The Economic Cost of Discrimination Against Women-Led Startups

UN Women emphasizes that investing in women is one of the most powerful drivers of economic growth, with the potential to unlock $342 trillion in global gains by 2050." - UN Women, Global Report on Women's Economic Empowerment, 2025

The Global Funding Gap Facing Women Entrepreneurs

Executive Overview

The global startup ecosystem is celebrated as a meritocracy, a space where the best ideas, executed by the most capable teams, rise to the top. Yet mounting evidence from every corner of the world exposes a deeply troubling reality: women-led start-ups are systematically denied equal access to the capital, grants, and loans they need to survive and scale.

In 2025, women-only founding teams received just roughly 2% of total global venture capital funding with the 2% serving as a baseline against which every region’s gap can be measured. Male-only teams captured about 82-84%. Mixed-gender teams claimed the remaining estimate of 14%. This persistent imbalance reflects a decades-old structural failure that continues despite growing awareness, investor pledges, and women-focused funding initiatives

The discrimination is not confined to Africa, though the continent's challenges are acute. From Silicon Valley to Singapore, from London to Lagos, from São Paulo to Seoul, women entrepreneurs face higher interest rates, stricter collateral demands, lower grant approval rates, shorter pitch meetings, and more skeptical questioning from investors. The bias is embedded in algorithms, institutional culture, legal frameworks, and social norms.

The economic cost is staggering. The McKinsey Global Institute estimates that advancing women's equality in entrepreneurship and the broader economy could add $12 trillion to global GDP. The World Bank projects that closing the gender gap in African entrepreneurship alone could unlock $300 billion by 2030. Yet despite these numbers, the pace of change remains glacially slow.

This analysis explores the root causes, regional dimensions, economic implications, and strategic pathways for dismantling gender discrimination in startup financing. It draws on the latest data, case studies, and policy frameworks from across the world, offering a comprehensive roadmap for investors, policymakers, entrepreneurs, and civil society.

How Much Venture Capital Do Women-Led Startups Receive?

Understanding the scale of the problem requires confronting hard data. The following figures paint a consistent picture across regions and time periods.

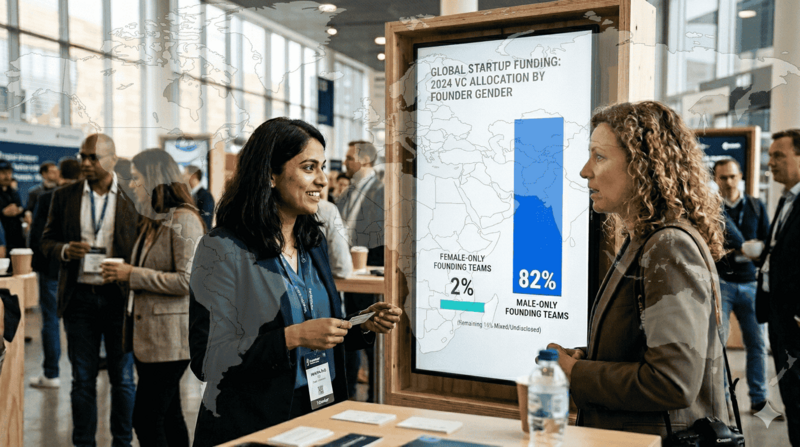

Global Venture Capital Funding by Founder Gender (2024-2025)

Figure 1: Global VC funding by founder gender in 2024-2025: 82 male-only, 2% female-only, 16% mixed teams.

Takeaway: Women led teams are extremely underfunded representing a share of 2% in the global share of venture capital funding compared to male led businesses (82%) and mixed teams (16%).

Regional Breakdown of Women-Led Startup Funding

The chart below illustrates global disparity in venture capital for women startups.

Figure 2: World map of women’s venture capital share by region.

Why Women Entrepreneurs Face Greater Difficulty Accessing Business Loans

Gender gap disparity is also prevalent in loan accessibility by women entrepreneurs with the following statistics showing regional contrasts:

Global Loan Denial Probability. Women-managed firms are roughly 5 percentage points less likely to receive a loan than comparable male-owned firms.

In Sub-Saharan Africa, the gender financing gap for SMEs stands at $42 billion which is the largest financing gap for women entrepreneurs in the world relative to economic size, with a specific $15.6 billion deficit in the agriculture sector alone.

In South Asia, women entrepreneurs pay interest rates 2-4 percentage points with global averages for this disparity often around 0.5 percentage points when controlling for all creditworthiness factors.

In the United States, women-owned firms with low credit risk are approved for business loans at a rate of 68%, compared to 78% for their male counterparts which is a 10-percentage point gap in approval rather than a 31% difference in total funding amounts.

In Europe, the European Investment Bank (EIB) women-led firms face a significant investment gap due to lower venture capital and debt access.

The table below highlights key barriers for venture capital funding across North America, Europe, Sub-Sahara Africa, Southeast Asia, South Asia, Latin America and MENA (Middle East and North Africa).

Table 1: Regional comparison of women‑led startup VC funding 2024‑2025 with barriers by continent.

