demonstrated strong performance, attracting well over 5 million viewers.

Travel Experiences and Tourism Highlights: Speed showcased the country's diverse and high-adrenaline tourism offerings, featuring exotic Animal Interactions including cage diving and a race with a cheetah.

Ishowspeed taking a photo with a cheeter in South Africa after racing the cheetar.

The "Speed Effect": Converting Viral Visibility into Long-Term Economic Value

The " Speed Effect" refers to the potential for this viral visibility to translate into tangible economic benefits. For Kenya, this presents a high-value promotional opportunity:

Earned Media Value: The tour provided international promotional opportunities worth millions without paid media.

Sectoral Benefits: Key local industries are poised to gain from increased global interest

Hospitality (hotels, lodges).

Transportation (tours, travel services).

Cultural Events (festivals, experiences).

The Challenge: The key will be channeling the surge in interest into sustained booking activity and investment.

Diplomatic Coup: Ghana's Citizenship Grant and Global Media Strategy

Ghana executed a masterstroke in influencer diplomacy, generating a second wave of global media coverage:

Strategic Honor: At the tour's conclusion, Ghana granted IShowSpeed honorary citizenship as appreciation for promoting the country to millions worldwide.

Cultural Showcase: His content from Accra served as a dynamic primer on Ghanaian culture, food, music, traditions, and heritage sites.

Destination Branding: This strategy powerfully positioned Ghana as a modern, culturally rich destination for Gen Z travelers.

Amplified Impact: The citizenship grant itself became a global news story, multiplying media coverage and solidifying a lasting association between the influencer and the nation.

Infrastructure Gaps: Challenges in Sustaining Viral Momentum

The tour's success illuminated critical areas requiring development to harness future opportunities fully:

Coordination: Lack of structured collaboration between influencers, tourism boards, and local businesses.

Infrastructure Readiness: Challenges in hospitality capacity, digital connectivity, and visitor services to meet sudden, large-scale interest.

Conversion Strategy: The absence of systematic mechanisms to transform views and impressions into long-term tourism, investment, and brand equity.

Redefining National Promotion in the Digital Age

IShowSpeed's "Speed Does Africa" tour represents a paradigm shift in destination marketing and cultural diplomacy: It proved the unparalleled reach of authentic, influencer-led content in engaging a global youth audience.

Kenya demonstrated the immense viral potential and stereotype-shattering power of such visits.

Ethiopia and South Africa highlighted how authentic cultural and adventure showcasing can captivate millions and redefine a destination's appeal.

Ghana showcased a savvy diplomatic and PR strategy to amplify and institutionalize the benefits.

The overarching lesson is clear: The future of national promotion lies in strategic partnerships with digital creators, coupled with investments in infrastructure and strategic planning to convert viral moments into enduring economic and cultural capital.

Strategies to Maximize the "Speed Effect"

For National Governments and Tourism Boards

1. Implement an "Influencer Diplomacy" Procedure

Create a formalized rapid-response team responsible for identifying, vetting, and partnering with high-profile digital artists from all over the world.

The unit will streamline the visa process, coordinate secure transportation, and facilitate highly impactful introductions to local culture, thus increasing the likelihood of gaining positive exposure.

2. Establish a "Digital Surge" Conversion Framework

Build a seamless online-to-offline funnel by creating dedicated online landing pages (e.g., "Visit Like Speed").

Use these landing pages to showcase curated itineraries based on the influencer's journey, providing visitors with a clear sample of what to expect.

Pair this with real-time social media analytics to track short-term spikes in online searches and deploy targeted digital advertising campaigns for tourism and investment.

3. Establish a "Viral Infrastructure" Fund

Invest in core infrastructure needed to support a sudden surge in interest. Key areas include: Public Wi-Fi networks in major tourist zones and improvements to national electronic payment systems for visitor convenience.

Provide funding and capacity-building assistance to SMBs in the hospitality sector to: Improve their online booking capabilities and develop a stronger digital marketing presence.

4. Make "Cultural Ambassador" Programs an Ongoing Process

Formalize the process of granting honorary titles (e.g., Tourism Ambassador) with clear, mutually beneficial terms and conditions.

This structure transforms one-time viral experiences into long-lasting branding and partnership opportunities, ensuring sustained advocacy.

