US 2030 supply chain transformation map showing reshoring to Mexico and friend-shoring with Europe, Japan, South Korea, and Australia for resilient operations. Image Credits: Kencrave

The U.S. Supply Chain Transformation: Reshoring, Nearshoring, And Friend Shoring For Resilience

The United States is undergoing a supply chain realignment, driven by global disruptions, geopolitical tensions, and the need for greater systemic resilience. An era defined by cost-focused globalization and just-in-time models prioritized efficiency at the expense of resilience (The World Economic Forum, 2020).

As reported by Al Jazeera in 2021, events like the COVID-19 pandemic and the 2021 Suez Canal incident exposed the risks of depending on distant, centralized supply chains. These crises revealed that low cost and speed were insufficient, prompting a strategic resurgence of priorities like stability, security, and oversight.

This transformation is now widely described as the US Supply Chain Transformation. It marks a move away from hyper-globalized sourcing toward a more regional, diversified, and politically aligned production system. Understanding how this transformation emerged and how it is being executed is essential for businesses, policymakers, and investors navigating the next phase of global trade.

From Just-in-Time Efficiency to Systemic Fragility

For decades, the dominant supply chain model relied on just-in-time production. Goods moved from Asian factories to US markets with minimal inventory and precise scheduling. The system reduced costs and boosted margins, but it assumed stable geopolitics, predictable transportation, and uninterrupted global trade.

Pandemic-related factory shutdowns, port congestion, container shortages, and record freight rates broke delivery timelines. The Ever Given incident alone delayed nearly $10 billion in trade per day (Bloomberg, 2021). These shocks exposed the risk of relying on single-region manufacturing for essential goods such as semiconductors, pharmaceuticals, and consumer staples.

What emerged was not a temporary disruption, but a structural failure. Firms and governments began to reassess supply chains as strategic assets rather than cost centers.

What Defines the US Supply Chain Transformation

The US Supply Chain Transformation is a coordinated shift led by both public policy and corporate strategy. Its objective is to reduce dependence on single-source overseas manufacturing, particularly in China, by diversifying production locations and shortening supply lines.

Three approaches define this transition.

Reshoring focuses on bringing manufacturing and critical supply chains back to the United States.

Nearshoring shifts production to geographically close partners, primarily Mexico and Canada.

Friend-shoring relocates supply chains to countries with strong political alignment, trade ties, and stable institutions.

These strategies form the backbone of a more regional and risk-aware supply chain model.

The Forces Driving the Transformation

Several forces made the old model unsustainable.

Geopolitical Tensions and National Security: The US-China trade conflict highlighted the vulnerability of relying on a strategic competitor for semiconductors, rare earths, and pharmaceuticals (The New York Times, 2025). The war in Ukraine exposed the risk of relying on adversarial countries for resources.

High Cost of Supply Chain Distribution: During the pandemic, delays and freight price spikes erased decades of cost savings from global sourcing. OECD data shows that logistical breakdowns outweighed efficiency gains, forcing businesses to reassess total supply chain cost rather than unit price alone.

Push for Resilience: Companies began shifting toward just-in-case approaches by holding safety stock, adding backup suppliers, and diversifying production footprints. Predictability and shock absorption replaced marginal cost optimization.

Government Legislation: Government policy accelerated the shift. The CHIPS and Science Act of 2022 provides over $52 billion to boost domestic semiconductor production. The Inflation Reduction Act of 2022 introduced tax credits for clean energy, electric vehicles, and battery production within North America.

Consumer and Investors Demand: Consumer and investor expectations also evolved. Buyers and investors increasingly value supply chain ethics, sustainability, and reliability. Firms with visible, local, and resilient operations gained reputational and strategic advantages.

The 3 Strategies of the Supply Chain Transformation

1. Reshoring and the Return of Domestic Manufacturing

Reshoring is rebuilding US industrial capacity after decades of offshoring. Investment is concentrated in advanced manufacturing, semiconductors, clean energy, and electric vehicles (Tech News World, 2025).