Grant Allocation Disparity in Women Businesses

Grant programs, often perceived as more equitable than private capital, also reflect deep gender bias:

According to OECD women are significantly underrepresented. In some regions, women-led firms receive as little as 10.6% of total grant funding. The African Development Fund notes that less government enterprise disbursementsreach women-owned businesses, largely due to a lack of formal records and collateral required for state-linked funds.

Do Women Entrepreneurs Face Bias in Grant Funding?

The bias against women-led start-ups is structural, cultural, algorithmic, and institutional which requires first to understand its architecture. This is discussed below in 5 pillars of gender bias in startup funding: investor pipeline, banking systems, bias, exclusion and legal gaps.

I. Investor Pipeline Problem: Why Venture Capital Investors Fund More Male Founders

The venture capital industry remains heavily male-dominated, with women holding only 15.4% of partner-level roles in the U.S., approximately 12%-15% in Europe, and just 12% of senior general partner positions in Sub-Saharan Africa.

This lack of diversity at the decision-making level creates significant structural hurdles for female entrepreneurs. Research from Harvard Business School reveals a clear pitching double standard, showing that male entrepreneurs are 60% more likely to succeed in a pitch than women, even when the content is identical.

This disparity is further fueled by psychological biases identified by Columbia Business School, where investors tend to ask men promotion-focused questions about growth and vision while subjecting women to prevention-focused questions about risk and loss. This cycle persists despite evidence of a multiplier effect, which shows that VC firms with at least one female partner are 2 to 3 times more likely to invest in women-led startups (female founders).

II. Why Women Entrepreneurs Struggle to Access Bank Financing

Traditional banking systems were built when women had limited rights, and many of those structures persist today.

Collateral Requirements

In around 75 countries, women lack equal property rights, making collateral impossible (World bank, 2024).

In Africa and South Asia, land titles are often held by male household heads.

Even in developed economies, the wealth gap persists whereby women in the U.S. hold only 32 cents for every dollar men hold. This wealth gap is significantly wider than the income gap and leaves women with far fewer liquid assets to use as collateral for business ventures.

Credit Scoring Bias

Credit scoring models penalize career gaps, part-time work, and lower salaries, all outcomes of inequality, not poor creditworthiness.

AI-driven tools trained on biased data often amplify these patterns.

Risk Perception on Women Led Businesses

A study in Chile focusing on gender discrimination in the consumer credit market reported that loan officers unconsciously assign higher risk scores to identical applications when the applicant is female. In Kenya and Nigeria, experiments showed women-owned businesses received loan offers 18-24% smaller than men with the same financial profile.

III. How Gender Stereotypes Affect Women Entrepreneurs

Gender stereotyping is not loud enough yet powerful in how it influences financing for women founders. Women founders are often described as “too cautious” or “not aggressive enough,” while men with the same traits are praised as visionary. Decisiveness earns men the label “leader” but women “bossy.”

Products targeting women like femtech or maternal health are undervalued, despite women controlling $31.8 trillion in global spending and approximately 85% of all consumer purchasing decisions (NielsenIQ Analysis)

A 2024 VC pitch analysis found femtech companies received valuations 34% lower than male-targeted tech firms at the same stage.

Women are more often asked to prove their ability to scale or balance family responsibilities, creating a prove-it-again tax that drains time and credibility.

IV. Networking Barriers: The Power of Who You Know

Access to capital depends heavily on networks. Alumni circles at elite universities, golf courses, private clubs, and informal groups remain male-dominated. Angel investor networks in the U.S., Europe, and Asia are about 78-85% male, limiting women’s access to early-stage capital. The pattern matching bias, where investors back founders who resemble past successes, further disadvantages women, since most past successes were male.

V. Legal BarriersFacing Women Entrepreneurs Worldwide

Across many jurisdictions, laws and policies still disadvantage women entrepreneurs.

More than 70 countries restrict women’s economic activity compared to men (World Bank, Women Business and the Law Index, 2025).

An estimated 15-18 countries, women need a husband’s permission to open a bank account or register a business.

Inheritance laws block women from inheriting business assets, breaking intergenerational wealth transfer.

Tax systems built around the male breadwinner model penalize women who manage both household and business finances.

Global Differences in Funding for Women Entrepreneurs

The $42 Billion Financing Gap for Women Entrepreneurs in Africa

Africa represents both the greatest challenge and the greatest opportunity in closing the gender financing gap. Women constitute 58% of Africa's informal economy and operate the majority of micro and small enterprises. Yet formal financing remains deeply exclusionary.

Key African Dynamics:

1) The African Development Bank (AfDB) estimates a $42 billion gender financing gap for women-led SMEs in Sub-Saharan Africa.

2) In Sub-Saharan Africa, 52% of women had a financial account in 2024 compared to 64% of men. This gender gap of 12 percentage points is the second largest worldwide after the Middle East and North Africa region.

3) Mobile money innovations, led by M-Pesa in Kenya and similar platforms across the continent, have made partial progress in expanding financial inclusion, but remain insufficient for business-scale financing due to high transaction costs and a lack of integrated long-term credit facilities for SMEs (World Bank, Financial Inclusion in SSA Overview).

4) In West Africa, informal groups like susu (savings) and tontines (rotating credit) remain the dominant financial lifelines for women. Their popularity reflects a systemic failure of formal banks to accommodate the community-based trust and flexible collateral needs of female market traders.

