14 min read

De Dollarization In 2026: How The Iran Crisis, Brics+, And Yuan Oil Trade Are Reshaping The Global Financial System

Asia

Politics

A Policy Analysis of Emerging Multipolar Financial Dynamics

Executive Summary

The 1974 petrodollar system is gradually eroding as geopolitical shocks (Russia sanctions, Iran conflict) drive nations toward yuan-based oil settlements. In early 2026, India paid for Iranian crude in yuan, and Iran explored a yuan-for-passage policy in the Strait of Hormuz, making the petroyuan a new alternative to the dollar in oil settlement. With BRICS+ controlling 42% of global oil production and 38 African nations exploring China's CIPS payment system, the world is showing early signs of a multipolar financial era. The dollar remains strong (48% of global payments), but it is no longer the only currency alternative in global trade settlements.

The global energy trade has experienced early shifts in 2026, signaling a progressive realignment in the "de-dollarization" of the global economy. This change has been driven by geopolitical scenarios resulting in the need for strategic financial diversification. However, this change can be traced back over fifty years from the 1970s and now includes new economic blocs such as the BRICS nations, major oil producers, and emerging African markets.

The 1974 petrodollar system is gradually eroding as geopolitical shocks (Russia sanctions, Iran conflict) drive nations toward yuan-based oil settlements. In early 2026, India paid for Iranian crude in yuan, and Iran explored a yuan-for-passage policy in the Strait of Hormuz, making the petroyuan a new alternative to the dollar in oil settlement. With BRICS+ controlling 42% of global oil production and 38 African nations exploring China's CIPS payment system, the world is showing early signs of a multipolar financial era. The dollar remains strong (48% of global payments), but it is no longer the only currency alternative in global trade settlements.

The global energy trade has experienced early shifts in 2026, signaling a progressive realignment in the "de-dollarization" of the global economy. This change has been driven by geopolitical scenarios resulting in the need for strategic financial diversification. However, this change can be traced back over fifty years from the 1970s and now includes new economic blocs such as the BRICS nations, major oil producers, and emerging African markets.

The Petrodollar System: How the U.S. Dollar Became the Global Reserve Currency

The foundation of the modern financial age was laid in the mid-1970s, specifically following the 1973 oil crisis. In 1974, the United States and Saudi Arabia struck a landmark deal in which the U.S. would provide military protection to the Saudi Kingdom in exchange for an agreement to price and sell oil exports to any nation exclusively in U.S. dollars. This created what is now known as the Petrodollar System.

This petrodollar system created a continuous global demand for the U.S. dollar, cementing the U.S. dollar as the world's undisputed reserve currency. It allowed the U.S. to finance its spending with unparalleled ease by recycling these petrodollars back into the American economy through Treasury bonds.

BRICS and De-Dollarization: How Emerging Economies Are Reducing Dollar Dependence

For years, the BRICS nations (Brazil, Russia, India, China, and South Africa) discussed reducing dollar reliance, but geopolitical events turned these discussions into a formidable policy ready for execution. Following the 2022 invasion of Ukraine, Russia was heavily sanctioned by the U.S. and European countries from dollar-based transactions, leading it to move almost entirely away from the dollar in bilateral trade.

The result: most bilateral trade has shifted away from dollar settlement to settlement in Russian Rubles and Chinese Yuan.

At the 2024 BRICS summit in Kazan, the bloc emphasized advancing yuan settlement alongside other local currencies. The addition of major oil exporters like Iran, the UAE, and Egypt to BRICS+ in 2024 significantly enhanced the group's collective bargaining power, as the expanded bloc now constitutes approximately 42% of global oil production and nearly 45% of proven global oil reserves, increasing its collective leverage in energy market.

Compared to G7 nations, which account for an estimated 26% of oil production (with the majority from Canada and the U.S.), this reflects BRICS' potential influence over global oil production and supply dynamics.

