A Futuristic Asian cityscape with digital overlays, viewed by silhouetted figures, under the title 'Asia 2030 Investment Playbook. Image Credits: Alex via Pexels/Ai/Financials Hub

Asia 2030: Your $30 Trillion Investment Playbook, Where To Invest & What To Avoid

Asia continues to solidify its position as the world's economic growth engine, offering unparalleled opportunities amid rapid digital transformation and shifting global supply chains. By 2030, the region will contribute over 60% of global GDP growth(Asian Development Bank, World Economic Forum), representing a $30 trillion economic opportunity, but success requires navigating complex regulations, cultural nuances, and fierce local competition.

Why Asia Remains the World's Growth Hotspot

1. The Digital Revolution: Asia at the Center of Tech Innovation

China and India lead in AI adoption (45% of global fintech unicorns are Asian). Southeast Asia's (SEA) digital economy to hit $1 trillion by 2030 (WEF).

2. Middle Class Boom: Consumer Power

Asia will house 66% of the global middle class by 2030 (Statista,McKinsey)

E-commerce penetration jumps from 25% (2020) to 45% (2025) in Southeast Asia (Intelliwings).

“India’s consumption economy is expected to be the third largest globally by 2030, reaching approximately $5 trillion, with 75 per cent of consumption being led by the middle-income segment,’’ says Kalyan Krishnamurthy, CEO of the e-commerce giant Flipkart Group

Strategic Manufacturing Shifts: The China+1 Momentum

Vietnam exports grew 17% YoY as companies diversify from China

India’s Production-Linked Incentive (PLI) scheme attracts $26B in electronics manufacturing.

Asia's economic dominance is entering a transformative phase. With 40% of global tech startups now Asian-born (CB Insights 2024) and 75% of the world's semiconductors produced in the region, understanding these markets has never been more critical. This analysis incorporates exclusive projections to guide your strategic planning.

Asia's 2025 Economic Power Matrix: Growth, Foreign Direct Investment (FDI), and Tech Talent

A piechart indicating Asia GDP composition in 2025

Asia Market Projections to Watch- 2025

Source: IMF, World Bank, BCG, Goldman Sachs and McKinsey 2025 Outlook Reports

Strategic Notes:

Philippines continues to lead in BPO and voice-based services, with rising momentum in AI-enabled customer solutions and healthcare outsourcing.

Thailand is positioning itself as a regional hub for smart factories, EV production, and industrial robotics, backed by its “Thailand 4.0” initiative.

Malaysia is a key node in Islamic fintech innovation, digital banking, and Halal tech, supported by a robust regulatory framework and regional connectivity.

Key Takeaways for Investors: Where and Why to Bet in Asia

1.Growth Champions:

Vietnam and India will outpace regional averages (6.5%+ GDP growth)

"Vietnam's semiconductor ecosystem is attracting 40% of new electronics FDI" BCG 2024 Tech Report

2. Talent Hotspots:

China produces 60% of Asia's STEM graduates. Chinese universities now output more PhDs in STEM than U.S. institutions, further underscoring China’s lead (fdiintelligence).