5) Rwanda is a global leader in gender equity, with women owning 55% of individual businesses as of 2025. However, a massive credit gap persists: in early 2025, women-led businesses received only Rwf 164 million out of Rwf 4.6 trillion in total business lending (Ethical Business Africa, Rwanda's Credit Gap).

6) South Africa's startup ecosystem, while more developed, shows the same patterns of a global baseline of 2% in VC funding which it received in 2024.

7) In North Africa, cultural and legal constraints (inheritance laws) add additional layers, with women entrepreneurs in Egypt, Morocco, and Tunisia facing both social stigma and structural financing barriers that views entrepreneurship as a male domain, leading to the world's largest gender gaps in financial inclusion.

Successful African Initiatives Financing Women Led Businesses

There are several African case studies which have played a great role in supporting women led businesses:

1. AFAWA (Affirmative Finance Action for Women in Africa)

The African Development Bank (AfDB) launched AFAWA as its flagship program, targeting $3 billion in financing for women entrepreneurs across the continent. on May 8, 2026, theAfrican Development Bank Groupapproved a $61 million package specifically to boost women-led businesses in Nigeria.This initiative directly addresses the $42 billion gender financing gap for women-led SMEs in Sub-Saharan Africa (AfDB - AFAWA).

2. WeFi (Women Entrepreneurs Finance Initiative)

Led by the World Bank, WeFi initially committed $350 million to support women entrepreneurs globally, with a strong focus on Africa. By leveraging blended finance and partnerships, the program expands access to capital for women-led startup. Its total allocated donor contributions reached $364 million by late 2023.

3. Tony Elumelu Foundation (TEF)

The Tony Elumelu Foundation (TEF) has provided seed capital to over 24,000 African entrepreneurs as of May 2026. The foundation maintains a strong focus on gender equity, with women now making up 46% of its total portfolio, and some recent cohorts reaching as high as 68% female participation.

Through its comprehensive model, participants receive a $5,000 non-refundable grant, intensive business management training, and professional mentorship. This support has enabled women to scale businesses across all 54 African countries.

4. Equity Bank Kenya through Fanikisha & Wings to Fly

Equity Bank’s Fanikisha program has disbursed over KSh 300 billion to women-led businesses, bridging the gender financing gap through a tiered credit system and mentorship. By providing over 2.5 million women with financial literacy training and specialized products, such as KSh 10 million unsecured bid bonds for tender, the program successfully transitions female entrepreneurs from informal savings into the formal banking ecosystem (Equity Bank, Fanikisha Program).

Gender Bias in the U.S. Venture Capital Industry

Silicon Valley is often celebrated as the world’s most advanced startup ecosystem, yet it remains one of the most unequal when it comes to gender. 2025 was a record year for total deal value due to massive AI investments (e.g., Anthropic, Scale AI). However, core disparity exists with PitchBook data indicating that all-female founding teams consistently receive about 2% to 2.3% of total U.S. venture capital, a figure that has fluctuated by only decimal points for a decade.

The #MeToo Movement and Culture: The #MeToo movement exposed deep-seated harassment and exclusion of women in VC circles. Forbes and NVCA reports in 2025/2026 note that while awareness has increased, women still face systemic barriers, including a lack of representation in decision-making roles (only an estimated 15.4% of investment partners are women).

Intersectionality (Black and Latina Founders): The gap in funding is most severe for women of color. 2025 data shows that Black founders received only 0.4% of all U.S. startup funding in 2024, with Black and Latina women receiving only a tiny fraction of that sub-total.

Policy and Reporting Requirements: California (via SB 54) became the first state to mandate that VC firms report the diversity of the founders they fund. New York and Massachusetts have explored similar legislation to increase transparency, with early data from 2024 suggesting these laws are beginning to drive modest shifts in firm behavior.

Figure 3: Funding to US startups with black founders from 2020 to 2025.

Why Europe Still Has a Gender Gap in Startup Funding

Venture Capital Funding Gap: Confirmed. While 2025 saw a slight rise in total deal value for female founders, their share of overall dealmaking continues to slide. According to PitchBook, startups founded solely by women raised approximately 1.5% to 2% of European venture capital in 2024 mirroring the 2% VC global baseline for women businesses.

The European Investment Fund (EIF) has attempted to address this imbalance through its Gender Smart Finance initiative. By early 2025, the EIB Group reached a milestone of €100 billion in new financing initiatives, with a significant portion of higher-risk equity activities directed toward mandates that include gender-smart criteria.

The UK Government's Rose Review in 2024 found that women-led businesses contribute over £250 billion annually to the UK economy. Despite this, female founders secured only 1.9% to 2.3% of total UK venture capital investment in that year aligning with the global pattern of 2%.

Even in the Nordic countries such as Sweden and Finland which are seen as global leaders in gender equality, significant startup funding gaps persist. This suggests that general equity policies alone are insufficient without targeted financial interventions (European Investment Bank, 2025).

The European Commission has integrated gender equality as a core priority for 2024-2029, including provisions for women's entrepreneurship under its Union of Equality framework. However, implementation varies significantly, with women-led deep tech ventures in Eastern Europe capturing as little as 3.6% of regional funding compared to better performance in Central Europe.