Yuan Oil Trade and the Rise of the Petroyuan in Global Energy Markets

In early 2026, amidst the Israel-US conflict with Iran in the Middle East, the "Petroyuan" led to early-stage petroyuan operational mechanisms in oil across several bilateral trade corridors:

- India: Seeking to manage high energy prices and bypass USD sanctions, Indian refiners led by the state-owned Indian Oil Corporation (IOC) began settling payments for Iranian crude oil in yuan via ICICI Bank's Shanghai branch.

- Iran explored a yuan-linked passage framework: In March 2026, Iran granted safe passage to vessels from a "Yuan Bloc" including India, Russia, China, Iraq, and Pakistan, that agreed to trade or pay tolls in yuan.

- China's Dominance: China now purchases approximately 90% of Iran's oil, with imports reaching up to 1.8 million barrels per day in 2025, mostly settled in yuan through specialized institutions like the Bank of Kunlun to prevent U.S. sanctions.

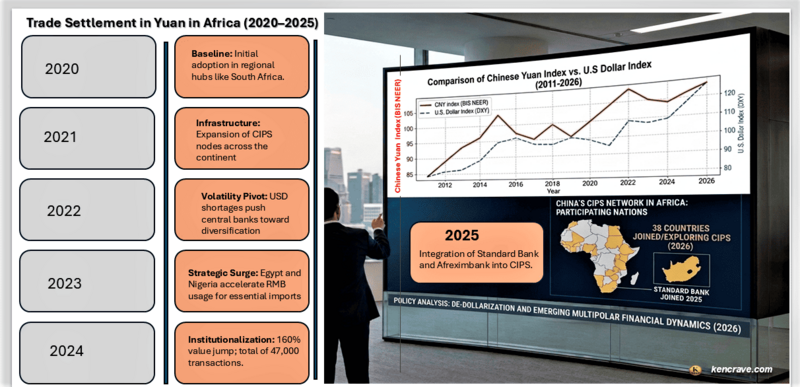

The Chinese Yuan Expansion into Africa

The BRICS efforts to settle international payments in Chinese yuan have resulted in some African countries exploring the adoption of the Chinese yuan in global deals. By late 2025 and early 2026, several African nations integrated the yuan as a form of managing debt and commerce:

- Nigeria & Angola: These nations expanded currency swap deals and yuan-denominated settlements to bypass dollar risks and repay loans.

- Kenya: In early 2026, it converted $3.5 billion of its dollar-denominated debt into yuan, seeking cheaper repayment options. The Kenyan government continues to explore direct convertibility between the shilling and yuan to lower trade costs and repay debts more cheaply.

- Zambia: Became the first African nation to allow mining companies to pay taxes and royalties in yuan to service its Chinese debt. This has enabled the country to service its Chinese debt more cost-effectively and aligns with its status as a major copper exporter to China.

- The CIPS Network: Roughly 38 African countries have joined or explored China's Cross-Border Interbank Payment System (CIPS), a parallel financial infrastructure independent of the Western-led SWIFT system. In late 2025, South Africa, through the Standard Bank of South Africa, became the first African bank to plug directly into China's Cross-Border Interbank Payment System (CIPS), allowing businesses to settle invoices in Chinese yuan and bypass the dollar.

1. The Yuan's Long-Term Appreciation

Since 2011, the Chinese Yuan Index (BIS NEER) has seen a structural upward shift, moving from the mid-80s to over 108. This indicates that, despite fluctuations against the U.S. dollar, the yuan has significantly strengthened against almost everyone else it trades with over the last 15 years.

2. A Powerful Dollar vs. A Steady Yuan (2022–2026)

The sharp rise in the DXY (approaching 120 by 2026) reflects an exceptionally strong U.S. dollar. Interestingly, the CNY Index has remained elevated (around 108) during this same period. This suggests that the yuan is not just following the dollar but is maintaining its own independent strength against other major currencies like the euro, yen, and British pound.