Geopolitical Risks Flash-points That Could Derail Investment

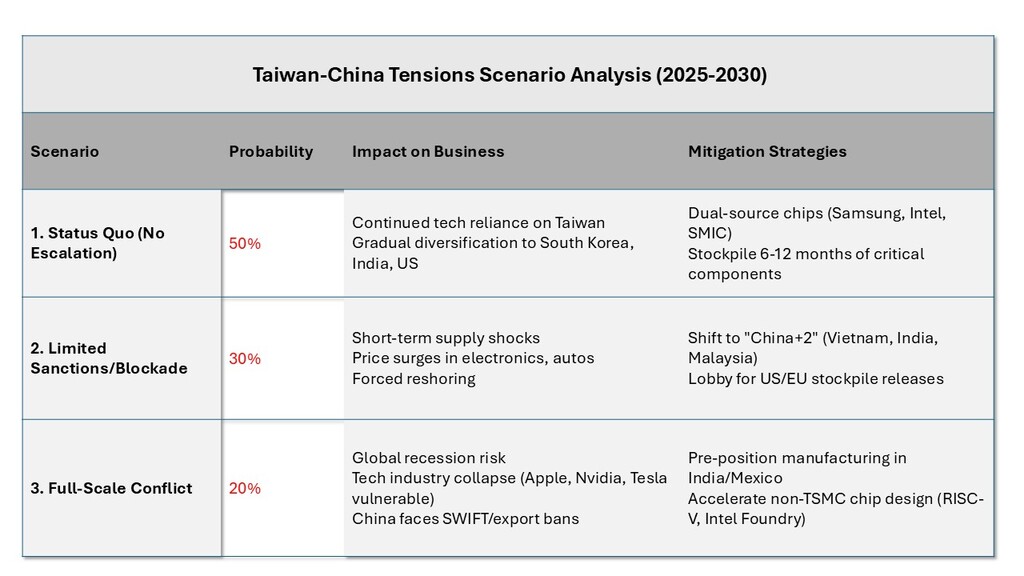

1. Taiwan-China Tensions

Why It Matters: Taiwan produces 60% of the world’s semiconductors (TSMC alone dominates advanced chip manufacturing). A conflict or blockade would disrupt $2 trillion+ in global tech supply chains (iPhones, AI chips, EVs, defense systems).

Taiwan -Scenario Analysis affecting major sectors and how to mitigate business impacts

Key Takeaways:

Best Case: Slow decoupling with managed diversification (Korea’s Samsung, India’s Tata Electronics gain).

Worst Case:War triggers a "tech depression" 12-36 month shortages in advanced chips, forcing autos/tech firms to halt production.

Bans on Chinese apps (TikTok, WeChat) Workaround: Local JVs (e.g., Walmart-Flipkart)

"The key to navigating Asia's complexity is building redundancy into every part of your supply chain," advises Lei Zhang, Founder of Hillhouse Capital

Beyond Traditional Metrics: Non-Financial Risks Investors Must Consider

As investors look beyond GDP and FDI numbers, several non-financial but critical risk layers are increasingly shaping success and failure in Asia’s dynamic markets. These include Environmental, Social, and Governance (ESG) compliance, governance quality, social equity, and political volatility, especially in frontier economies.

ESG Compliance Challenges

Environmental, Social, and Governance (ESG) standards are no longer optional in global investment strategies. These are 3 things companies and countries are judged on, not just how much money they make. Environmental - Pollution, climate change, renewable energy, protecting nature Social - Workers' rights, fair wages, safety, diversity, community support Governance - Fair leadership, anti-corruption, transparency, rules that protect investors and workers

Yet, several Asian markets lag in regulation, enforcement, and reporting mechanisms:

Environmental Gaps: While China and India lead in renewable capacity, environmental violations remain widespread in sectors like textiles, mining, and construction.

Social Concerns: Labor rights issues are prevalent in Vietnam, Bangladesh, and Cambodia. Forced overtime, wage suppression, and unsafe working conditions pose reputational risks.

Governance Shortfalls: Weak board diversity, lack of shareholder protections, and inconsistent climate risk disclosures create friction with institutional ESG benchmarks.

Why ESG Matters (Even for Non-Finance People)

Protects people & planet: Good ESG means safer jobs and a cleaner future.

Attracts investors: Companies and countries with strong ESG often get more international investment.

Reduces risk: ESG issues can cause strikes, lawsuits, pollution fines, or even protests.

Investor Response:

Conduct ESG audits, integrate third-party certification (e.g., B-Corp, Fair Trade), and collaborate with local ESG training bodies.

Asia's ESG Audit Compliance in 2025

Key Insights:

Singapore, Japan, South Korea are top performers: They do well in all three areas: clean energy, worker rights, and honest business rules.

Vietnam, Indonesia, Philippines lag behind: These countries need to improve safety, pay, and company rules.

India and China are making progress: Mid-range scores show improvements, but there's still room to grow.

Corruption and Transparency Issues

Corruption remains a structural barrier to doing business in parts of Asia:

Low CPI Rankings: Myanmar, Cambodia, Pakistan, and Laos routinely rank in the bottom third of Transparency International's Corruption Perceptions Index.

Opaque Permitting and Procurement: Bribery and unofficial fees for licenses, customs clearance, and government tenders erode investor confidence.