Figure 4: European VC funding comparison showing Finland and Central Europe leading female founder investment.

Funding Challenges Facing Women Entrepreneurs Across Asia

Asia’s diversity means gender financing gaps manifest differently across subregions.

a. South Asia

Women entrepreneurs across South Asia face a number of structural and financial barriers, with India having around $158 billion financing gap. While India’s tech ecosystem shows signs of progress, with women-led startups securing approximately 8.8% to 11.6% of total capital ($1.1 billion) in 2025, the broader landscape remains excluded. Bangladesh has a world-leading microfinance access.

However, financing gap persists where women-led SMEs receive less than 5% of total bank credit, struggling to transition from microloans to formal growth capital. Meanwhile, Pakistan remains one of the world's most restrictive environments due to socio-cultural constraints, with women founders capturing just 1.4% of total venture capital. Across the region, the primary themes are a lack of formal collateral, high interest rates, and a systemic rejection by design in traditional banking.

b. Southeast Asia

Singapore and Vietnam have relatively stronger performers in women-led venture capital share compare to their peers in the region. Vietnam is a regional standout, with women owning approximately 26.5% of businesses.

Despite women leading nearly two-thirds of MSMEs in Indonesia, exceeding global average, they receive a disproportionately small share of formal startup funding. These numbers sit squarely at the 2% baseline that runs through every region examined in this report. This confirms that indeed Asia is not an exception to global disparity in financing women led businesses.

c. East Asia

Women’s entrepreneurship in East Asia is defined by deep structural disparities, with Japan trailing the G7 with only 13-14% of entrepreneurs being women due to a conservative corporate culture in the country. While China maintains high female labor participation, its competitive ecosystem suffers from limited data transparency regarding gender-specific financing gaps and executive representation.

On the other hand, South Korea is making significant strides through targeted government initiatives, such as its 2025-2029 Basic Plan, which provides high-tech grants of up to 80 million KRW to scale women-led ventures in fields like AI and FemTech.

Why Women Entrepreneurs in Latin America Struggle to Access Formal Financing

Latin America is faced with an informal dynamic scenario facing women entrepreneurs.

a. Entrepreneurial Dynamism vs. Funding Gap: Latin America and the Caribbean (LAC) is one of the most entrepreneurial regions globally for women, with nearly 49% of women starting their own businesses as of 2025. However, a massive credit gap of approximately $93 billion to $98 billion persists for women-owned SMEs in the region.

b. Business Ownership vs. VC Allocation: While women-led businesses represent a significant portion of the economy, owning roughly one-third of MSMEs and showing a business ownership rate of 29.5% to 38% in high-activity countries, they receive a tiny fraction of formal venture capital.

Reports from IDB Lab's wX Insights (2024/2025) highlight that while women-led STEM startups are raising more capital, the gap remains wide, with regional VC funding for all-female teams often not breaking from the 2% global trend.

c.Brazil’s Startup Ecosystem: As the largest economy in the region, Brazil reflects global exclusion patterns. In 2024, only 19% of startup founders in Brazil were women. While the National Strategy for Female Entrepreneurship (Elas Empreendem) was launched to improve access to finance and markets, cultural factors and a "machista" attitude continue to hinder formal growth.

d. IDB Gender-Lens Programs: The Inter-American Development Bank (IDB) has launched major initiatives like WeForLAC and gender-focused social bonds to expand credit for women-led businesses. Despite helping over 1.4 million women-led MSMEs access credit between 2016 and 2024, implementation gaps persist, particularly in the "missing middle" where some businesses are too large for microfinance but too small for traditional commercial banking.

e. Fintechs targeting women in Mexico, Colombia, and Brazil represent a promising structural shift. Yet cultural factors, including machismo and family responsibility norms, remain powerful barriers to women’s full participation.

Women Entrepreneurs in the Middle East and North Africa Face the World’s Largest Funding Gaps

The Union for the Mediterranean (UfM) identifies a big gender gap in the MENA financial sector, where women own only 5% to 14% of SMEs, the lowest rate worldwide outside South Asia. While a global credit gap for women-owned SMEs is estimated at $1.7 trillion, the MENA region's share remains a significant multi-billion dollar hurdle.

The World Economic Forum highlights a dramatic contrast between education and capital access: women constitute over 50% to 70% of STEM graduates in countries like Iran, Oman, and Saudi Arabia, significantly outpacing the U.S. (where women account for only an estimated 35% of STEM graduates).

For Startups founded solely by women in the MENA region, they received only 1.2% of regional venture capital in 2024-2025. While this is a modest improvement from the 0.47% recorded in 2023, it remains among the lowest figures globally. Data for the first half of 2025 indicates that Saudi Arabia and the UAE continue to dominate regional funding.

By late 2025, Saudi Arabia secured the lead with $3.2 billion in funding (representing over 40% of the regional total), while markets like Egypt saw significantly lower figures (est. $22.3 million) and Iraq trailed with minimal formal VC activity.

