Jamie Dimon at a JPMorgan podium with American and Chinese flags, rare earth minerals, and an industrial port scene, symbolizing global economic strategy and resource competition.

The Jp Morgan Doctrine: A $1.5 Trillion Blueprint For U.S. Economic Independence And Strategic Capitalism

Executive Overview: U.S. Economic Independence and Strategic Resilience The United States faces growing strategic dependence on foreign sources for critical minerals, advanced components, and manufacturing expertise. This dependency creates both economic and national security vulnerabilities, particularly in defense, energy, and technology.

In response, JPMorgan Chase & Co., under CEO Jamie Dimon, has launched a major initiative to restore U.S. economic independence by directing private capital into critical industries (JPMorgan Chase & Co., 2025). The bank’s $1.5 trillion sustainable growth plan, with $10 billion in direct equity and venture investments, positions finance as a strategic partner in national economic resilience.

What began as a global production shift has now evolved into a sustainability-driven economic model, emphasizing resilience, supply chain security, and technological leadership.

The Historical Foundations of American Capitalism and Economic Power

The American economy emerged from Enlightenment-era capitalism, influenced by Adam Smith’s The Wealth of Nations (1776). Built on free markets and private enterprise, it evolved through the Industrial Revolution, transforming the U.S. from an agrarian society into the world’s industrial leader.

By the early 20th century, corporate expansion and financial integration through Wall Street defined the U.S. model. However, globalization’s later phase, especially after the 1980s, shifted manufacturing overseas, fragmenting the domestic industrial base and exposing new vulnerabilities.

The 2001 Trade Policy Shift: U.S.–China Relations and Global Supply Chains

The early 2000s were a watershed moment. When the United States granted China Permanent Normal Trade Relations (PNTR) in 2001, it aimed to integrate China into a rules-based trading system. Policymakers justified the move in various ways.

Reasons for Granting PNTR to China

To secure Economic opportunities for the U.S. organizations: The U.S. companies would have been locked out of the massive trade benefit that came with China's joining the WTO, compared to other firms in Europe, Japan, and other nations.

To boost China’s reformers and strengthen U.S. influence: Granting PNTR strengthened the Chinese reformers who advocated for more open and market-based economic policies. Prohibiting PNTR would weaken the U.S. influence in shaping China’s final WTO membership terms, limiting the ability to ensure strong enforcement of trade rules.

To bring China into a Rules-Based Global System: The WTO’s dispute-settlement system enabled the U.S. to challenge unfair trade practices. The objective was to integrate China into the international rules-based system, promoting long-term reforms inside China that would make China’s growth more consistent with global standards and U.S. interests.

Yet, PNTR accelerated offshoring. Between 2001 and 2004, over 33% of U.S. manufacturing employment losses were linked to Chinese import competition. There were 25 production shifts from the U.S. to China, as seen with Apple, which outsourced its manufacturing operations to Foxconn, a Taiwanese multinational electronics manufacturer.

U.S. production shifts to China, India, and other Asian countries in Q1 2004 - bar and line chart

Key Insight:Post-PNTR, China saw the highest number of U.S. production shifts, reflecting early signs of strategic dependence.

By 2004, production had more than doubled to 58 productions, marking a new face of global manufacturing integration. Production in key sectors: electronics, machinery, and consumer goods, shifted rapidly to Asia. Companies like Apple, Caterpillar, and Boeing relocated supply chains to leverage lower costs, while domestic production declined in the U.S.

U.S. Supply Chain Dependence on Critical Minerals and Rare Earths

The U.S. Geological Survey (2023) reports that the U.S. is 100% import-reliant on several critical minerals, including rare earth elements, graphite, manganese, and tantalum, most of which originate from China (USGS Mineral Commodity Summaries, 2023).

A 2023 Al Jazeera report revealed that between 2020 and 2023, 70% of U.S. rare-earth imports came from China. These minerals are essential for modern technologies:

Electric vehicles

Smartphones

Defense systems (e.g, missile and jet engine components).

As of 2024, China controls over 60% of global rare-earth refining capacity and 85% of rare-earth magnet production, granting it powerful leverage over high-tech manufacturing (IEA, 2024).

Global map of critical minerals refining capacity highlighting China's 70% share in rare earths

Key Insight: China controls 70% of global rare earth refining, underscoring U.S. supply chain fragility.

This supply chain dependency exposes the U.S. to economic vulnerabilities and geopolitical risks, especially during global crises like the COVID-19 pandemic and ongoing trade tensions

Government Response: Executive Order 14017 and the 100-Day Supply Chain Review

Recognizing the threat of overdependence, the U.S. government issued Executive Order 14017 (2021) under President Joe Biden, initiating a 100-day review of critical supply chains (Executive Order 14017 – America’s Supply Chains)

The review focused on:

Energy and critical minerals

Information and communication technology

Medical products

Food and agriculture

Transportation and defense industries

This initiative marked the beginning of a national strategy for supply chain resilience, signaling a shift from globalization to domestic capacity building

Subsequent legislation, the CHIPS and Science Act (2022) and Inflation Reduction Act (2022), has allocated over $400 billion toward domestic semiconductor manufacturing, clean energy, and advanced industries.