Major chipmakers are leading the trend. Intel is expanding fabrication plants in Arizona and building a large-scale semiconductor hub in Ohio. TSMC is constructing a multi-fab campus in North Phoenix. Samsung is developing a major semiconductor complex in Texas that combines production and research.

These projects strengthen intellectual property protection, create high-skilled jobs, and reduce exposure to global logistics shocks. They also face constraints. Labor costs are higher, and the supply of skilled manufacturing talent remains limited.

2.Nearshoring: The “China +1” Strategy

Nearshoring is among the most popular and scalable supply chain strategies, with Mexico being the primary beneficiary (Boston Consulting Group, 2024). Companies are adopting a China +1 model. They maintain Asian production for global markets while shifting US-focused output to Mexico. This approach helps reduce risk without a complete exit from Asia.

Key Structural Advantages of Mexico:

Proximity enables faster and cheaper truck and rail transport.

The USMCA trade agreement provides tariff-free access and regulatory predictability.

Shorter transit times reduce inventory risk and improve responsiveness.

As a result, Mexico has become a critical node in North American manufacturing, particularly for automotive, electronics, and consumer goods.

3.Friend-Shoring and Trusted Supply Networks

Friend-shoring adds a geopolitical dimension to supply chain design. Production is relocated to countries with strong diplomatic ties, stable governance, and aligned economic interests (The World Economic Forum, 2023).

Each partner plays a specific role. Canada supplies critical minerals. Japan and South Korea provide advanced electronics and battery technology. Australia supports lithium and raw material supply. India offers an alternative manufacturing hub with scale and growth potential.

The result is a distributed but trusted network that reduces exposure to political pressure and trade disruption.

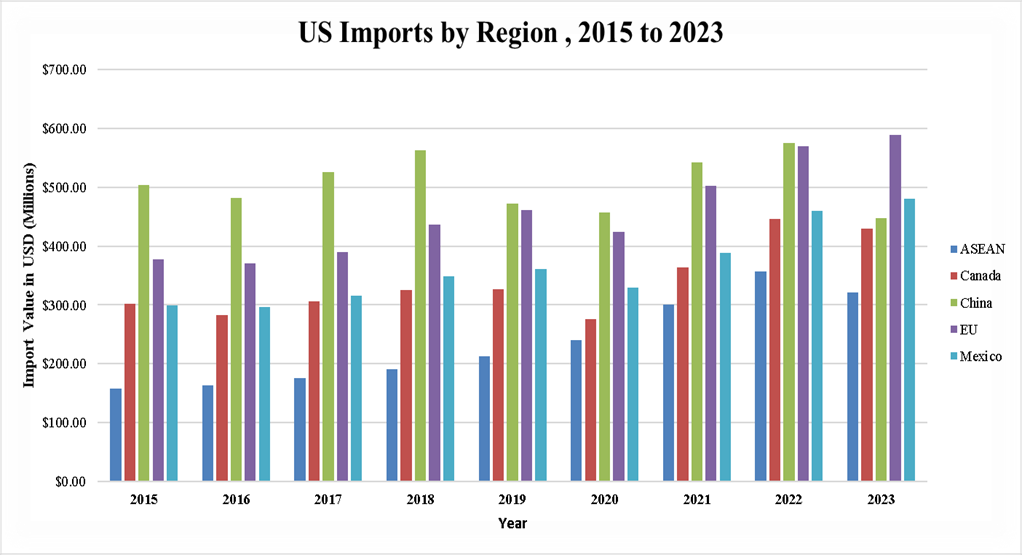

Bar chart showing US imports from major partners (ASEAN, Canada, China, EU, Mexico) from 2015–2023, highlighting shifts in trade volumes and diversification trends.

Key Insights from the US Import Trends by Region (2015–2023)

China’s share of US imports peaked in 2018 at $563 billion but fell to $448 billion by 2023, reflecting efforts to reduce dependence on a single source.

Mexico’s imports rose steadily from $299 billion in 2015 to $480 billion in 2023, highlighting its role as a nearshoring partner.