Saudi Arabia’s Vision 2030 has driven a transformative shift in women’s economic participation, with the female labor force participation rate rising from 17% in 2017 to 36.3% in Q1 2025, significantly exceeding the original 30% target. This progress is underscored by the female unemployment rate dropping to a historic low of 10.5% during the same period.

The country has modernized its labor laws to support diverse employment models, resulting in over 240,000 flexible work contracts for women by Q3 2025 and over 280,000 women benefiting from remote work initiatives. Furthermore, women have emerged as a dominant force in the independent economy, accounting for nearly 50% of self-employment activity with 690,000 active independents, while women-led enterprises now represent approximately 44% of all total enterprises in the country.

Yet despite these labor market gains, startup funding gaps persist. The UAE and Israel stand out as regional powerhouses with more developed women-focused financing ecosystems. Legal reforms are progressing but uneven. Countries such as Jordan, Morocco, and Tunisia lead on regulatory change, while others lag behind (OECD, 2020).

The Business Case: Why Funding Women Is Good Business

Funding women businesses can be noted as a positive decision highlighting women businesses tend to outperform their male peers in returns.

Figure 5: Comparative chart showing women‑led companies outperforming male‑led firms in ROI and innovation.

Key observations on women vs male led businesses

Capital Efficiency: For every dollar invested, women-led startup generate more revenue than those led by men.

Long-term Value: Over a 10-year horizon, female-founded companies create more value (ROI) for investors.

Asset Management: Companies with gender-balanced leadership achieve a higher Return on Assets, outperforming all-male teams.

Innovation Velocity: Women-led firms are more likely to introduce innovative products to the market.

The Economic Impact of Closing the Gender Funding Gap

Supporting women businesses could result in several macroeconomic benefit. Achieving gender parity in entrepreneurship represents a massive macroeconomic opportunity, with the McKinsey Global Institute estimating that closing the gap could add $12 trillion to global GDP. In a full potential scenario where women participate in the economy identically to men, this gain could reach as high as $28 trillion.

The impact is particularly profound in Africa, where the World Bank and IMF project that gender parity could unlock an estimated $300 billion in GDP by 2030, equivalent to a 10% boost to the continent's collective economy. This "parity dividend" is now a core focus for global financial institutions, who view the removal of barriers for women entrepreneurs as a primary driver for sustainable global growth.

Figure 6: Economic projection of $28T global GDP unlock and $300B Africa dividend from women entrepreneurs.

Beyond macroeconomic growth, women entrepreneurs generate stronger community-level impacts. Studies show that women reinvest 90 cents of every dollar earned back into their families and communities, comparedto 30-40 cents for men ((UN Women, 2025). This multiplier effect strengthens education, health, and local job creation.

At the firm level, gender diversity also drives innovation. Research by the Boston Consulting Group found that gender-diverse founding teams generate 19% higher innovation revenue compared to less diverse teams.

How Governments and Investors Can Close the Gender Funding Gap

A comprehensive response to bridging the gap in financing of women led businesses requires action at multiple levels simultaneously, from individual behavior change to institutional reform to policy transformation.

Figure 7: A representation of five pillars dismantling gender barriers in startup financing with $0.90 social value per $1 invested.

Pillar 1: Policy and Regulatory Needed to Support Women Entrepreneurs

National Government Actions:

Immediate Impact

Grant Allocation: Mandating a 30% minimum for women-led ventures in public grants.

Reporting Requirements: Requiring gender-disaggregated (banks, venture capital firms, and government agencies must break down their financial reporting by sex (male vs. female) rather than presenting one single neutral number) data to identify exactly where capital is stalling.

Short-Term (1-2 Years)

Credit Policy: Reforming collateral laws to accept moveable assets (like inventory or equipment) instead of just land.

Procurement: Implementing equity targets to give women-owned businesses a fair share of government contracts.

Medium-to-Long-Term (2-5 Years)

Tax Policy: Using incentives to encourage private investors to move capital into women-led startups.

Property Rights: Enacting and enforcing gender-neutral inheritance and land laws to secure women’s foundational wealth.

Figure 8: A strategic policy roadmap chart showing policies for national governments for advancing women’s financial inclusion.

Multilateral and Regional Actions:

The G20 should adopt binding gender equity targets for national development finance institutions.

The African Union should accelerate implementation of the Maputo Protocol provisions on women's economic rights across African countries.

The World Trade Organization (WTO) should integrate gender equity requirements into trade finance frameworks.

ASEAN should create a regional women's entrepreneurship financing facility modeled on AfDB's AFAWA.

Pillar 2: Financial Sector Transformation

This pillar represents the policies to be implemented in the financial sector to support financing for women led businesses.

Banking Reform:

Replace traditional collateral requirements such as land with cash flow-based lending for women entrepreneurs.

Adopt gender-neutral credit scoring methodologies that do not penalize career gaps or caregiving histories.

Establish dedicated women's enterprise banking units within major commercial banks.

Implement gender audits of loan approval processes and publish results publicly.

Expand guarantee schemes that de-risk lending to women entrepreneurs, modeled on successful programs in India, Kenya, and Colombia.

Venture Capital Reform:

Establish gender diversity requirements for VC firms receiving institutional capital from pension funds, sovereign wealth funds, and development finance institutions.