5. Develop a "Metrics-to-Mandate" Reporting Program

Mandate that tourism ministries and agencies provide regular reports analyzing the value and impact of influencer-driven promotion.

Reports should quantify earned media value, digital sentiment, and engagement metrics alongside traditional tourism statistics to justify and guide future strategy and investment.

For Municipal Governments & Local Business Associations 1. Create "Creator-Ready" District Partnerships

Identify and curate specific neighborhoods or markets that are authentic, visually engaging, and logistically prepared for influencer visits.

Develop packages for local businesses (e.g., a "Speed Trail" of featured restaurants/shops) with agreed-upon protocols for filming and promotions. 2. Host "Digital Hospitality" Training Workshops

Train local business owners, taxi drivers, and market vendors on the economic value of digital creators.

Focus training on positive engagement, consent for filming, and sharing their own social handles to capture downstream interest.

3. Build a "Rapid Reaction" Local Network

Form a quick-communication network (e.g., WhatsApp group) between the city, police, tourism officers, and key venues.The goal is to safely manage and leverage unexpected influencer visits, turning potential chaos into organized opportunity. 4. Develop Micro-Conversion Tools for SMEs

Provide templates for small businesses: QR code menus linking to the specific moment they were featured.

Create "as seen by Speed" digital badges for their websites and simple social media content packs to re-share and capitalize on the spotlight.

5. Invest in "Viral Clean-Up" and Beautification Prioritize basic municipal services: cleanliness, clear signage, public safety in areas with high viral potential.

The unfiltered nature of IRL streaming means everyday backdrops become global brand assets overnight.

For the Private Sector

Tour Operators & Hotels:

1. Design "Influencer Itinerary" Packages

Create bookable tour packages that explicitly recreate the most engaging segments of the influencer's visit.

Market these directly to the creator's fanbase demographic via targeted social media ads.

2. Implement "Viral Moment" Booking Systems

Create flexible booking and cancellation policies for surge periods.

Develop dynamic pricing models that respond in real-time to spikes in search volume and social mentions for your destination or specific experience.

Develop partnership tools like "Creator Collab" filters that allow businesses to tag themselves in viral travel videos, linking directly to booking pages.

Provide analytics dashboards that show businesses their traffic sourced from specific influencer content.

2. Brands (Local & International)

Move beyond simple sponsorship to authentic integration. Fund "challenge grants" for creators to engage in specific cultural or adventure activities.

Be ready with agile social media marketing budgets to co-brand and amplify content that features your product or service organically. 3. Cross-Sector "Conversion Taskforce"

Form a joint private-sector alliance (transport, hospitality, attractions, retail) to share data on post-viral interest spikes.

Create seamless, cross-promotional offers (e.g., a bundled "Viral Explorer Pass") to increase tourist spend and length of stay.

Key Takeaways

Influencer diplomacy is transforming tourism and nation branding at global scale.

Kenya’s 93.1B potential impressions prove viral creator content can outperform traditional marketing.

Authentic livestreaming reshapes global perceptions and reaches Gen Z audiences directly.

Viral visibility only delivers economic value when paired with conversion-ready infrastructure.

Strategic creator partnerships are now essential for modern digital diplomacy and growth.

FAQs

1. What is influencer diplomacy and why does it matter?

Influencer diplomacy uses digital creators to shape national image, tourism demand, and cultural perception at global scale, especially among Gen Z audiences.

2. What does the 93.1 billion impressions figure represent?

It refers to estimated potential digital impressions, including livestreams, clips, reposts, reactions, and media coverage not unique viewers.

3. How did IShowSpeed’s Africa tour impact tourism branding?

The tour delivered massive earned media exposure, challenged stereotypes, and showcased African cities and cultures through authentic, real-time content.

4. Can viral influencer exposure generate real economic value?

Yes but only when paired with conversion strategies like booking infrastructure, analytics, and coordinated public–private action.

5. What lessons can governments and tourism boards take from this tour?

Successful nation branding now requires structured creator partnerships, rapid-response coordination, and investment in digital and tourism infrastructure.

Executive Summary: Australia Financial Markets Outlook 2026

Australia’s financial markets in 2026 are operating in a late-cycle expansion, characterised by moderate growth, persistent inflation, and a cautious Reserve Bank of Australia (RBA) policy stance. While the Australian economy has shown resilience relative to global peers, restrictive financial conditions, elevated household debt, and tightening domestic liquidity are limiting acceleration.