Canada remains a stable supplier, with imports increasing from $302 billion in 2015 to $430 billion in 2023, peaking at $447 billion in 2022.

ASEAN imports more than doubled, from $157 billion in 2015 to $321 billion in 2023, showing broader Southeast Asian sourcing.

EU imports grew from $378 billion to $589 billion, reflecting continued reliance on advanced machinery, pharmaceuticals, and high-value goods.

Implications: The US is actively diversifying supply sources, reducing reliance on China, strengthening nearshoring in Mexico, and broadening partnerships with ASEAN and EU countries to support supply chain resilience.

The Infrastructure and Technology Enablers

The supply chain transformation depends on modern infrastructure and advanced technology. For companies to rebuild a more resilient system, they have to upgrade the tools and the networks that support it.

Workforce Development: The new supply chain model depends on experts in logistics analysis, robotics, and advanced manufacturing. Investments in such areas help build a workforce that supports long-term growth.

Digital Supply Chains: Companies are deploying AI to forecast demand and spot risks early, IoT sensors to track goods in real time, and cloud platforms to connect every stage of production and transport. This transition increases supply chain transparency and operational agility.

Physical Infrastructure: The Bipartisan Infrastructure Law of 2021 allocates roughly $1.2 trillion between 2022 and 2026 to upgrade roads, rail, ports, and logistics corridors needed to handle increased domestic and regional freight.

Economic and Strategic Implications

The supply chain shift is already shaping the US economy, business decisions, and consumer expectations.

The US Economy With this shift, the growth of high-skilled, high-wage jobs in manufacturing will increase, and there will be reduced dependencies on adversaries for essential goods, strengthening national and economic security. Funding is flowing into regions that are building new factories, technology centers, and logistics hubs, creating momentum for industrial growth across the country.

Businesses The shift brings lower long-term risk but higher upfront costs. Production costs in the US, Mexico, or allied countries are higher, yet they protect businesses from long delays and shutdowns. Businesses must build partnerships with suppliers in Mexico, the US, and allied countries. To stay competitive, they will have to invest in advanced technologies that provide visibility across the chain.

Consumers Some products may cost more because of higher production costs, but with minimal shortages during crises and better availability trade-off. Consumers will have access to goods made in the US, which often come with confidence in quality and labor standards.

Strategic Risks and Critical Implementation Challenges

Systemic Strategic Risks

Geopolitical and Alliance Risks

Friend-shoring assumes long-term political alignment. This is not guaranteed. Leadership changes, trade policy shifts, or regional instability can weaken alliances over time. Overreliance on a narrow group of allied partners can recreate concentration risk under a different label.

Export controls, sanctions, or diplomatic disputes may still disrupt critical inputs such as semiconductors, critical minerals, or energy components.

Economic and Market Risks

Reshoring and nearshoring increase fixed costs. If global demand slows or inflation persists, higher cost structures can compress margins and reduce competitiveness.

Firms that restructure supply chains during economic downturns risk stranded assets if projected demand does not materialize. Currency volatility and interest rate fluctuations also affect cross-border investments in Mexico, Canada, and allied economies.

Execution and Timing Risks

Supply chain transformation is capital-intensive and slow. Semiconductor fabs, battery plants, and logistics hubs take years to reach scale. If execution lags behind geopolitical or market shocks, firms may remain exposed during the transition period. Poor sequencing of investments can lead to capacity bottlenecks, underutilized assets, or missed market windows.

Core Implementation Challenges

Workforce and Talent Pipeline

Advanced manufacturing requires engineers, technicians, data analysts, and automation specialists. The current US labor market does not supply these skills at a sufficient scale. Training pipelines lag capital deployment. Without coordinated investment in technical education, apprenticeships, and immigration pathways for skilled labor, new facilities will face chronic understaffing and lower productivity.

Cost Competitiveness and the Business Case

The U.S. based and allied manufacturing struggles to match Asia on unit cost. Energy prices, labor costs, and regulatory compliance raise production expenses. The business case for reshoring depends on valuing resilience, reliability, and risk reduction. Many firms still lack internal frameworks to quantify these benefits, making investment decisions harder to justify to shareholders focused on short-term returns.