Create gender-lens investing mandates, allocating a defined percentage of investment capital to women-led ventures.

Build women-only VC funds to address the pipeline gap while systemic change occurs.

Reform pitch process design to reduce pattern-matching bias such as blind pitches, standardized question protocols, and diverse evaluation panels.

Create transparent deal-flow data to enable tracking of gender bias in investment decisions.

Blended Finance Innovations:

Expand first-loss guarantee mechanisms that reduce perceived risk of investing in women-led startups.

Create revenue-based financing products that do not require the equity dilution often more painful for women founders with smaller initial stakes.

Develop pay-it-forward financing models where successful women entrepreneurs fund the next generation.

Scale Islamic finance products compatible with gender equity principles across Muslim-majority markets.

Pillar 3: Ecosystem and Network Building

This pillar consists of accelerators and incubators, mentorship and sponsorship, and network accces reform.

Accelerators and Incubators:

The proliferation of women-focused accelerators represents one of the most promising developments in closing the financing gap. Key programs and their models:

Figure 9: Global and regional programs supporting women entrepreneurs with scale of impact.

Key programs and their modelsSummary

Structural Bias Mitigation

Founder Institute: Implements a unique gender-blind evaluation model for its pre-seed program to ensure applicants are judged solely on merit and potential.

Y Combinator: Continues to serve as a major global pipeline, achieving 27% female representation in its recent high-growth cohorts.

Direct Capital & Training

Cartier Women's Initiative:It provides high-impact $100,000 grants to 30 laureates annually, paired with world-class mentorship.

Women's Startup Lab:Focuses on funding readiness, with 75% of its founders successfully raising capital within a year.

Network Scale

Lionesses of Africa: Supports a vast Pan-African network of 2 million plus women, facilitating essential market access.

She Leads Africa and Vital Voices: Combined, they support over 50,000 entrepreneurs and leaders through connections and specialized investment readiness programs.

Mentorship and Sponsorship:

Research consistently shows that women entrepreneurs with mentors raise more capital than those without.

Formal sponsorship programs, where senior investors actively advocate for women founders, outperform mentorship alone.

Corporate-startup mentorship bridges (connecting women founders with senior female executives in large companies) have shown strong results in the U.S. and UK.

Peer networks among women founders share investor intelligence, negotiation strategies, and due diligence insights thus providing collective power.

Network Access Reform:

Major VC conferences should adopt gender equity attendance and speaking requirements.

Angel investor networks should actively recruit women members as research shows that women angels are 2.3x more likely to fund women founders.

Universities should create gender-inclusive alumni entrepreneurship networks connecting women graduates with funding opportunities.

Digital platforms for investment networking should implement anti-bias design principles.

Pillar 4: Capacity Building and Financial Literacy

This pillar focuses on investment readiness and financial literacy for women-led businesses.

Investment Readiness:

A genuine structural challenge, clear but related to discrimination, is that many women entrepreneurs lack exposure to the language, norms, and expectations of formal investment processes. Addressing this requires:

Pitch training programs specifically designed for women, addressing the double standard in investor questioning.

Financial modeling workshops ensuring women founders can present sophisticated financial projections.

Term sheet literacy programs such as understanding equity, valuation, dilution, and investor rights.

Legal support for navigating investment agreements and intellectual property protection.

Financial Literacy at Scale:

Mobile-based financial literacy programs have shown effectiveness in reaching women in developing markets.

Radio and community-based programs in rural Africa and Asia can reach women entrepreneurs outside formal education systems.

Peer learning models where women teaching women in trusted community settings, outperform formal classroom approaches in many scenarios.

Curriculum integration in schools and universities, ensuring the next generation of women entrepreneurs enters the ecosystem better prepared.

Pillar 5: Data, Transparency, and Accountability

The Measurement Gap:

One of the most significant enablers of gender discrimination in financing is the absence of systematic, publicly available data on funding allocation by founder gender. Without measurement, accountability is impossible.

Recommended Data Infrastructure:

a) Mandatory gender-disaggregated reporting for all regulated financial institutions i.e. banks, VC funds, private equity firms, and grant-making bodies.

b) Public dashboards allowing real-time tracking of gender funding allocation.

c) Standardized gender metrics across international financial reporting frameworks (GRI, SASB, TCFD equivalent for gender).

d) Independent auditing of gender equity claims by financial institutions.

e) Research investment in understanding intersectional barriers faced by women from different racial, ethnic, and socioeconomic backgrounds.

What Works for Women-Led Startups

There are several approaches which have been adopted in different countries indicating what works for women led startups.

Case Study 1: Rwanda - Policy-Driven Transformation

Rwanda offers one of the world's most instructive examples of how deliberate policy can reshape gender dynamics in entrepreneurship. Following the genocide, Rwanda embedded gender equity in its constitutional framework and economic policy. Results include:

Women constitute around 64% of Rwanda's parliament, the highest in the world and own 55% of registered individual businesses in Rwanda.