This report provides an Australia financial markets outlook for 2026, examining business cycle positioning, GDP growth forecasts, labour market dynamics, RBA monetary policy, fiscal policy settings, liquidity conditions, geopolitical risks, and sector-level investment strategy.

Summary table of Australia’s 2026 macroeconomic indicators including cash rate, inflation, GDP growth, and unemployment trends with strategic impacts. Source: RBA/ABS.

Australia Business Cycle Analysis: Late-Cycle Economic Resilience

Late-Cycle Expansion: A late-cycle expansion occurs when economic growth remains positive but slows toward trend. Inflation pressures persist, labor markets stay firm, and monetary policy becomes restrictive. Asset prices become more sensitive to shocks as policy support fades.

Australia has avoided the “per capita recession” traps of 2024–2025 and has transitioned into a broad-based recovery. Growth, however, remains modest rather than explosive. The economy has clearly moved past early-cycle acceleration and into a mature expansion phase.

Current Business Cycle Phase: Late-Stage Expansion

Key Economic Indicators for Australia Outlook 2026

1. GDP Growth Outlook

Projected real GDP growth of approximately 2.1% in 2026 by IMF reflects moderate, trend-aligned expansion rather than overheating (Commbank, 2026). Independent data corroborate this outlook, pointing to steady but restrained growth consistent with long-run potential.

The composition of growth is evolving. Momentum is increasingly investment-led, driven by private capital inflows into:

Data centres.

Renewable energy.

Digital infrastructure.

This shift signals improving capital deepening, productivity potential, and structural resilience within the economy. While headline growth remains modest, its quality has improved. The expansion is increasingly anchored in long-term asset formation, technological capacity, and energy transition dynamics rather than cyclical excess or demand-side overheating.

2. Labour Market Conditions in Australia

Unemployment remains low and stable at around 4.1%as of January 2026, signalling a labour market that is broadly tight and not exhibiting clear signs of overheating. At the same time, underutilisation has risen (Australian Bureau of Statistics, 2026).

This points to emerging hidden labour slack. Spare capacity persists through reduced hours, involuntary part-time employment, and weaker labour demand in certain sectors. Labour market conditions are therefore less uniformly tight than headline unemployment suggests.

This allows continued employment absorption without immediate inflationary pressure, even as headline indicators remain resilient.

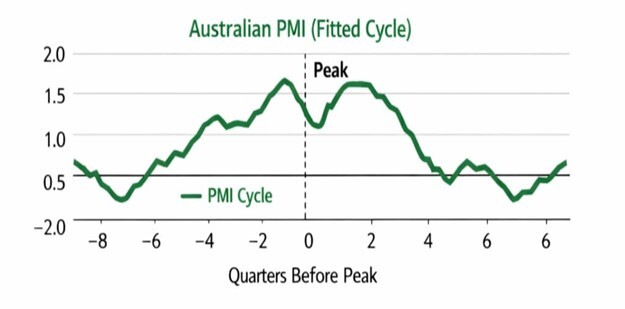

3. PMI Trends and Manufacturing Activity

The Manufacturing Purchasing Managers’ Index (PMI) registered 51.6 in January 2026, indicating modest expansion in manufacturing activity. Growth is supported by an increase in new orders.

However, overall momentum remains muted. Elevated input costs and a slow export environment continue to weigh on profitability and production confidence. The data suggest cautious expansion rather than robust acceleration.

PMI (Purchasing Managers’ Index): A diffusion index measuring manufacturing and services activity. Readings above 50 (0.5) indicate expansion, while readings below 50 signal contraction.

In a mid-to-late expansion phase, PMI readings typically remain above 50 (0.5) but trend downward toward the neutral line. This signals slowing momentum as the economic cycle matures.

Australian PMI fitted cycle chart showing business activity trends before and after peak, highlighting economic growth and contraction phases.

4. Leading Economic Indicators (LEI)

Leading indicators point to continued but moderate economic momentum heading into 2026. The Conference Board’s Leading Economic Index (LEI) for Australia recorded a modest increase in November 2025.

This suggests the economy is still expanding and retaining forward growth traction rather than rolling over into contraction. However, the improvement lacks the strength typically associated with late-cycle acceleration.

