Symbolic display of Australia and U.S. diplomatic unity featuring national flags and mineral specimens representing shared natural heritage and international cooperation.

Australia’s Rare Earth Strategy: A Plan To Break China's Grip On Tech And Defense

Australia’s rare earth metals have emerged as pivotal assets in the global contest for technological supremacy and supply chain resilience. As geopolitical tensions deepen between the United States and China, these critical minerals, vital for semiconductors, electric vehicles (EVs), and advanced defense systems, have become more than commodities. They now function as strategic levers shaping industrial policy, defense readiness, and global influence.

Historical Context: From Discovery to Strategic Asset in Global Supply Chains

Australia’s rare earth journey began with the discovery of Mount Weld deposits in Western Australia during the 1980s. Commercial development accelerated in the early 2000s, driven by Lynas Rare Earths Ltd., now one of the world’s few non-Chinese producers.

This evolution transformed Australia from a resource-rich nation into a strategic player in global critical minerals supply chains.

Why Rare Earth Elements (REEs) Matter for the Future Economy

Rare earth elements (REEs) such as neodymium, dysprosium, and terbium possess unique magnetic and conductive properties. They are indispensable in manufacturing smartphones, wind turbines, electric motors, and precision-guided missiles.

According to the International Energy Agency (IEA), demand for rare earths used in clean energy technologies could grow by up to 700% by 2040, making control over these materials a defining factor in the next industrial revolution (IEA Report).

China’s Rare Earth Dominance: Control Over the Global Value Chain

China controls roughly 70% of global rare earth mining and nearly 90% of global processing capacity (ABC News). Its dominance stems from aggressive subsidies, environmental leniency, and vertical integration across the full value chain.

A case in point is BYD, which received RMB 30.88 billion in R&D support, enabling it to lead in EV manufacturing and clean energy systems, underpinned by access to rare earth materials.

Global Struggles to Reduce Reliance on China

Attempts by the U.S., European Union, and Japan to diversify away from China’s rare earth supply have largely faltered due to high production costs, policy delays, and limited refining infrastructure (DW, SCMP, TIME).

This dependence underscores the urgency for countries like Australia to expand local processing capacity and value-added production.

Australia’s Strategic Response: U.S. Partnership and Domestic Policy Reform

In October 2025, Australia and the U.S. signed a $13-billion critical minerals pact, with each nation committing $1 billion to joint investments.

Australia’s environmental, social, and governance (ESG) standards are among the strongest globally (Corrs Chambers Westgarth), surpassing Southeast Asia’s emerging frameworks (ESGPedia).

Innovations such as Minespider’s Digital Product Passports are improving traceability, reinforcing Australia’s image as a trusted, sustainable rare earth supplier.

ESG Leadership in Asia: Australia’s Sustainability Edge Australia’s ESG leadership is a strategic differentiator. The graph below compares ESG scores across leading Asian economies.

Line graph comparing ESG scores across Asian countries in 2025, highlighting Australia’s leadership over Japan, South Korea, Singapore, India, Indonesia, and Thailand

Key Insights from the Graph

Australia leads Asia with an ESG score of 82, ahead of Japan (78), South Korea (74), and Singapore (70).

India, Indonesia, and Thailand lag behind, reflecting gaps in governance and environmental enforcement.

Australia’s ESG advantage enhances its credibility as a supplier of ethically sourced rare earths, aligning with Western partners’ priorities for sustainable materials and transparent supply chains.

Talent and Expertise: Comparing Australia, China, and Global Leaders

China maintains a commanding lead in rare earth processing expertise, built over decades of industrial development.

Australia is investing in research institutions such as CSIRO and the University of Adelaide, but scale and specialization remain challenges. Meanwhile, Japan, Germany, and the U.S. continue to lead in magnet production and advanced metallurgical innovation.

Industrial Policy Pathway: Tax Incentives and Long-Term Investment

Australia’s Critical Minerals Production Tax Incentive provides a 10% tax credit and $22.7 billion in long-term support (AusIMM), encouraging domestic refining and magnet manufacturing.

This industrial policy forms the backbone of Australia’s bid to reduce dependence on Chinese processing facilities.

Strategic Implications: Building a Competitive Rare Earths Ecosystem

Capital investment alone won’t secure Australia’s leadership. To remain competitive, Australia must:

Reform university curricula to develop specialized rare earth engineers.