Women-owned businesses access formal credit at near-parity with men, unusual for Sub-Saharan Africa

BPR Bank Rwanda's Women Banking Unit offers tailored products including lower collateral requirements and business development support

Rwanda's Gender Monitoring Office tracks economic participation data and holds institutions accountable

Key lesson: Top-down political commitment, combined with institutional accountability and tailored financial products, can drive measurable change within a decade

Case Study 2: India - Microfinance to Mainstream

India's microfinance revolution, pioneered by institutions like SEWA Bank, Mann Deshi Foundation, and Grameen replicas, has demonstrated that women are exceptionally reliable borrowers. Key outcomes include:

SEWA Bank's portfolio of 400,000 plus women borrowers maintains a repayment rate exceeding 97%.

Mann Deshi has disbursed over $1 billion in loans to rural women entrepreneurs with minimal default.

The Mudra Yojana scheme has disbursed $180 billion in loans, with 68% going to women borrowers since its inception.

Yet the problem persists, women who succeed at the micro level struggle to access growth capital, highlighting the middle-market financing gap.

Key lesson: Demonstrated creditworthiness at scale has not automatically opened doors to larger capital, targeted interventions at each stage of the financing ladder are essential.

Case Study 3: United States - The Arlan Hamilton Effect

Arlan Hamilton, founder of Backstage Capital, built a $36 million fund focused exclusively on investing in underrepresented founders such as women and people of color entrepreneurs, while homeless. Her story and success demonstrate:

Underrepresented founders represent an arbitrage opportunity; they are overlooked by mainstream VC, creating less competition for deals.

Backstage Capital portfolio companies have raised over $1 billion in follow-on funding from other investors.

Hamilton's approach has inspired a wave of diversity-focused funds that are collectively beginning to shift the capital allocation landscape.

Key lesson: Underrepresented founders are a high-value market arbitrage opportunity. By identifying and funding the underestimated talent that traditional venture capital overlooks, investors can unlock significant capital efficiency and outsized returns.

Case Study 4: Netherlands - Gender-Smart Public Procurement

The Dutch government's initiative to track and promote gender equity in enterprise support programs offers a model for public sector leadership:

The Netherlands Enterprise Agency (RVO) now reports gender-disaggregated data on all business development grants.

Introduction of gender-neutral language in grant application forms increased women's application rates.

Quota-adjusted evaluation panels with mandatory female representation reduced gender gap in grant awards.

Key lesson: Process reform in public grant-making can rapidly shift outcomes without requiring new legislation.

Case Study 5: Kenya - Fanikisha SME program

Equity Bank's targeted women's banking initiative in Kenya demonstrates the commercial viability of gender-focused financial products:

Women customers now constitute about 40% of Equity Bank's customer base.

Women's business loans show default rates lower than the overall portfolio.

The bank's Fanikisha SME program for women entrepreneurs has disbursed over KES 200 billion, resulting in the bank being independently recognized as the "Most Loved Banking Brand by Kenyan Women" three years in a row.

Mobile banking integration has reduced barriers of physical access that disproportionately affected women.

Key lesson: Gender-smart banking is commercially sustainable and generates positive social externalities simultaneously.

Emerging Innovations: Technology as a Force for Equity in Gender Financing Gap

Technology presents both risks (algorithmic bias) and opportunities (financial inclusion) in closing the gender financing gap.

Can AI Reduce Gender Bias in Business Lending?

Emerging fintech companies are reshaping credit assessment by moving beyond traditional, often biased, metrics. Instead of relying solely on collateral or conventional credit histories, these firms use non-traditional data sources such as mobile phone usage, utility payment records, social networks, and behavioral patterns to evaluate creditworthiness. This approach has proven particularly valuable in regions where women are excluded from formal banking systems.

Platforms like Tala, Branch, and FairMoney, operating across Africa and Asia, have demonstrated that alternative data can predict repayment behavior more accurately than traditional credit scores. By leveraging mobile-first ecosystems, they are serving previously unbanked populations, especially women, who were historically denied access to growth capital.

However, this innovation carries a critical risk. AI systems trained on historical data can replicate and even amplify existing biases if not deliberately designed with fairness in mind. Without active algorithmic bias testing and fairness safeguards, these tools risk reinforcing the very inequalities they aim to solve. Ensuring transparency, accountability, and inclusive design in AI-driven credit scoring is therefore essential to unlocking its full potential for women entrepreneurs.

How Blockchain and DeFi Could Expand Financing for Women Entrepreneurs

Blockchain and decentralized finance (DeFi) are opening new pathways for women’s economic empowerment by addressing structural barriers in asset ownership and access to capital. In places where formal land rights remain contested, blockchain-based property registries can establish verifiable ownership records for women, creating new collateral options that were previously unavailable. This innovation has the potential to unlock credit markets for women entrepreneurs who have historically been excluded due to discriminatory property laws.

At the same time, DeFi lending protocols offer permissionless access to capital, bypassing traditional financial gatekeepers. By removing intermediaries, these platforms can democratize funding opportunities for women entrepreneurs, especially in regions where banking systems remain biased or inaccessible.

Complementing this, smart contract-based guarantee schemes can reduce the administrative costs of credit guarantees, making them viable even at smaller loan sizes. This is particularly important for women-led SMEs, which often seek modest financing but face disproportionate barriers in securing it.

Together, blockchain and DeFi present a transformative opportunity: they not only challenge entrenched financial exclusion but also create scalable, transparent, and cost-effective mechanisms that can expand women’s participation in formal entrepreneurship.