This policy shift signals a new economic doctrine: “strategic capitalism.” Instead of prioritizing global efficiency, the U.S. now emphasizes selective economic sovereignty and balancing open markets with domestic capacity.

JPMorgan Chase and U.S. Strategic Capitalism: $1.5 Trillion Plan for Economic Resilience

Jamie Dimon, CEO of JPMorgan Chase, in his speech published on October 13, 2025, notes “the US has become too reliant on unreliable sources of critical minerals, products, and manufacturing, all of which are essential for US national security” (JPMorgan Chase & Co., 2025).

To counter this, JPMorgan announced a $1.5 trillion, decade-long initiative, including $10 billion in direct equity and venture investments across four strategic pillars:

Advanced Manufacturing & Supply Chains: Robotics, automation, and critical minerals.

Defense & Aerospace: Drones, space tech, and secure communications.

Energy Resilience: Battery storage, hydrogen, and distributed energy.

Frontier Technologies: AI, quantum computing, and cybersecurity.

As the JPMorgan doctrine outlines a $1.5 trillion investment in strategic industries, the long-term trajectory of rare earth element (REE) supply becomes a critical lens for evaluating U.S. economic independence.

The chart below illustrates projected mining and refining capacities across China, the U.S., and Australia through 2040. While the U.S. and Australia show steady growth in mining, China maintains a commanding lead in refining, underscoring the urgency for domestic infrastructure investment in processing and value-added capabilities.

Projected global rare earth supply trends for China, U.S., and Australia – mining vs. refining (2022–2040)

Key Insight:China maintains refining dominance through 2040, while U.S. and Australia expand mining capacity, highlighting the need for strategic investment in domestic refining.

JP Morgan has structured a key investment of $1 billion in MP Materials, supporting U.S. rare-earth magnet production, reducing reliance on Chinese inputs. JPMorgan’s role exemplifies financial alignment with national strategy, redefining capitalism as a partner to security and sustainability.

Global Comparison: JPMorgan’s Strategic Capitalism vs. Global Financial Peers

JPMorgan’s “strategic capitalism” approach contrasts with peers:

BlackRock has focused on ESG-aligned sustainability, emphasizing decarbonization and climate resilience but not industrial independence.

Goldman Sachs has targeted venture-tech investments (AI, green startups) with smaller direct industrial exposure.

Sovereign wealth funds such as Singapore’s Temasek and the UAE’s Mubadala have invested heavily in critical minerals projects abroad, but primarily for-profit diversification, not national security.

Thus, JPMorgan’s plan stands out as a domestic industrial-security investment model, integrating finance, policy, and technology, a modern reimagining of Hamiltonian industrial capitalism.

Global Critical Minerals Market: China’s Refining Dominance and U.S. Vulnerability

The International Energy Agency’s (IEA) Global Critical Minerals Outlook 2025 shows that China controls over 70% of global rare earth refining capacity, owing to decades of strategic investment and technological mastery (IEA, 2025).

Price manipulation risks from China could undercut new entrants.

Even with rising U.S. public and private investments, full independence could take a decade or more. The report underscores that economic security equals national security in today’s geopolitical landscape.

U.S. Human Capital Crisis: Addressing STEM Skills Gaps in Critical Industries

Rebuilding domestic manufacturing is not just a question of capital; it also demands expertise. The U.S. faces a shortage of chemical engineers, metallurgists, and technicians skilled in rare earth separation and processing.

Key challenges:

Expertise Deficit: Few professionals possess hands-on experience in rare-earth production.

Training Lag: New education and vocational programs approximately take 5–10years to yield results.

Brain Drain: Skilled professionals continue migrating to global hubs with more mature industrial ecosystems.

Without an equivalent focus on human capital development, financial investments like JP Morgan’s $10 billion investment alone will fail to rebuild domestic supply chain capacity.

“A factory is useless without the intelligence to run it.”

A successful economic-independence strategy, therefore, depends on parallel STEM education reform, apprenticeship funding, and industrial knowledge retention.

Strategic Outlook: Reclaiming U.S. Control of Industrial and Supply Chain Power

China’s entrenched dominance, over 60% of refining and 80% of processing capacity, poses a structural challenge (IEA, 2024).

U.S. projects face longer permitting, higher costs, and stricter environmental standards, extending the recovery timeline. Nonetheless, with over $500 billion in combined public-private commitments announced since 2021, the groundwork for industrial reshoring is solidifying.

By 2035, U.S. domestic processing of rare-earth elements could rise from 5% today to 25–30%, provided permitting and workforce development proceed as planned.