3. Reduced Correlation: Breaking Away from the U.S.

In the past (early 2010s), the U.S. and Chinese currencies usually moved in the same direction. Now, they are moving more independently. This "decoupling" shows that China's economy and monetary rules showing reduced short-term correlation with U.S. monetary movements such as interest rates and banking.

4. Toughness in a Messy Market

The fact that the yuan is staying near its highest value ever in 2026, even while the world economy is shaky and the dollar is surging, suggests how resilient the Chinese currency has become. It isn't easily pushed around by global chaos compared to historical volatility.

Economic Implications

For Global Trade and Competitiveness

- Export Pressure for China: A high CNY Index means Chinese goods are becoming more expensive for buyers in Europe, Southeast Asia, and Japan. To maintain its trade surplus, China may shift from low-cost manufacturing to high-value innovation as a way to justify these higher price points.

- U.S. Trade Deficit: A surging DXY makes U.S. exports more expensive and imports cheaper, which could lead to a widening trade deficit but help cool domestic inflation by lowering the cost of imported goods.

For Monetary Policy and Inflation

- Inflation Buffer: For China, a strong trade-weighted yuan acts as a cushion against imported inflation (such as energy and raw material costs priced in dollars). For the U.S., the extreme strength of the DXY suggests tight monetary policies, likely driven by higher interest rates relative to the rest of the world.

- Capital Flows: The strength of both indices indicates a "flight to quality" or "flight to stability." This means that investors are betting on the two largest economies, potentially draining liquidity from smaller emerging markets.

For the Global Financial System

- De-dollarization vs. Dollar Dominance: While the DXY shows the dollar is at its strongest point in decades, the steady high level of the CNY Index supports China's efforts to increase the yuan's role as a global reserve currency. Trade partners may increasingly settle debts in yuan to avoid the high costs associated with an expensive U.S. dollar, as evidenced by the latest international payments in Chinese yuan by different countries.

The Future of De-Dollarization: Multipolar Financial System or Fragmented Markets?

The rise of the petroyuan does not mean the dollar will collapse overnight; it still accounts for roughly 48% of global payments. However, the world is slowly entering a "multipolar" financial era:

- Financial Bifurcation: The global system is partially splitting into Western bloc centered on the USD/euro and an Eastern/Global South bloc centered on the yuan and local currencies.

- Reduced U.S. Influence: As more nations bypass the American banking system, the effectiveness of U.S. economic sanctions continues to decline due to the adoption of policies such as government-to-government settlements and regional bloc payment integrations.

- Resilience for Sanctioned States: For nations like Iran and Russia, these alternative settlement options have provided a vital economic safety zone during times of extreme pressure.

How the U.S. Could Slow the Transition to a Multipolar Financial World

The U.S. Federal Reserve currently faces a pivotal role and a difficult period in recent years, as it navigates a transition toward a more multipolar financial world. While the Fed's formal mandate focuses on domestic maximum employment and stable prices, it may require a proactive strategy to maintain the dollar's competitive edge in the multipolar financial world.

This is by:

- Prioritizing long-term macro-stability and fiscal credibility.

- Investing in digital infrastructure. This could involve a central bank digital currency. Through such dollar tools, it could help the U.S. compete with rising alternative payment systems like China's CIPS.

- Policy shifts: In 2026, the Fed is expected to diverge from other central banks, with a potential bias toward easing (one to two rate cuts) if employment softens, despite persistent geopolitical risks.

- Strengthening Global Liquidity Networks. To ensure the dollar remains the world's primary alternative during crises, the Fed maintains liquidity swap lines with other foreign central banks. This reinforces the dollar's role as the ultimate safe-haven asset even in a multipolar world.

Policy Recommendations for Navigating De-Dollarization and Currency Diversification

1. State Actors & Monetary Authorities

Pursue selective currency diversification

Expand bilateral currency swap agreements with BRICS+ and emerging markets to reduce overreliance on the U.S. dollar, while maintaining sufficient dollar liquidity for global trade stability.