Expand domestic refining and magnet manufacturing capacity.

Deepen alliances with the U.S., Japan, India, and Canada for joint R&D and technology transfer.

Pursue selective cooperation with China for technical know-how while safeguarding strategic autonomy.

Africa’s Rising Role in the Rare Earth Market

Africa is emerging as a future supplier of critical minerals. Kenya’s Critical Mineral Catalogue lists REEs among nine priority resources. South Africa and the Democratic Republic of Congo also possess significant deposits.

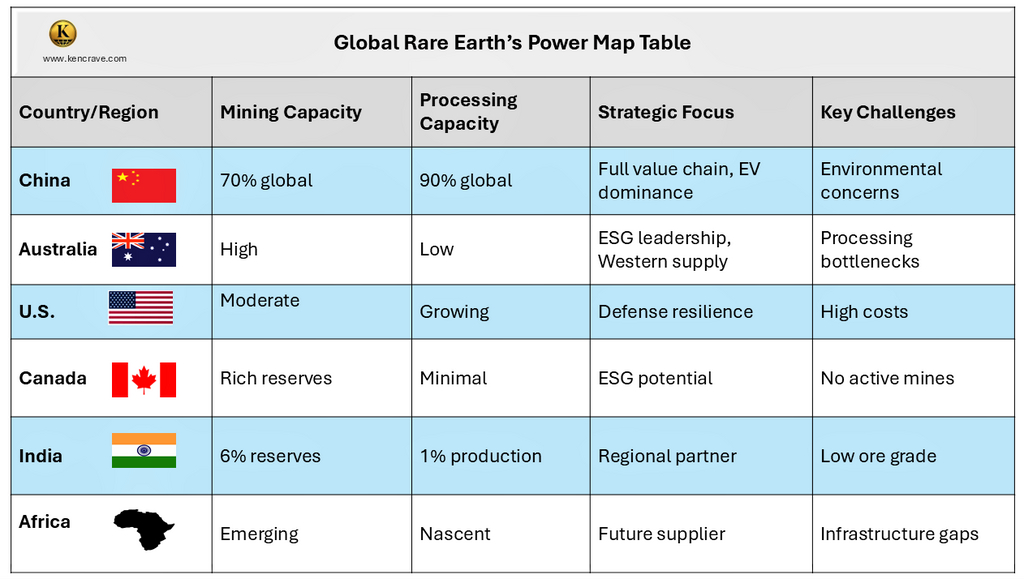

Global rare earth power map comparing mining, processing, strategy, and challenges across China, Australia, U.S., Canada, India, and Africa

According to Brookings, Africa could supply 10% of global rare earth demand by 2029, although infrastructure and transparency challenges persist.

Key Takeaways: The Future of Australia’s Rare Earths Strategy

Australia and the U.S. signed a $13B critical minerals pact (2025).

China maintains 90% control over global rare earth processing.

Australia’s ESG standards surpass those of Southeast Asia.

Education reform and industrial policy are essential for Australia’s long-term success.

The Road Ahead: Securing Australia’s Leadership in the Global Rare Earths Race

To cement its position as a global rare earths powerhouse, Australia should pursue a multi-pronged strategy balancing economic growth with geopolitical foresight:

Expand Domestic Processing Capacity – Reduce reliance on China through refining and magnet production.

Reform Education and Talent Pipelines – Train engineers in metallurgy, chemistry, and mineral purification.

Strengthen Strategic Alliances – Partner with the U.S., Japan, India, and Canada for technology exchange.

Engage China Pragmatically – Collaborate selectively to accelerate technical know-how.

Implement Robust Industrial Policies – Use tax credits, joint ventures, and R&D grants to de-risk investments.

Maintain ESG and Traceability Leadership – Promote transparency in mining and processing operations.

Collaborate with Africa – Build ethical, sustainable supply chains across Kenya, South Africa, and Congo.

Australia’s Opportunity in the Next Global Mineral Revolution

Australia stands at the center of the critical minerals transformation reshaping global technology, energy, and defense.

By combining policy foresight, industrial innovation, and ESG leadership, Australia can emerge as the world’s trusted supplier of rare earths, a strategic pillar in both the green energy transition and global security landscape.

Australia has been experiencing a housing crisis. The housing crisis didn’t happen overnight. For decades Australia has not built enough homes to match growth in population and households. This persistent...