Digital Platforms and Community Finance

Digital platforms are reshaping access to capital for women entrepreneurs by bypassing traditional gatekeepers and formalizing community finance. Crowdfunding platforms, particularly equity crowdfunding, have shown higher female founder participation rates compared to traditional venture capital. Platforms like iFundWomen demonstrate that women raise more on gender-inclusive platforms, highlighting the importance of inclusive design in digital finance ecosystems.

In Africa, digital susu and chama platforms are formalizing traditional community savings groups, creating credit histories and pooled financing opportunities for women entrepreneurs. By digitizing these long-standing practices, women gain access to structured financial records that can be leveraged for future credit, bridging the gap between informal and formal finance.

Meanwhile, in Asia, social commerce platforms such as TikTok Shop, Shopee, Lazada, and social messaging ecosystems like WeChat and WhatsApp Businessare enabling women entrepreneurs to build businesses with minimal startup capital.

These platforms allow women to monetize networks and digital marketplaces, often with little upfront investment. However, while they provide entry points into entrepreneurship, the challenge of accessing formal growth financing remains unresolved, limiting scalability.

Together, these innovations point to how digital platforms, and community finance can expand women’s economic participation, while also underscoring the need for structural reforms to ensure that early-stage gains translate into long-term growth opportunities.

What Must Happen by 2030 to Improve Funding for Women Entrepreneurs

For the gender financing gap to be substantively closed by 2030, the following milestones must be achieved shown in the following charts below:

Figure 10: A comparison of women’s financial inclusion baseline vs 2030 goals worldwide.

Priority Actions for the Next 24 Months

Immediate (0-6 months):

a) Adopt mandatory gender-disaggregated reporting requirements in all G20 jurisdictions.

b) Launch emergency technical assistance for women-focused fintech platforms.

c) Establish cross-institutional working group on AI bias in credit scoring.

Short-term (6-18 months):

a) Scale guarantee schemes for women entrepreneurs across Sub-Saharan Africa and South Asia.

b) Reform public grant application processes to reduce implicit bias.

c) Launch industry-wide VC gender equity pledge with binding accountability mechanisms.

Medium-term (18-36 months):

a) Harmonize gender equity requirements across multilateral development bank lending frameworks.

b) Expand women-focused accelerator programs to tier-2 and tier-3 cities in developing markets.

c) Establish international gender financing data standard for cross-border comparability.

Figure 11: Africa’s women SME credit gap shrinking from $42B in 2024 to zero by 2030.

The Future of Women Entrepreneurs and Global Economic Growth

The systematic discrimination against women-led start-ups in accessing grants, loans, and equity investment is among the most consequential and correctable failures in the global economy. It is not a problem unique to any region, culture, or development stage. It manifests itself in various parts of the world.

The barriers are real which have been embedded in law, banking practice, investor culture, and social norms. But they are not immutable. Rwanda has shown that political commitment can reshape access to capital in a decade.

India's microfinance sector has proven that women are among the world's most creditworthy borrowers. Arlan Hamilton has demonstrated that overlooked founders generate great returns on investments. Kenya's Equity Bank has shown that gender-smart banking is commercially sustainable.

The report shows that women-led companies not only deliver a broader social impact but also an underexploited reservoir of innovation and economic growth. Every dollar denied to a qualified woman entrepreneur is not just an injustice, but a measurable, quantifiable economic loss absorbed by investors, communities, and nations.

The choice before investors, policymakers, financial institutions, and society is clear: continue the status quo and forfeit the returns that gender equity generates or remove the barriers and unlock a new era of inclusive economic growth.

Frequently Asked Questions

1. Why do women entrepreneurs receive less funding?

Women founders face investor bias, weaker access to networks, collateral barriers, and underrepresentation in venture capital decision-making.

2. How much venture capital goes to women-led startups?

As detailed throughout this report, women‑only founding teams consistently receive roughly 2% of venture capital across major markets.

3. Do women-led startups perform well?

Many studies suggest women-led startups often show strong capital efficiency, resilience, and competitive long-term returns.

4. What is the financing gap for women entrepreneurs?

It is the difference between the funding women-owned businesses need and the financing they can access through formal systems.

5. Why does closing the gender funding gap matter?

Closing the gap could boost innovation, job creation, financial inclusion, and global economic growth.

IShowSpeed's African Tour and the New Era of Influencer Diplomacy

Darren Jason Watkins Jr., better known as “IShowSpeed”, is an American YouTuber and livestreaming sensation. His high-energy, unpredictable content blends...

From M-Pesa to fintech regulation, Kenya’s step-by-step approach to digital finance offers lessons for policymakers, investors, and emerging markets worldwide.

Kenya’s digital finance ecosystem is widely regarded as the most...

What Is Driving Africa’s 2026 Risk Outlook?

Executive Summary

Africa’s 2026 growth and risk landscape is being reshaped by high-stakes agreements and regional macro developments. The Washington Accords between the...

China’s engagement in Africa has expanded dramatically over the past two decades, reshaping economies, trade patterns, and political alliances. As China becomes Africa’s largest trading partner, biggest bilateral lender, and...