Policy Recommendations: Building a Resilient U.S. Economy

To reduce dependency and strengthen industrial capacity, a multi-stakeholder approach is essential

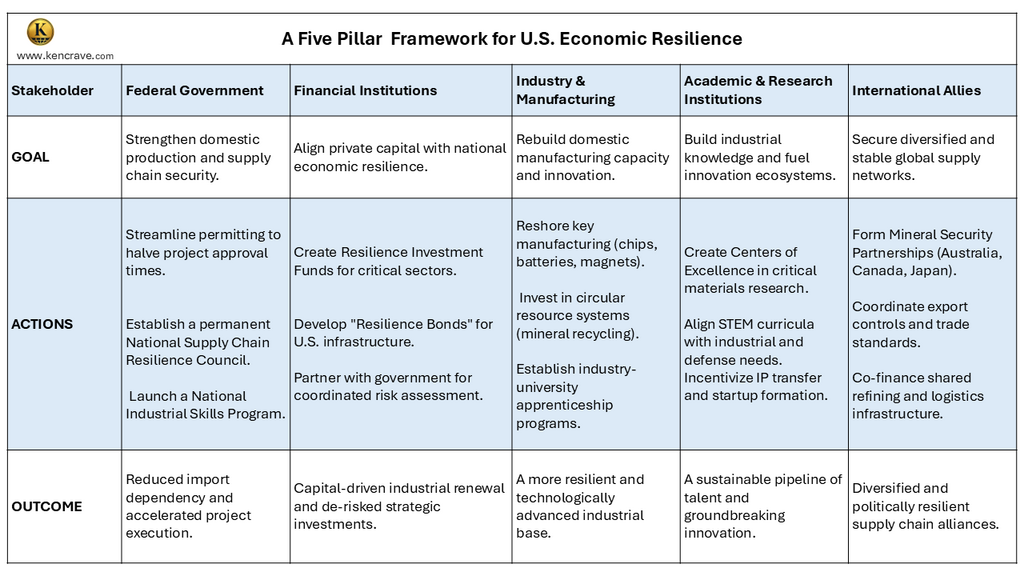

1. Federal Government

Goal: Strengthen domestic production and supply chain security.

Streamline permitting to halve project approval times (3–5 years).

Establish a permanent National Supply Chain Resilience Council.

Launch a National Industrial Skills Program to rebuild STEM expertise.

Expected Outcome: Lower dependency and faster project execution(White House EO 14017)

2. Private Financial Institutions

Goal: Align investment with national resilience.

Create Resilience Investment Funds for critical sectors.

Develop Resilience Bonds to fund U.S.-based infrastructure.

Partner with the government for coordinated risk assessment.

Goal: Build industrial knowledge and innovation ecosystems.

Create Centers of Excellence in critical materials research.

Align STEM curricula with industrial and defense needs.

Incentivize IP transfer and startup formation.

Expected Outcome: Strengthened innovation and talent pipelines.

5. International Allies & Partners

Goal: Secure diversified global supply networks.

Form Mineral Corridors with allies (Australia, Canada, Japan).

Coordinate export and trade standards.

Co-finance shared refining and logistics infrastructure.

Expected Outcome: Diversified and stable supply chain alliances (IEA 2025 Outlook).

Strategic capitalism policy matrix showing stakeholder goals, actions, and outcomes for U.S. economic resilience and rare earth supply chain security

Key Takeaways: Strategic Capitalism and U.S. Economic Independence

Economic Model Shift: U.S. capitalism is restructuring toward sustainability and resilience.

Entrenched Dependence: China remains the primary supplier for key inputs.

Private Capital as Policy Partner: JPMorgan’s initiative demonstrates the private sector’s central role in national resilience.

Decade-Long Challenge: Industrial renewal will require time, coordination, and talent.

Economic Security = National Security: The alignment of finance, policy, and innovation defines 21st-century competitiveness.

JPMorgan Chase’s $1.5 trillion initiative marks a pivotal evolution in U.S. capitalism, from global efficiency to domestic resilience. The integration of private finance with national objectives redefines the role of markets in safeguarding sovereignty.

While rebuilding industrial autonomy is a long-term endeavor, coordinated policy, capital investment, and education reform can transform dependency into strength. In the emerging age of strategic capitalism, economic independence is not merely a financial goal; it is the cornerstone of national power.

The United States is undergoing a supply chain realignment, driven by global disruptions, geopolitical tensions, and the need for greater systemic resilience. An era defined by cost-focused globalization and just-in-time...

Since its public introduction, artificial intelligence (AI) has evolved from a niche technology into a strategic growth driver for modern businesses. Its ability to analyze vast datasets, automate complex workflows,...

Canada is entering a decisive decade. As global markets accelerate toward clean technologies, renewable energy, and climate-aligned investment, Canada’s green transition is emerging as both an economic necessity and a...

.png)

.png)