Expand bilateral currency swap agreements with BRICS+ and emerging markets to reduce overreliance on the U.S. dollar, while maintaining sufficient dollar liquidity for global trade stability.

Adopt a dual-system strategy (SWIFT + alternatives)

Engage with alternative payment systems such as CIPS where strategically beneficial, but retain access to established systems like SWIFT to preserve flexibility and global interoperability.

Engage with alternative payment systems such as CIPS where strategically beneficial, but retain access to established systems like SWIFT to preserve flexibility and global interoperability.

Diversify foreign exchange reserves cautiously

Gradually rebalance reserves to include yuan, gold, and other currencies as hedges, while recognizing liquidity, convertibility, and governance differences compared to dollar assets.

Gradually rebalance reserves to include yuan, gold, and other currencies as hedges, while recognizing liquidity, convertibility, and governance differences compared to dollar assets.

Develop and test CBDCs (pilot-based approach)

Invest in central bank digital currencies through pilot programs and cross-border experiments (e.g., mBridge), focusing on interoperability rather than full-scale immediate deployment.

Invest in central bank digital currencies through pilot programs and cross-border experiments (e.g., mBridge), focusing on interoperability rather than full-scale immediate deployment.

Negotiate resource-backed trade agreements selectively

Explore yuan- or local-currency-denominated trade deals (energy, minerals, agriculture) where economically advantageous, while avoiding excessive dependency on a single external partner.

Explore yuan- or local-currency-denominated trade deals (energy, minerals, agriculture) where economically advantageous, while avoiding excessive dependency on a single external partner.

2. Private Sector: Finance & Commerce

Maintain multi-currency operating capacity

Open and manage accounts in multiple currencies (including yuan where relevant) to increase settlement flexibility, especially in trade corridors involving emerging markets.

Open and manage accounts in multiple currencies (including yuan where relevant) to increase settlement flexibility, especially in trade corridors involving emerging markets.

Hedge across multiple currency exposures

Expand hedging strategies beyond USD pairs to include yuan and other regional currencies, particularly where trade flows are shifting.

Expand hedging strategies beyond USD pairs to include yuan and other regional currencies, particularly where trade flows are shifting.

Use dual-contract pricing structures where needed

Incorporate optional currency clauses (USD and alternative currencies) in commodity and trade contracts to manage volatility and geopolitical risk.

Incorporate optional currency clauses (USD and alternative currencies) in commodity and trade contracts to manage volatility and geopolitical risk.

Strengthen sanctions and compliance frameworks

Develop internal controls to navigate both Western and non-Western financial systems, ensuring strict adherence to sanctions laws and minimizing exposure to secondary sanctions.

Develop internal controls to navigate both Western and non-Western financial systems, ensuring strict adherence to sanctions laws and minimizing exposure to secondary sanctions.

Diversify financing channels cautiously

Engage with a broader range of financial institutions (including non-Western banks) where appropriate, but only within legal and regulatory boundaries and with full risk assessment.

Engage with a broader range of financial institutions (including non-Western banks) where appropriate, but only within legal and regulatory boundaries and with full risk assessment.

3. Financial Infrastructure & Payment Systems Operators

Build interoperability, not replacement

Focus on integrating yuan and other currency settlement capabilities into existing systems rather than attempting full substitution of current infrastructure.

Focus on integrating yuan and other currency settlement capabilities into existing systems rather than attempting full substitution of current infrastructure.

Develop dual-system messaging capabilities

Invest in systems that can process transactions across multiple networks (e.g., SWIFT and CIPS), reducing friction in cross-border trade.

Invest in systems that can process transactions across multiple networks (e.g., SWIFT and CIPS), reducing friction in cross-border trade.

Enhance compliance and monitoring systems

Implement advanced sanctions screening and transaction monitoring tools that can operate across parallel financial networks.

Implement advanced sanctions screening and transaction monitoring tools that can operate across parallel financial networks.

Support CBDC experimentation and cross-border pilots

Participate in early-stage CBDC interoperability projects to remain competitive in evolving payment ecosystems.