Judicial Weakness: Inconsistent enforcement of contracts and arbitrary legal rulings pose a major deterrent for foreign players in countries like Bangladesh and the Philippines.

Investor Response:

Use FCPA-compliant legal partners, avoid JV structures with politically exposed persons (PEPs), and demand audit rights in any state-facing contract.

Corruption Perception Index in Asia in 2024 estimates

A high Corruption Perception Index (CPI) score means that a country is perceived to have lower levels of public sector corruption.

High CPI Score Means: Greater investor confidence, strong rule of law and regulatory enforcement, lower risk of bribery or opaque procurement, better alignment with ESG and ethical standards

⚠️ Low CPI Score Means: Higher risks of fraud, kickbacks, or regulatory manipulation, costlier and slower business operations, reputational risk for global investors, may require mitigation (e.g., using FCPA-compliant legal structures).

Key Insights:

Singapore (83) and Japan (73) are considered low-risk environments.

Philippines (33) and Vietnam (39) suggest elevated governance and compliance risks.

Income Inequality and Social Unrest

Booming growth has not been evenly shared:

Widening Gaps: India’s top 1% owns over 40% of national wealth. Urban-rural divides in Indonesia and the Philippines strain social cohesion.

Youth Underemployment: High graduation rates have not translated into productive employment in countries like Pakistan, leading to disillusionment.

Protest Risk: Displacement due to megaprojects, fuel price hikes, or weak welfare coverage has led to frequent unrest across South Asia.

Investor Response:

Factor in social impact metrics, engage local communities pre-development, and prioritize inclusive hiring strategies.

Political Instability in Frontier Markets

Some of Asia’s lowest-cost destinations carry the highest geopolitical volatility:

Myanmar: The 2021 military coup reversed a decade of investor optimism. Sanctions, civil conflict, and restricted banking access have paralyzed international operations.

Pakistan: Frequent leadership changes, civil-military tensions, and IMF negotiations create a climate of unpredictability, especially in energy and tech sectors.

Sri Lanka: Recent debt crises and protests underscore the fragility of fiscal governance even in middle-income countries.

The chart maps significant events across five Asian countries, highlighting patterns of social unrest, economic instability, and policy shifts over a five-year span

Investor Response:

Deploy country-specific political risk insurance, maintain multi-market hedging strategies, and set clear exit contingencies.

Executive Decision Points

For Manufacturers:

A decision tree for manufactures

For Tech Firms:

Priority 1: Secure quantum talent in Hefei/Hangzhou

Priority 2: Partner with ISRO-linked incubators

Priority 3: Join Singapore's AI Verify program

Proven Strategies to Win in Asian Markets

Forge Local Alliances Example: Walmart owns 77% of Flipkart

Hyper-Localize Marketing Use KOLs on Douyin (China) and K-pop integrations (Korea)

Leverage Government Incentives Vietnam's 10-year tax holidays for tech firms

Adopt Agile Supply Chains SHEIN's 2-week production cycle vs Zara's 6 weeks

Prioritize Mobile-First Strategies 95% of Indonesians access internet via smartphones

The Bottom Line: ROI in Asia’s Business Future

Asia's business landscape rewards those who combine local insight with global expertise. While risks exist, from geopolitical tensions to market saturation, the region offers the world's highest ROI for growth-stage companies.

The companies winning will be those that:

Leverage 2025-specific incentives (e.g., India's updated PLI schemes)

Build modular supply chains

Implement talent pipelines with local universities

Asia 2030, Investment Summary Snapshot

$30T Opportunity: Asia will drive 60% of global GDP growth by 2030.

Top Picks: India, Vietnam, Malaysia, Thailand, Philippines, each with sector-specific strengths.

Hot Sectors: Tech, fintech, green energy, healthcare, led by China and India.

Risks: Geopolitical tensions, ESG gaps, corruption, and social unrest in frontier markets.

Winning Moves: Local alliances, mobile-first supply chains, government incentives, and hyper-local marketing.

Asia is entering a new phase of economic transformation, driven by decades of export-led growth, market liberalization, and human capital development. Through reforms that promoted exports, opened markets, and built...

%20(4).jpg)

%20(1).jpg)

.jpg)

.png)

%20(1).png)

.png)