Similarly, the Westpac–Melbourne Institute Leading Index continues to print positive yet subdued readings. Together, these indicators imply an economy operating close to its trend path. Growth momentum is intact, downside risks appear contained, and conditions do not point to either imminent slowdown or overheating.

Australia’s Mature Expansion Phase: Growth Without Acceleration

Australia has transitioned into a mature expansionary phase, moving past the high-velocity growth typical of early recovery. Economic activity remains positive, supported by expanding manufacturing output and steady leading indicators.

The pace of growth, however, has plateaued. Businesses continue to invest and labour markets remain firm, but fresh acceleration is absent. This confirms a mid-to-late cycle environment.

In this stage, momentum is sustained but increasingly susceptible to headwinds. Rising costs, softening global demand, and monetary tightening pose growing risks. While the expansion may persist, its resilience to external shocks is gradually diminishing.

Monetary and Fiscal Policy Outlook: RBA Strategy and Government Support

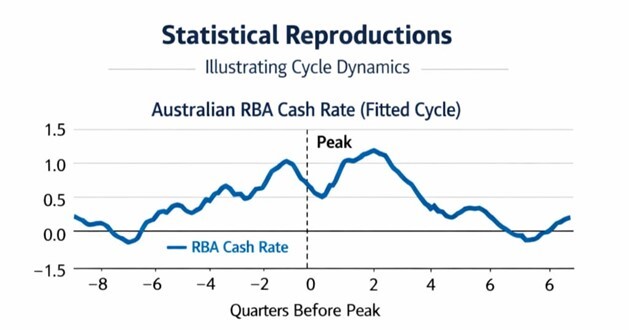

Reserve Bank of Australia Monetary Policy

The Reserve Bank of Australia eased the cash rate several times throughout 2025, gradually moving away from previously restrictive settings. Despite these cuts, monetary conditions are now approaching neutral rather than stimulative.

Lending costs have fallen and credit is more accessible. Household debt, however, remains elevated, limiting consumer spending and constraining overall demand. Compared with other major central banks, the RBA has taken a cautious approach. While G10 peers pursued aggressive rate reductions, the RBA maintained a measured “wait and see” bias.

As of January 2026, the cash rate stood at3.60% and 3.80%as of February 2026 moving away from the RBA’s target band of 2–3% target (Reserve Bank of Australia, 2026).

Neutral Interest Rate: The interest rate level that neither stimulates nor restricts economic growth when inflation is stable.

The Risk: Inflation is no longer driven by global supply chains but by domestic demand for services and high housing costs, making it harder to "break" with interest rates alone.

The cash rate chart illustrates the typical monetary policy path during an expansion. Interest rates generally rise as the economy nears its peak to curb inflation. However, the peak in the cash rate often occurs after the economic peak, as the RBA maintains restrictive settings to ensure price stability.

Fiscal Policy: Targeted Government Support

Australia’s fiscal policy in 2025 reflected a balance between supporting growth and maintaining sustainable public finances. According to the Mid-Year Economic and Fiscal Outlook (MYEFO), policy shifted away from broad demand stimulus.

Support is now targeted toward private-sector capacity building. This includes subsidies for “Future Made in Australia” green energy initiatives. The budget moved from surplus to a modest deficit, providing an expansionary impulse without excessive pressure on public debt.

Taxation and spending adjustments aim to support consumption and encourage investment. The approach remains measured, prioritising growth while preserving fiscal discipline.

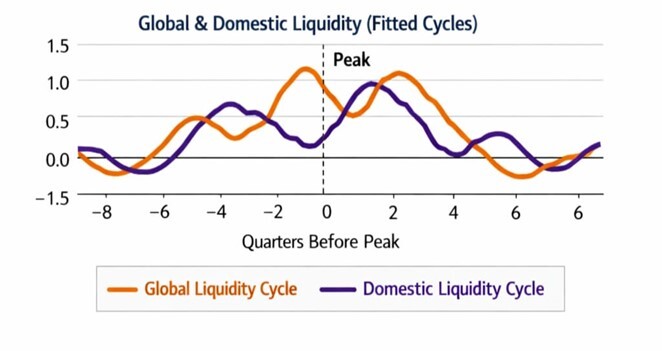

Domestic and Global Liquidity Conditions

Liquidity: Liquidity refers to the availability of credit and money within the financial system to support spending, investment, and asset prices.