Provide diversified liquidity solutions

Offer liquidity facilities in multiple currencies (including yuan where demand exists), while maintaining strong dollar liquidity given its continued global dominance.

Participate in early-stage CBDC interoperability projects to remain competitive in evolving payment ecosystems.

Provide diversified liquidity solutions

Offer liquidity facilities in multiple currencies (including yuan where demand exists), while maintaining strong dollar liquidity given its continued global dominance.

Strategic Risks and Trade-Offs in a De-Dollarizing World

-

Dollar dominance remains structural

The U.S. dollar continues to lead in global reserves, trade invoicing, and financial markets. Any transition will be gradual, not abrupt. -

Yuan adoption has limitations

Capital controls, limited convertibility, and institutional transparency constraints may restrict the yuan’s faster global scalability. -

Fragmentation, not full bifurcation

The global system is more likely to evolve into overlapping financial networks rather than a clean USD vs. CNY split. -

Geopolitical alignment risks

Deep integration into alternative systems may carry political and economic trade-offs, particularly for globally exposed economies. -

Dual-system participation is the base case

Most countries and firms will operate across both dollar-based and alternative systems rather than fully shifting away from one.

Bottom Line: Rather than a full transition away from the dollar, stakeholders should prepare for a more complex, multi-currency global system, where flexibility, compliance, and diversification, not replacement, are the defining strategies.

Key Takeaways

- The 1974 petrodollar system is gradually eroding as oil is settled in yuan in in selected cases.

- BRICS nations control about 42% of global oil production, giving member nations leverage to bypass the dollar.

- Iran’s yuan-for-passage policy in the Strait of Hormuz (March 2026) made the petroyuan a functional reality in some cases.

- China’s CIPS network now includes an estimated 38 African countries, offering a direct SWIFT alternative.

- The world is increasingly becoming multipolar: the dollar remains strong (48% of payments), it is no longer the sole settlement currency in all major trade flows.

Frequently Asked Questions About De-Dollarization and the U.S. Dollar

1. What is de-dollarization?

De-dollarization refers to the process by which countries reduce their reliance on the U.S. dollar for international trade, reserves, and financial transactions. This includes using alternative currencies such as the Chinese yuan, engaging in bilateral trade agreements, and adopting non-dollar payment systems.

2. Why are countries moving away from the U.S. dollar?

Countries are diversifying away from the dollar due to U.S. sanctions risks, currency volatility, geopolitical tensions, the rise of alternative systems like CIPS. This shift is particularly visible among emerging markets and sanctioned economies.

3. Is the U.S. dollar losing its global dominance?

The U.S. dollar remains the dominant global currency, especially in reserves and financial markets. However, its exclusive role is gradually being challenged as more countries experiment with alternative settlement currencies.

4. What is the petroyuan?

The “petroyuan” refers to oil trade settled in Chinese yuan instead of U.S. dollars. While not a full replacement for the petrodollar system, it represents a growing alternative in specific bilateral trade relationships.

The “petroyuan” refers to oil trade settled in Chinese yuan instead of U.S. dollars. While not a full replacement for the petrodollar system, it represents a growing alternative in specific bilateral trade relationships.

5. How does BRICS influence de-dollarization?

BRICS countries promote local currency trade, expand financial cooperation, and support alternative payment systems. Their growing share of global trade and energy production gives them increasing influence in reducing dollar dependency.

BRICS countries promote local currency trade, expand financial cooperation, and support alternative payment systems. Their growing share of global trade and energy production gives them increasing influence in reducing dollar dependency.

6. What role does Africa play in de-dollarization?

Several African nations are exploring yuan-based trade, currency swaps, and participation in alternative payment systems to reduce dollar exposure and manage external debt more efficiently.

Senior Editor: Kenneth Njoroge

Business & Financial Expert | MBA | Bsc. Commerce | CPA

Author Name

Author intro

Author bio goes here.