Strategic Recommendations

For Policymakers and US Institutions

Align industrial policy with workforce strategy. Capital subsidies must be matched with funding for technical education, community colleges, and apprenticeship programs tied directly to new manufacturing projects.

Build redundancy into trade policy. Avoid concentrating friend-shoring incentives in a narrow set of countries. Broaden alliances across regions to prevent new single points of failure.

Accelerate permitting and infrastructure delivery. Delays in zoning, environmental reviews, and grid access increase execution risk and discourage private investment.

Standardize resilience metrics. Develop national frameworks for measuring supply chain risk so firms can incorporate resilience into financial decision-making.

For Multinational Corporations

Adopt portfolio based supply chain design. Balance cost-efficient global sourcing with regional redundancy rather than pursuing full reshoring or full globalization.

Invest in digital visibility. Real-time tracking, scenario modeling, and supplier risk analytics are now core operating capabilities, not optional upgrades.

Build long-term supplier partnerships. Stability comes from co-investment, shared data, and joint contingency planning with suppliers in Mexico, the US, and allied economies.

Quantify resilience value. Incorporate downtime risk, revenue loss, and reputational impact into capital allocation models.

For Investors

Reprice resilience. Favor firms with diversified sourcing, regional manufacturing footprints, and strong supply chain governance.

Target infrastructure and enablers. Logistics, grid modernization, industrial real estate, and supply chain software benefit directly from regionalization trends.

Assess execution capability. Capital alone is insufficient. Management teams with proven experience in large-scale industrial projects will outperform.

Take a long-horizon view. Returns from reshoring and friend-shoring accrue over years, not quarters.

Regionalization as the Dominant Supply Chain Model

The US Supply Chain Transformation is shaping a future built on predictable operations and regional networks. The shift away from hyper-global systems is permanent. Businesses are moving toward a structure that balances production across the United States, nearby trade partners, and trusted allies.

The goal is to create a supply chain that supports long-term growth and withstands disruption. Workforce and costs remain challenges, but they do not change the overall path. The priority now is strength and stability, not the lowest possible price. Resilience-centered supply chain design is now a core determinant of long-term US commercial and industrial competitiveness.

Key Takeaways

The US supply chain model is shifting from cost minimization to risk minimization.

Reshoring, nearshoring, and friend-shoring now define industrial strategy.

Government policy is actively reshaping manufacturing geography.

Mexico and allied economies are gaining lasting strategic importance.

Companies that invest early in supply chain visibility and redundancy will outperform.

Supply chain resilience is now a competitive advantage, not a contingency cost.

Frequently Asked Questions: US Supply Chain Transformation

1. What is the US Supply Chain Transformation?

The US Supply Chain Transformation is a shift toward reshoring, nearshoring, and friendshoring to reduce supply chain risk, improve resilience, and protect national and economic security.

2. Why is the US reshoring and nearshoring manufacturing?

The US is reshoring and nearshoring to reduce dependence on China, limit exposure to geopolitical risk, shorten supply lines, and prevent disruptions like those seen during the COVID-19 pandemic.

3.What is friend-shoring in supply chains?

Friend-shoring is the practice of relocating supply chains to politically aligned countries with stable institutions to reduce trade risk and ensure reliable access to critical goods.

4. How does supply chain regionalization affect businesses?

Regionalized supply chains increase resilience and reliability but raise production costs, requiring firms to invest in automation, digital visibility, and diversified supplier networks.

Since its public introduction, artificial intelligence (AI) has evolved from a niche technology into a strategic growth driver for modern businesses. Its ability to analyze vast datasets, automate complex workflows,...

Canada is entering a decisive decade. As global markets accelerate toward clean technologies, renewable energy, and climate-aligned investment, Canada’s green transition is emerging as both an economic necessity and a...

Executive Overview: U.S. Economic Independence and Strategic Resilience

The United States faces growing strategic dependence on foreign sources for critical minerals, advanced components, and manufacturing expertise. This dependency creates both...