Domestic Liquidity in Australia

Liquidity conditions for households and small businesses are gradually tightening. Elevated debt, higher borrowing costs, and cautious lending standards are weighing on discretionary spending and small-scale investment.

Credit remains available, but not loose by historical standards. Following RBA easing, borrowing costs have moderated and business debt is expanding slowly. Elevated debt burdens continue to limit spending capacity.

Takeaway: Liquidity is sufficient to sustain activity but does not provide a strong growth impulse.

Global Liquidity Backdrop

Global credit markets show early signs of cyclical recovery. As major central banks pause or cut rates, a liquidity floor has formed, preventing a systemic credit crunch.

Despite this, investor confidence remains fragile. Markets face a “wall of worry” driven by inflation volatility, geopolitical tensions, and shifting fiscal regimes. As a result, risk assets continue to experience sharp volatility even with adequate liquidity.

This suggests central banks can stabilize financial flow but cannot suppress price swings caused by macro uncertainty.

Comparative chart of global liquidity cycle and domestic liquidity cycle, showing synchronized peaks and cyclical market liquidity trends across quarters.

Key Insights: Global & Domestic Liquidity (Fitted Cycles)

Australia’s current economic position aligns with the critical juncture in the chart where global liquidity (orange) has peaked and begun to subside, while domestic liquidity (purple) remains temporarily elevated.

The ''lag'' explains why the domestic economy still exhibits firm employment and business activity even as the broader global support system thins out.

Australia is currently sitting in a vulnerability window between two major cycles. Domestic conditions are still supporting growth, but with global liquidity retreating, the expansion has lost momentum and become highly sensitive to external shocks such as shifts in international demand or rising global costs.

As a result, the economy is now on a fragile plateau, growth can continue, but without a global tailwind, Australia is increasingly exposed to being dragged down by higher costs or weakening global demand.

Geopolitical Risk and Trade Fragmentation

Geopolitical Risk: Economic risk arising from international conflict, trade policy shifts, sanctions, cyber threats, and strategic competition between states.

Australia balances a commodity super-cycle against growing trade fragmentation risks. The green energy transition boosts demand for critical minerals, supporting fiscal revenues. At the same time, rising protectionism and friend-shoring create volatile market access.

Sustained prosperity now depends as much on diplomatic agility as on resource abundance.

Macro Risk Transmission Channels

Geopolitical risks increasingly operate through policy rather than price. Global supply chains are being reshaped by national security priorities, replacing efficiency with resilience.

Domestic financial stability is also exposed to cyber threats targeting national infrastructure. Regulators warn that non-financial risks can rapidly trigger systemic shocks. With global risk premia unusually low, markets are vulnerable to disorderly reassessments.

Australia’s open economy status makes it a high-beta exposure to global stability. Escalations in trade or military conflict could rapidly transmit volatility through currency depreciation and higher borrowing costs.

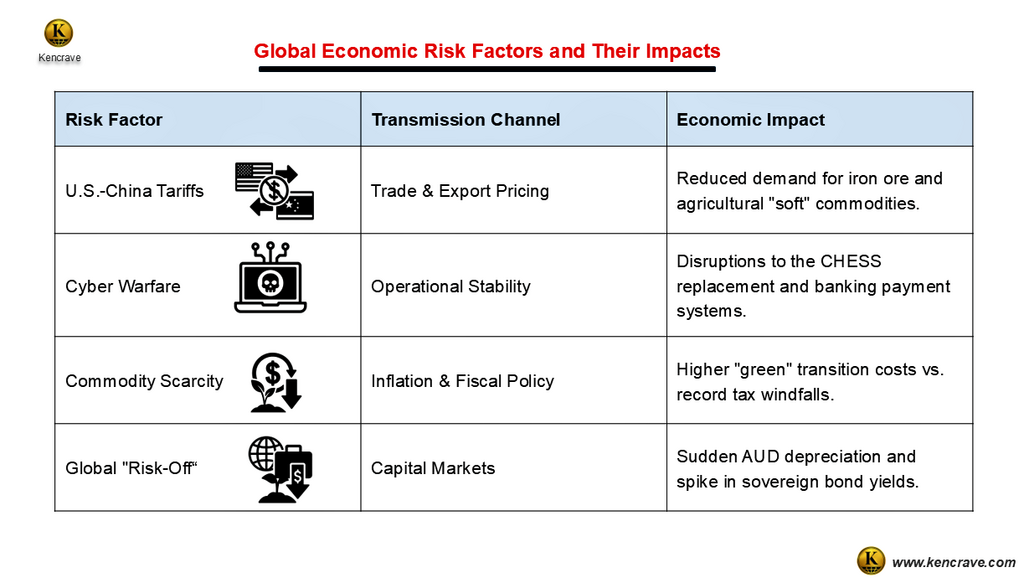

Table of global economic risk factors with transmission channels and impacts, including tariffs, cyber warfare, commodity scarcity, and capital market volatility.

Scenario Analysis: Australia Financial Markets 2026

With inflation, growth, and policy outcomes still uncertain, a scenario-based approach helps frame the range of possible paths for Australia’s economy in 2026. The scenarios below outline a base case and key upside and downside risks, and show how different outcomes could affect markets, policy decisions, and investment positioning.

The base case reflects the most likely continuation of current late-cycle dynamics, while the upside and downside scenarios capture asymmetric risks that could materially alter market outcomes and investment strategy.

What Would Invalidate the Base Case

The base case would be invalidated by a clear shift in inflation, growth, or financial stability dynamics. A faster-than-expected decline in services inflation, driven by rising labour slack, would allow earlier RBA easing and shift the outlook to the upside.

Conversely, a sharp global growth shock or accelerating household credit stress would overwhelm domestic resilience and push the economy into the downside scenario. Any of these outcomes would signal a regime change and require a reassessment of policy expectations and portfolio positioning.

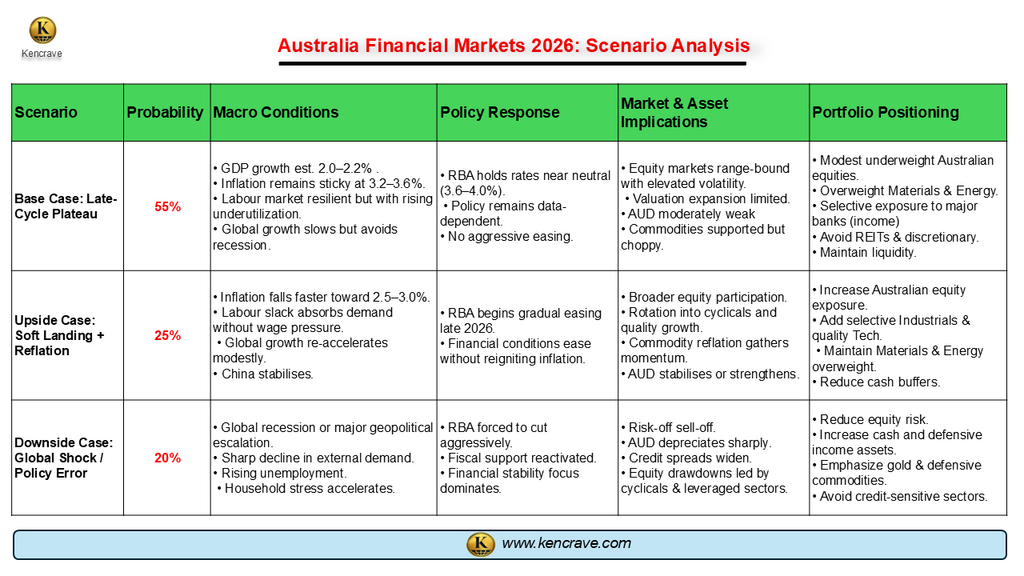

Scenario analysis chart of Australia’s 2026 financial markets showing base case, upside soft landing, and downside global shock with probabilities, policy responses, and portfolio strategies.

ASX Sector Sensitivity: The 4.25% Terminal Rate Stress Test

With inflation trending above the target range, markets are now pricing in a potential terminal rate of 4.25% (Money Management, 2026). This environment creates a sharp divergence in sector performance:

High-Risk Sectors (Underweight)

A-REITs: Property trusts are highly sensitive to the cost of capital. Higher rates lead to capitalisation rate adjustments, pressuring valuations (Pitcher Partners, 2026).

Technology & Growth: Valuation multiples for ASX tech (e.g., Wisetech, Xero) are compressing as higher discount rates reduce the present value of future earnings.